GE 2013 Annual Report Download - page 143

Download and view the complete annual report

Please find page 143 of the 2013 GE annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150

|

|

GE 2013 ANNUAL REPORT 141

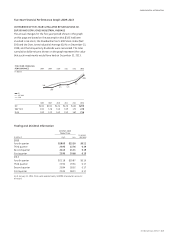

Average GE Shareowners’ Equity, Excluding Effects of Discontinued Operations (a)

December 31 (In millions) 2013 2012 2011 2010 2009

Average GE shareowners’ equity (b) $ 124,501 $ 120,411 $ 122,289 $ 116,179 $ 110,535

Less the effects of the average net investment in

discontinued operations (167) (478) 4,924 13,819 17,432

Average GE shareowners’ equity, excluding effects of

discontinued operations (a) $ 124,668 $ 120,889 $ 117,365 $ 102,360 $ 93,103

(a) Used for computing return on average GE shareowners’ equity and return on average total capital invested (ROTC).

(b) On an annual basis, calculated using a five-point average.

Our ROTC calculation excludes earnings (losses) of discontinued

operations from the numerator because U.S. GAAP requires us

to display those earnings (losses) in the Statement of Earnings.

Our calculation of average GE shareowners’ equity may not be

directly comparable to similarly titled measures reported by

other companies. We believe that it is a clearer way to measure

the ongoing trend in return on total capital for the continuing

operations of our businesses given the extent that discontinued

operations have affected our reported results. We believe that

this results in a more relevant measure for management and

investors to evaluate performance of our continuing operations,

on a consistent basis, and to evaluate and compare the perfor-

mance of our continuing operations with the ongoing operations

of other businesses and companies.

Defi nitions indicating how the above-named ratios are calcu-

lated using average GE shareowners’ equity, excluding effects of

discontinued operations, can be found in the Glossary.

Ratio of Adjusted Debt to Equity at GECC, Net of Adjusted Cash and Equivalents and with Classification of Hybrid Debt as Equity

December 31 (Dollars in millions) 2013 2012 2011 2010 2009

GECC debt $ 371,062 $ 397,039 $ 442,830 $ 470,363 $ 493,224

Add debt of businesses held for sale and discontinued operations 316 403 527 575 7,136

Adjusted GECC debt 371,378 397,442 443,357 470,938 500,360

Less cash and equivalents 74,873 61,853 76,641 60,231 62,565

Less cash of businesses held for sale and discontinued operations 236 265 332 222 1,975

Less hybrid debt 7,725 7,725 7,725 7,725 7,725

$ 288,544 $ 327,599 $ 358,659 $ 402,760 $ 428,095

GECC equity $ 82,694 $ 81,890 $ 77,110 $ 68,984 $ 70,833

Plus hybrid debt 7,725 7,725 7,725 7,725 7,725

$ 90,419 $ 89,615 $ 84,835 $ 76,709 $ 78,558

Ratio 3.19:1 3.66:1 4.23:1 5.25:1 5.45:1

We have provided the GECC ratio of debt to equity on a basis that

refl ects the use of cash and equivalents as a reduction of debt,

and long-term debt due in 2066 and 2067 classifi ed as equity.

For purposes of this ratio, we have also adjusted cash and debt

balances to include amounts classifi ed as assets and liabilities of

businesses held for sale and discontinued operations. We believe

that this is a useful comparison to a GAAP-based ratio of debt to

equity because cash balances may be used to reduce debt and

because this long-term debt has equity-like characteristics. The

usefulness of this supplemental measure may be limited, how-

ever, as the total amount of cash and equivalents at any point in

time may be different than the amount that could practically be

applied to reduce outstanding debt, and it may not be advanta-

geous or practical to replace certain long-term debt with equity.

Despite these potential limitations, we believe that this measure,

considered along with the corresponding GAAP measure, pro-

vides investors with additional information that may be more

comparable to other fi nancial institutions and businesses.