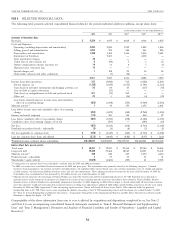

Charter 2005 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 2005 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

|

|

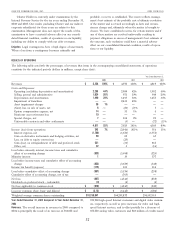

CHARTER COMMUNICATIONS, INC. 2005 FORM 10-K

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF

OPERATIONS.

Reference is made to ‘‘Item 1A. Risk Factors’’ and ‘‘Cautionary competition from DBS has resulted in net analog video

Statement Regarding Forward-Looking Statements,’’ which customer losses and decreased growth rates for digital video

describes important factors that could cause actual results to customers. Competition from DSL providers combined with

differ from expectations and non-historical information con- limited opportunities to expand our customer base now that

tained herein. In addition, the following discussion should be approximately 33% of our analog video customers subscribe to

read in conjunction with the audited consolidated financial our high-speed Internet services has resulted in decreased

statements of Charter Communications, Inc. and subsidiaries as growth rates for high-speed Internet customers. In the recent

of and for the years ended December 31, 2005, 2004 and 2003. past, we have grown revenues by offsetting video customer

losses with price increases and sales of incremental advanced

INTRODUCTION services such as high-speed Internet, video on demand, digital

video recorders and high definition television. We expect to

We continue to pursue opportunities to improve our liquidity. continue to grow revenues through price increases and through

Our efforts in this regard have resulted in the completion of a continued growth in high-speed Internet and incremental new

number of financing transactions in 2005 and 2006, as follows: services including telephone, high definition television, VOD and

(the January 2006 sale by our subsidiaries, CCH II, LLC DVR service.

(‘‘CCH II’’) and CCH II Capital Corp., of an additional Historically, our ability to fund operations and investing

$450 million principal amount of their 10.250% senior notes activities has depended on our continued access to credit under

due 2010; our credit facilities. We expect we will continue to borrow

under our credit facilities from time to time to fund cash needs.

(the October 2005 entry by our subsidiaries, CCO Holdings

The occurrence of an event of default under our credit facilities

and CCO Holdings Capital Corp., as guarantor thereunder,

could result in borrowings from these facilities being unavailable

into a $600 million senior bridge loan agreement with

to us and could, in the event of a payment default or

various lenders (which was reduced to $435 million as a

acceleration, trigger events of default under our outstanding

result of the issuance of CCH II notes);

notes and would have a material adverse effect on us.

(the September 2005 exchange by Charter Holdings, CCH I Approximately $30 million of indebtedness under our credit

and CIH of approximately $6.8 billion in total principal facilities is scheduled to mature during 2006. We expect to fund

amount of outstanding debt securities of Charter Holdings payment of such indebtedness through borrowings under our

in a private placement for new debt securities; revolving credit facilities.

(the August 2005 sale by our subsidiaries, CCO Holdings Overview of Operations

and CCO Holdings Capital Corp., of $300 million of Approximately 86% of our revenues for each of the years ended

83

/4% senior notes due 2013; December 31, 2005 and 2004, respectively, are attributable to

(the March and June 2005 issuance of $333 million of monthly subscription fees charged to customers for our video,

Charter Operating notes in exchange for $346 million of high-speed Internet, telephone and commercial services provided

Charter Holdings notes; by our cable systems. Generally, these customer subscriptions

may be discontinued by the customer at any time. The

(the repurchase during 2005 of $136 million of Charter’s remaining 14% of revenue is derived primarily from advertising

4.75% convertible senior notes due 2006 leaving $20 million revenues, franchise fee revenues, which are collected by us but

in principal amount outstanding; and then paid to local franchising authorities, pay-per-view and

(the March 2005 redemption of all of CC V Holdings, VOD programming where users are charged a fee for individual

LLC’s outstanding 11.875% senior discount notes due 2008 programs viewed, installation or reconnection fees charged to

at a total cost of $122 million. customers to commence or reinstate service, and commissions

related to the sale of merchandise by home shopping services.

During the years 1999 through 2001, we grew significantly, We have increased revenues during the past three years,

principally through acquisitions of other cable businesses primarily through the sale of digital video and high-speed

financed by debt and, to a lesser extent, equity. We have no Internet services to new and existing customers and price

current plans to pursue any significant acquisitions. However, we increases on video services offset in part by dispositions of

may pursue exchanges of non-strategic assets or divestitures, systems. Going forward, our goal is to increase revenues by

such as the sale of cable systems to Atlantic Broadband Finance, offsetting video customer losses with price increases and sales of

LLC. We therefore do not believe that our historical growth incremental advanced services such as telephone, high-speed

rates are accurate indicators of future growth. Internet, video on demand, digital video recorders and high

The industry’s and our most significant operational chal- definition television. See ‘‘Item 1. Business — Sales and Market-

lenges include competition from DBS providers and DSL service ing’’ for more details.

providers. See ‘‘Item 1. Business — Competition.’’ We believe that

31