HSBC 2002 Annual Report Download - page 85

Download and view the complete annual report

Please find page 85 of the 2002 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

|

|

83

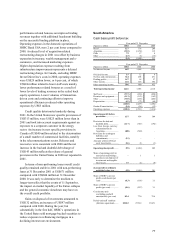

Personal Financial Services

Cash basis profit before tax

Year ended

31 December

2002

31 December

2001*

31 December

2000*

US$m % US$m % US$m %

Europe ................................ 987 27.8 1,091 31.6 624 20.7

Hong Kong ......................... 1,705 48.1 1,631 47.2 1,680 55.8

Rest of Asia-Pacific............. 127 3.6 80 2.3 189 6.3

North America .................... 757 21.4 593 17.1 482 16.0

South America .................... (33 ) (0.9) 62 1.8 35 1.2

3,543 100.0 3,457 100.0 3,010 100.0

Year ended

Figures in US$m 31 December

2002

31 December

2001*

31 December

2000*

Net interest income....... 7,581 6,828 6,508

Dividend income .......... 651

Net fees and

commissions ............ 2,979 2,877 2,644

Dealing profits.............. 50 53 97

Other income................ 788 806 711

Other operating

income ..................... 3,823 3,741 3,453

Total operating

income..................... 11,404 10,569 9,961

Operating expenses

(excluding goodwill

amortisation)............ (6,973) (6,477 ) (6,237)

Operating profit

before provisions.... 4,431 4,092 3,724

Provisions for bad and

doubtful debts .......... (857 ) (767) (602)

Provisions for

contingent liabilities

and commitments (42 ) (17 ) (31)

Amounts written off

fixed asset

investments.............. (2 ) (5 )

–

Operating profit.......... 3,530 3,303 3,091

Share of operating

(losses) in joint

ventures ................... (23 ) (99 ) (52)

Share of operating

profit/(losses) in

associates 17 43 (44)

Gains on disposal of

investments and

tangible fixed assets. 19 210 15

Profit on ordinary

activities before

tax (cash basis) ....... 3,543 3,457 3,010

Share of HSBC’ s pre-

tax profits (cash

basis) (per cent) 33.7 39.3 29.2

Cost: income ratio

(excluding goodwill

amotisation) (per

cent)......................... 61.1 61.3 62.6

Selected balance sheet data (third party items

only)

At

Figures in US$m 31 December

2002

31 December

2001*

31 December

2000*

Loans and advances to

customers (net)........ 143,696 113,844 103,901

Customer deposits........ 257,880 228,931 216,058

*Restatement consistent with page 81.

Year ended 31 December 2002 compared with

year ended 31 December 2001

On a cash basis Personal Financial Services

contributed US$3,543 million to pre-tax profits in

2002 and represented 33.7 per cent of such profits.

Growth in pre-tax profits over 2001 amounted to

US$86 million, an increase of 2 per cent.

Revenues grew by 8 per cent driven by strong

growth in net interest income as mortage banking

and personal savings grew strongly. Cost growth of

8 per cent tracked revenue growth, with benefits

from moving activity to the HSBC’s Group’s

Shared Service Centres offset by increased

marketing costs and property costs arising on

surplus space following relocation of the PFS

central London based staff to the new head office

at Canary Wharf.

Provisions for bad and doubtful debts rose by

US$90 million, an increase of 12 per cent, but less

than the rise in customer lending. Disposal gains

were significantly lower than 2001, which

benefited from the sale of the HSBC’s interest in

British Interactive Broadcasting in May 2001.

Net interest income increased by US$753

million or 11 per cent. Within this, net interest

income in Europe rose by US$405 million as the

investment made in improving customer

relationship management systems improved the

ability of front office staff in the branches to sell

more effectively. In the low interest rate

environment, there has been significant growth in

personal lending and with the property market

continuing to rise there has been strong demand for

mortgages and equity release loans. Personal

current accounts and savings accounts continued to

grow as customers preferred liquidity and security

in the uncertain investment climate. The impact of

product re-pricing initiatives in the UK in late 2001

and the benefit of lower cost of funds has increased

spreads.