Apple 2000 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2000 Apple annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

|

|

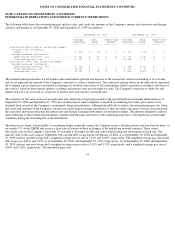

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (CONTINUED)

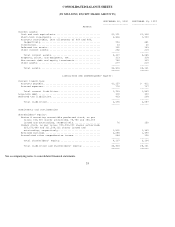

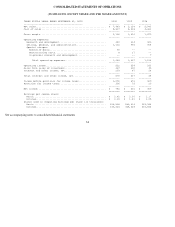

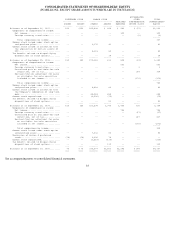

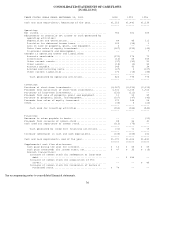

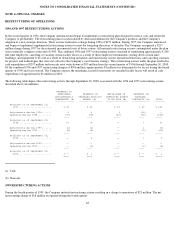

NOTE 2--FINANCIAL INSTRUMENTS (CONTINUED)

INTEREST RATE DERIVATIVES AND FOREIGN CURRENCY INSTRUMENTS

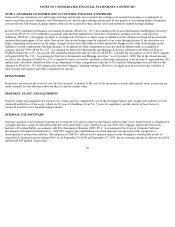

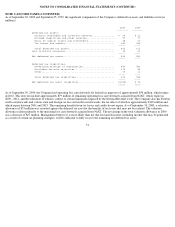

The following table shows the notional principal, net fair value, and credit risk amounts of the Company's interest rate derivative and foreign

currency instruments as of September 30, 2000 and September 25, 1999 (in millions).

The notional principal amounts for off-balance-sheet instruments provide one measure of the transaction volume outstanding as of year-end,

and do not represent the amount of the Company's exposure to credit or market loss. The credit risk amount shown in the table above represents

the Company's gross exposure to potential accounting loss on these transactions if all counterparties failed to perform according to the terms of

the contract, based on then-current currency exchange and interest rates at each respective date. The Company's exposure to credit loss and

market risk will vary over time as a function of interest rates and currency exchange rates.

The estimates of fair value are based on applicable and commonly used pricing models using prevailing financial market information as of

September 30, 2000 and September 25, 1999. In certain instances where judgment is required in estimating fair value, price quotes were

obtained from several of the Company's counterparty financial institutions. Although the table above reflects the notional principal, fair value,

and credit risk amounts of the Company's interest rate and foreign exchange instruments, it does not reflect the gains or losses associated with

the exposures and transactions that the interest rate and foreign exchange instruments are intended to hedge. The amounts ultimately realized

upon settlement of these financial instruments, together with the gains and losses on the underlying exposures, will depend on actual market

conditions during the remaining life of the instruments.

The interest rate swaps, which qualify as accounting hedges, generally require the Company to pay a floating interest rate based on the three-

or

six-month U.S. dollar LIBOR and receive a fixed rate of interest without exchanges of the underlying notional amounts. These swaps

effectively convert the Company's fixed-rate 10 year debt to floating-rate debt and convert the floating rate investments to fixed rate. The

maturity date of the asset swaps is September 2001 and the debt swaps mature in February of 2004. As of September 30, 2000 and September

25, 1999, interest rate debt swaps had a weighted-average receive rate of 7.21% and 6.04%, respectively. The weighted-average pay rate on the

debt swaps was 6.68% and 5.45% as of September 30, 2000, and September 25, 1999, respectively. As of September 30, 2000 and September

25, 1999, interest rate asset swaps had a weighted-average receive rate of 5.50% and 5.53% respectively; and a weighted-average pay rate of

6.66% and 5.24%, respectively. The unrealized gains and

43

SEPTEMBER 30, 2000 SEPTEMBER 25, 1999

----------------------------------- ----------------------------------

NOTIONAL FAIR CREDIT RISK NOTIONAL FAIR CREDIT RISK

PRINCIPAL VALUE AMOUNTS PRINCIPAL VALUE AMOUNTS

--------- --------- ----------- --------- -------- -----------

Transactions qualifying as accounting hedges:

Interest rate instruments:

Swaps....................................... $ 800 $ (1) $ 4 $ 790 $ (5) $ --

Foreign exchange instruments:

Spot/Forward contracts, net................. $ 826 $ 10 $ 10 $ 730 $ (8) $ 4

Purchased options, net...................... $ 615 $ 21 $ -- $1,305 $ 4 $ --

Transactions other than accounting hedges:

Foreign exchange instruments:

Spot/Forward contracts, net................. $ 275 $ -- $ -- $ 185 $ (1) $ --

Purchased options, net...................... $1,051 $ 4 $ 4 $ 645 $ 8 $ 8

Sold options, net........................... $1,201 $ (5) $ -- $ 585 $(17) $ --