LabCorp 2010 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2010 LabCorp annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

|

|

34

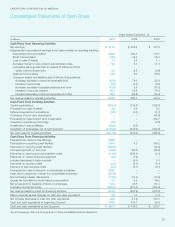

a percentage based on the Company’s credit rating with Standard

& Poor’s Ratings Services. The remaining quarterly principal

repayments of the Term Loan Facility are $18.8 from March 31,

2011 to September 30, 2012 with $243.8 due on the maturity

date of October 26, 2012. At December 31, 2010, future

principal repayments under the Term Loan facility are as follows:

2011 - $75.0 and 2012 - $300.0.

The senior credit facilities are available for general corporate

purposes, including working capital, capital expenditures,

acquisitions, funding of share repurchases and other payments.

The agreement contains certain debt covenants which require

that the Company maintain a leverage ratio of no more than

2.5 to 1.0 and an interest coverage ratio of at least 5.0 to 1.0.

Both ratios are calculated in relation to EBITDA (Earnings Before

Interest, Taxes, Depreciation, and Amortization). The credit

agreement allows payment of dividends provided that the

Company is not in default (as defined in the agreement) and

its leverage ratio is less than 2.0 to 1.0. The Company is in

compliance with all covenants at December 31, 2010.

On March 31, 2008, the Company entered into a three-year

interest rate swap agreement to hedge variable interest rate

risk on the Company’s variable interest rate term loan. On a

quarterly basis under the swap, the Company pays a fixed rate

of interest (2.92%) and receives a variable rate of interest

based on the three-month LIBOR rate on an amortizing notional

amount of indebtedness equivalent to the term loan balance

outstanding. The swap has been designated as a cash flow

hedge. Accordingly, the Company recognizes the fair value of

the swap in the consolidated balance sheets and any changes

in the fair value are recorded as adjustments to accumulated

other comprehensive income (loss), net of tax. The fair value

of the interest rate swap agreement is the estimated amount

that the Company would pay or receive to terminate the swap

agreement at the reporting date. The fair value of the swap

was a liability of $2.4 and $10.6 at December 31, 2010 and

2009, respectively, and is included in other liabilities in the

consolidated balance sheets.

As of December 31, 2010, the effective interest rates on

the Term Loan Facility and Revolving Facility were 3.67% and

0.61%, respectively.

Zero-Coupon Convertible Subordinated Notes

The Company had $354.6 and $368.8 aggregate principal

amount at maturity of zero-coupon convertible subordinated

notes (the “notes”) due 2021 outstanding at December 31,

2010 and 2009, respectively. The notes, which are subordinate

to the Company’s bank debt, were sold at an issue price of

$671.65 per $1,000 principal amount at maturity (representing

a yield to maturity of 2.0% per year). Each one thousand dollar

principal amount at maturity of the notes is convertible into

13.4108 shares of the Company’s common stock, subject to

adjustment in certain circumstances, if one of the following

conditions occurs:

1) If the sales price of the Company’s common stock for at

least 20 trading days in a period of 30 consecutive trading

days ending on the last trading day of the preceding quarter

reaches specified thresholds (beginning at 120% and declining

0.1282% per quarter until it reaches approximately 110%

for the quarter beginning July 1, 2021 of the accreted

conversion price per share of common stock on the last

day of the preceding quarter). The accreted conversion

price per share will equal the issue price of a note plus the

accrued original issue discount and any accrued contingent

additional principal, divided by the number of shares of

common stock issuable upon conversion of a note on that

day. The conversion trigger price for the fourth quarter of

2010 was $69.27.

2) If the credit rating assigned to the notes by Standard & Poor’s

Ratings Services is at or below BB-.

3) If the notes are called for redemption.

4) If specified corporate transactions have occurred (such as

if the Company is party to a consolidation, merger or binding

share exchange or a transfer of all or substantially all of

its assets).

Holders of the notes may require the Company to purchase

in cash all or a portion of their notes on September 11, 2011

at $819.54 per note, plus any accrued contingent additional

principal and any accrued contingent interest thereon.

The Company may redeem for cash all or a portion of the

notes at any time on or after September 11, 2006 at specified

redemption prices per one thousand dollar principal amount at

maturity of the notes.

LABORATORY CORPORATION OF AMERICA

Notes to Consolidated Financial Statements