GE 2013 Annual Report Download - page 11

Download and view the complete annual report

Please find page 11 of the 2013 GE annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

|

|

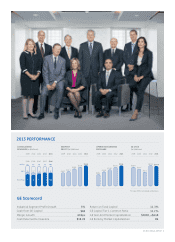

Our industrial segment earnings grew

5%. Performance was broad-based

with four businesses growing earnings

10% or more: Aviation, Oil & Gas,

Transportation and Appliances &

Lighting. We ended the year with

$244 billion in backlog, a record.

GE Capital grew its earnings by 12%,

behind strong performance in Real

Estate and international lending and

leasing. We continued to shrink our

balance sheet; ending net investment

was $380 billion at year-end, down

more than 40% from our pre-crisis

peak. With a shrinking balance sheet

and massive fi nancial strength,

GE Capital was able to pay a $6 billion

dividend to the parent.

Our total shareholder return expanded

by 38% in 2013, ahead of the market.

We added $64 billion of market cap

and, at $282 billion, are the sixth most

valuable company in the world. At

year-end, we increased our dividend

by 16%.

In 2014, we have planned for our

industrial earnings to grow by more

than 10%. We expect organic revenue

growth between 4%–7%. The big

initiatives will fuel our success. Growth

market orders expanded by 11%

in 2013; this will translate into solid

revenue growth. Our service revenue

is $45 billion, and we expect solid rev-

enue growth in 2014. We are planning

for another year of substantial margin

enhancement, beyond the 15.7% we

achieved in 2013.

Margins have been an area of focus

for GE. A decade ago, during the

power bubble, we had artifi cially high

margins. This has now been reset, and

we have been making steady prog-

ress. Through simplifi cation, we have

made substantial reductions in struc-

tural cost. FastWorks is focused on

equipment margins, which will be up

substantially this year. We are restruc-

turing our lower-margin businesses

with a target of at least 10% margins

for them in the near term.

GE Capital’s earnings will decline in

2014 and 2015 as we exit Retail

Finance. However, we plan to grow

move commercial decisions closer to

the customer. In our Aviation services

business, 75% of the fl ow commercial

deals are approved in the regions

with quick turnaround. Our Company

is beginning to feel the market speed.

In a digital world, the major source of

scale advantage derives from a lean

backroom structure with a foundation

of information. GE will be a major ben-

efi ciary of cloud computing, simplifi ed

systems and mobility.

We will still make a few mistakes. But

the biggest risks at GE are the inabil-

ity to seize market opportunities,

layers that block reality and leaders

who are not personally account-

able. Simplifi cation is making us

more competitive.

We Are Delivering

for Investors

Executing our initiatives will deliver

results for investors. We would like

investors to view our fi nancial per-

formance as a multi-year plan with

substantial progress reached each

quarter and year. By 2016, we expect

to have 70% of GE’s earnings from

our industrial businesses. We expect

to have industrial margins and returns

exceeding 17%, at the top of our peers.

We expect GE Capital to generate good

returns while delivering cash to the

parent. We expect to generate more

than $90 billion of cash to allocate,

returning the majority of that to you in

dividends and buyback. And, we plan

to grow EPS each year.

We made progress in 2013. We earned

$24.5 billion of segment profi t, up 7%.

We grew operating EPS by 9% and

returned $18 billion to you through divi-

dends and share repurchase. We ran the

Company well, with margins expanding

by 60 basis points and $17 billion of cash

generation, excluding NBCUniversal

deal-related taxes. GE Capital fi nished

the year with Tier 1 capital above 11%

and $75 billion of liquidity.

DELIVERING FOR INVESTORS

SIGNIFICANT

CASH

INDUSTRIAL

MARGIN GROWTH GROW EPS

EVERY YEAR

70% OF EARNINGS

FROM INDUSTRIAL

1 3

4

2

15.7%

$1.64

~55%

70%+

17%+

2013 2016

2014–201620162013

20142013 2015 2016

FUNDING:

Dividends

Buyback

M&A

Organic

Growth

$90B+

GE 2013 ANNUAL REPORT 9