LabCorp 2010 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2010 LabCorp annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

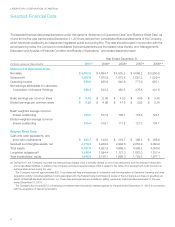

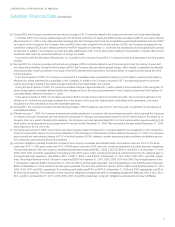

12

LABORATORY CORPORATION OF AMERICA

Management’s Discussion and Analysis

of Financial Condition and Results of Operations

Liquidity, Capital Resources and Financial Position

The Company’s strong cash-generating capability and financial

condition typically have provided ready access to capital markets.

The Company’s principal source of liquidity is operating cash

flow, supplemented by proceeds from debt offerings. This cash-

generating capability is one of the Company’s fundamental

strengths and provides substantial financial flexibility in meeting

operating, investing and financing needs. The Company’s senior

unsecured credit facilities are further discussed in “Note 11 to

Consolidated Financial Statements.”

Operating Activities

In 2010, the Company’s operations provided $883.6 of cash,

net of $16.8 in transition payments to UnitedHealthcare, reflect-

ing the Company’s solid business results. The increase in the

Company’s cash flow from operations primarily resulted from

lower transition payments to UnitedHealthcare. The Company

continued to focus on efforts to increase cash collections

from all payers and to generate on-going improvements to the

claim submission processes.

The Company made contributions to the defined benefit

retirement plan (“Company Plan”) of $0.0, $54.8 and $0.0 in

2010, 2009 and 2008, respectively. In October 2009, the

Company received approval from its Board of Directors to

freeze any additional service-based credits for any years of

service after December 31, 2009 on the Company Plan and

the PEP. Both plans have been closed to new participants.

Employees participating in the Company Plan and the PEP

no longer earn service-based credits, but continue to earn

interest credits. In addition, effective January 1, 2010, all

employees eligible for the defined contribution retirement plan

(the “401K Plan”) receive a minimum 3% non-elective contri-

bution (“NEC”) concurrent with each payroll period. The NEC

replaces the Company match, which has been discontinued.

Employees are not required to make a contribution to the

401K Plan to receive the NEC. The NEC is non-forfeitable and

vests immediately. The 401K Plan also permits discretionary

contributions by the Company of 1% to 3% of pay for eligible

employees based on service. Non-elective and discretionary

contributions are approximately $25.4 higher in 2010 than the

Company’s contributions to its 401K Plan in 2009.

Projected pension expense for the Company Plan and PEP is

expected to decrease from $9.6 in 2010 to $8.9 in 2011. In addi-

tion, the Company does not plan to make contributions to the

Company Plan during 2011. See “Note 16 to the Consolidated

Financial Statements” for a further discussion of the Company’s

pension and postretirement plans.

Investing Activities

Capital expenditures were $126.1, $114.7 and $156.7 for 2010,

2009 and 2008, respectively. The Company expects capital

expenditures of approximately $140.0 to $150.0 in 2011. The

Company will continue to make important investments in its

business, including information technology. Such expenditures

are expected to be funded by cash flow from operations, as well

as borrowings under the Company’s revolving credit facilities

as needed.

The Company remains committed to growing its business

through strategic acquisitions and licensing agreements. The

Company has invested a total of $1,738.7 over the past three

years in strategic business acquisitions. These acquisitions

have helped strengthen the Company’s geographic presence

along with expanding capabilities in the specialty testing oper-

ations. The Company believes the acquisition market remains

attractive with a number of opportunities to strengthen its

scientific capabilities, grow esoteric testing capabilities and

increase presence in key geographic areas.

The Company has invested a total of $50.6 over the past

three years in licensing new testing technologies (including

approximately $49.4 estimated fair market value of technology

acquired in certain acquisitions in 2010 and 2009) and had $69.0

net book value of capitalized patents, licenses and technology

at December 31, 2010. While the Company continues to believe

its strategy of entering into licensing and technology distribution

agreements with the developers of leading-edge technologies

will provide future growth in revenues, there are certain risks

associated with these investments. These risks include, but

are not limited to, the failure of the licensed technology to gain

broad acceptance in the marketplace and/or that insurance

companies, managed care organizations, or Medicare and

Medicaid will not approve reimbursement for these tests at a

level commensurate with the costs of running the tests. Any

or all of these circumstances could result in impairment in the

value of the related capitalized licensing costs.