American Express 2009 Annual Report Download - page 12

Download and view the complete annual report

Please find page 12 of the 2009 American Express annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

|

|

CARDMEMBERS

MERCHANTS

AXP

MERCHANTS

AXP

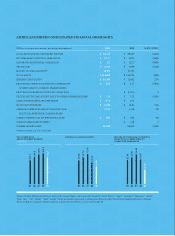

Past-due and net write-o rates improved in the second half of 2009, but remained at high levels compared to prior years. ese charts

show results on a managed basis. On a GAAP basis, 30-day past-due rates were 3.6% for 4Q 2009, 4.0% for 3Q 2009, 4.3% for 2Q 2009,

4.9% for 1Q 2009 and 4.4% for 4Q 2008; while the net write-o rates were 7.4%, 9.1%, 9.6%, 8.0% and 6.5% for the same periods.

MANAGED LOANS 30 DAYS PAST-DUE

AS A PERCENT OF TOTAL

4Q

09

3Q

09

2Q

09

1Q

09

5.0%

4.3%

4.0%

3.6%

4Q

08

4.6%

WORLDWIDE CARDMEMBER LENDING

MANAGED BASIS NET WRITE-OFF RATE

4Q

09

3Q

09

2Q

09

1Q

09

8.2%

9.7%

8.6%

7.3%

4Q

08

6.5%

MONEY MANAGER

helps cardmembers gain

more control over their

personal nances

OUR CLOSED LOOP

network helps us analyze

market trends to better serve

cardmembers and merchants

10

and network services carries comparatively

lower credit risk and capital requirements than

consumer lending.

Clearly, lending is still an important part of our

business. Our customers want the ability to extend

payments, and we want to grant credit wisely and

responsibly. Making credit decisions is not a perfect

science, but we have sophisticated tools to guide

us. We’ve spent a great deal of time examining

how we make decisions, building new capabilities,

integrating new housing and commercial data

into our models, and developing a broad set of

programs to manage high-risk customers. We

have learned from our experiences and improved

our credit and fraud operations

—

all with the goal

Not surprisingly, credit quality in our charge

card portfolio outperformed our lending portfolio.

Write-off rates for charge card receivables were

well controlled. Past-due rates improved from a

year ago.

One key distinction between American Express

and other card issuers is that our business model

relies less on lending. Most of our revenue

comes from spending on cards rather than from

interest income and credit fees. In fact, only 13

percent of our cardmember spending takes

place on proprietary lending cards (excluding

co-brands) in the U.S., and the percentage is

lower in international markets. In addition, our

strong presence in business-to-business payments

AMERICAN EXPRESS COMPANY