Charter 2005 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2005 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

|

|

CHARTER COMMUNICATIONS, INC. 2005 FORM 10-K

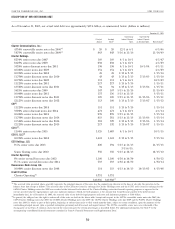

As of December 31, 2005 and 2004, our long-term debt revolving credit facility, and up to 3.25% for the Term B facility,

totaled approximately $19.4 billion and $19.5 billion, respec- and for base rate loans of up to 2.00% for the Term A facility

tively. This debt was comprised of approximately $5.7 billion and revolving credit facility, and up to 2.25% for the Term B

and $5.5 billion of credit facility debt, $12.8 billion and facility. A quarterly commitment fee of up to .75% is payable on

$13.0 billion accreted amount of high-yield notes and $863 mil- the average daily unborrowed balance of the revolving credit

lion and $990 million accreted amount of convertible senior facilities.

notes at December 31, 2005 and 2004, respectively. The obligations of our subsidiaries under the Charter

As of December 31, 2005 and 2004, the weighted average Operating credit facilities (the ‘‘Obligations’’) are guaranteed by

interest rate on the credit facility debt was approximately 7.8% Charter Operating’s immediate parent company, CCO Holdings,

and 6.8%, the weighted average interest rate on our high-yield and the subsidiaries of Charter Operating, except for immaterial

notes was approximately 10.2% and 9.2%, and the weighted subsidiaries and subsidiaries precluded from guaranteeing by

average interest rate on the convertible senior notes was reason of the provisions of other indebtedness to which they are

approximately 6.3% and 5.7%, respectively, resulting in a subject (the ‘‘non-guarantor subsidiaries,’’ primarily Renaissance

blended weighted average interest rate of 9.3% and 8.8%, and its subsidiaries). The Obligations are also secured by (i) a

respectively. The interest rate on approximately 77% and 83% of lien on all of the assets of Charter Operating and its subsidiaries

the total principal amount of our debt was effectively fixed, (other than assets of the non-guarantor subsidiaries), to the

including the effects of our interest rate hedge agreements as of extent such lien can be perfected under the Uniform Commer-

December 31, 2005 and 2004, respectively. The fair value of our cial Code by the filing of a financing statement, and (ii) a pledge

high-yield notes was $10.4 billion and $12.2 billion at Decem- by CCO Holdings of the equity interests owned by it in Charter

ber 31, 2005 and 2004, respectively. The fair value of our Operating or any of Charter Operating’s subsidiaries, as well as

convertible senior notes was $647 million and $1.1 billion at intercompany obligations owing to it by any of such entities.

December 31, 2005 and 2004, respectively. The fair value of our Upon the Charter Holdings Leverage Ratio (as defined in

credit facilities is $5.7 billion and $5.5 billion at December 31, the indenture governing the Charter Holdings senior notes and

2005 and 2004, respectively. The fair value of high-yield and senior discount notes) being under 8.75 to 1.0, the Charter

convertible notes is based on quoted market prices, and the fair Operating credit facilities require that the 11.875% notes due

value of the credit facilities is based on dealer quotations. 2008 issued by CC V Holdings, LLC be redeemed. Because

such Leverage Ratio was determined to be under 8.75 to 1.0,

Charter Operating Credit Facilities — General CC V Holdings, LLC redeemed such notes in March 2005, and

The Charter Operating credit facilities were amended and CC V Holdings, LLC and its subsidiaries (other than non-

restated concurrently with the sale of $1.5 billion senior second- guarantor subsidiaries) became guarantors of the Obligations and

lien notes in April 2004, among other things, to defer maturities have granted a lien on all of their assets as to which a lien can

and increase availability under these facilities and to enable be perfected under the Uniform Commercial Code by the filing

Charter Operating to acquire the interests of the lenders under of a financing statement.

the CC VI Operating, CC VIII Operating and Falcon credit

facilities, thereby consolidating all credit facilities under one Charter Operating Credit Facilities — Restrictive Covenants

amended and restated Charter Operating credit agreement. The Charter Operating credit facilities contain representations

The Charter Operating credit facilities provide borrowing and warranties, and affirmative and negative covenants custom-

availability of up to $6.5 billion as follows: ary for financings of this type. The financial covenants measure

performance against standards set for leverage, debt service

(two term facilities: coverage, and interest coverage, tested as of the end of each

(i) a Term A facility with a total principal amount of quarter. The maximum allowable leverage ratio is 4.25 to 1.0,

$2.0 billion, of which 12.5% matures in 2007, 30% the minimum allowable interest coverage ratio is 1.25 to 1.0 and

matures in 2008, 37.5% matures in 2009 and 20% the minimum allowable debt service coverage ratio is 1.05 to

matures in 2010; and 1.0. Additionally, the Charter Operating credit facilities contain

provisions requiring mandatory loan prepayments under specific

(ii) a Term B facility with a total principal amount of circumstances, including when significant amounts of assets are

$3.0 billion, which shall be repayable in 27 equal sold and the proceeds are not reinvested in assets useful in the

quarterly installments aggregating in each loan year to business of the borrower within a specified period, and upon the

1% of the original amount of the Term B facility, with incurrence of certain indebtedness when the ratio of senior first

the remaining balance due at final maturity in 2011; and lien debt to operating cash flow is greater than 2.0 to 1.0.

(a revolving credit facility, in a total amount of $1.5 billion, The Charter Operating credit facilities permit Charter

with a maturity date in 2010. Operating and its subsidiaries to make distributions to pay

interest on the CCO Holdings senior notes, the CCH II senior

Amounts outstanding under the Charter Operating credit

notes, the CCH I senior notes, the CIH senior notes, the

facilities bear interest, at Charter Operating’s election, at a base

Charter Holdings senior notes and the Charter convertible

rate or the Eurodollar rate, as defined, plus a margin for

senior notes, provided that, among other things, no default has

Eurodollar loans of up to 3.00% for the Term A facility and

52