HSBC 2002 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2002 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

|

|

81

compared to 2001 and at 31 December 2001 funds

under management stood at US$9.0 billion (US$3.9

billion of which arose from the acquisition of CCF

Brasil). In total, funds under management by our

Brazilian operations now rank fifth largest in Brazil.

Life insurance premia grew by 24 per cent and now

represent 36 per cent (34 per cent in 2000) of total

insurance premia. In Argentina, fee income was

US$30 million, or 32.6 per cent, higher than in 2000.

Initiatives taken to improve revenue mix were

reflected in higher levels of fees from credit cards

and asset management. In addition, fee income

reflected fees earned from being an arranger and

market-maker for Argentine government bond

auctions.

The increased contribution from fee income was

partly offset by lower levels of dealing profits.

Brazil’s dealing profits of US$20 million were US$7

million lower than in 2000 as losses were incurred on

interest rate trading positions as interest rates rose.

These losses were only partly offset by higher levels

of dealing profits on foreign exchange and debt

securities trading. Argentina reported dealing losses

of US$6 million compared to dealing profits of

US$16 million in 2000. This resulted from difficult

trading conditions as a result of volatility in foreign

exchange rates and losses on bond positions.

HSBC’s Argentine pensions, healthcare and life

insurance businesses also reported falls in income as

rising unemployment and collapsing economic

conditions led to a 6 per cent fall in healthcare

membership, reduced contributions to pensions funds

and a reduction in annuities business.

Operating expenses, excluding goodwill

amortisation, of US$1,497 million were US$133

million, or 10 per cent, higher than 2000. In Brazil

operating expenses of US$1,023 million, were higher

by US$141 million reflecting the acquisition of CCF

Brasil and restructuring provisions. As economic

conditions became less certain cost controls were put

in place to restrain operating expense growth with a

number of contracts renegotiated. Investment in

electronic distribution channels continued and HSBC

Bank Brasil’s internet and wireless banking services

expanded with a twofold increase in the number of

registered Internet Bank users since December 2000,

to 420,000 performing on average 1.9 million on-line

transactions a month. The newer Wireless Services,

which encompass e-mail, Cellular and Palm

Banking, have 24,000 users, a 40 per cent increase

since June 2001. In Argentina, cost controls were

rigorously enforced and the increase in operating

expenses of US$11 million was due mainly to the

write-down to market value of certain properties now

considered to be permanently impaired.

Provisions for bad and doubtful debts of US$927

million increased by US$765 million compared to

2000. In Brazil, the significant increase in

provisioning requirements of US$80 million

reflected a change in the lending portfolio mix.

Targeted growth in the high margin personal lending

portfolio led to an expected and corresponding

increase in delinquencies and provisioning levels

rose to reflect the underlying risks within the

consumer portfolio. In Argentina, provisions for bad

and doubtful debts rose substantially to reflect the

disastrous economic conditions and financial

uncertainties. This is reflected in the US$681 million

increase in the bad and doubtful debt provisions to

US$737 million compared to US$56 million in 2000.

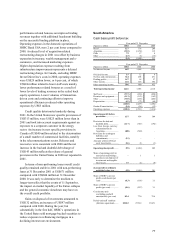

Analysis by line of business

Profit on ordinary activities before tax (cash

basis) by line of business

Year ended

31 December

2002

31 December

2001*

31 December

2000*

US$m % US$m % US$m %

Personal Financial

Services ........................ 3,543 33.7 3,457 39.3 3,010 29.2

Commercial Banking.......... 3,034 28.8 2,385 27.1 2,780 27.0

Corporate, Investment

Banking and Markets.... 3,717 35.4 4,033 45.8 3,559 34.6

Private Banking.................. 420 4.0 456 5.2 578 5.6

Other ................................ (201 ) (1.9) (1,524 ) (17.4 ) 373 3.6

10,513 100.0 8,807 100.0 10,300 100.0

* Restated for changes in management responsibility. The principal change

relates to aligning domestic private banking with international private banking

in the United States.

The cash basis measures included in this section are derived by deducting goodwill

amortisation from the equivalent reported measure.

Total assets by line of business

Year ended

31 December

2002

31 December

2001

Total assets# US$m % US$m %

Personal Financial Services. 171,496 22.9 138,908 20.2

Commercial Banking........... 113,525 15.1 101,002 14.7

Corporate, Investment

Banking and Markets..... 394,542 52.6 374,282 54.4

Private Banking................... 48,346 6.5 52,135 7.6

Other ................................. 21,892 2.9 21,281 3.1

749,801 100.0 687,608 100.0

#Excluding Hong Kong SAR Government certificates of indebtedness.