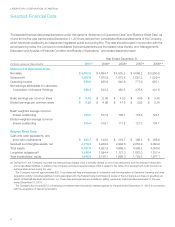

LabCorp 2010 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2010 LabCorp annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

16

LABORATORY CORPORATION OF AMERICA

Management’s Discussion and Analysis

of Financial Condition and Results of Operations

doubtful accounts at an appropriate level. The Company’s

process for determining the appropriate level of the allowance

for doubtful accounts involves judgment, and considers such

factors as the age of the underlying receivables, historical and

projected collection experience, and other external factors that

could affect the collectibility of its receivables. Accounts are

written off against the allowance for doubtful accounts based

on the Company’s write-off policy (e.g., when they are deemed

to be uncollectible). In the determination of the appropriate

level of the allowance, accounts are progressively reserved

based on the historical timing of cash collections relative to their

respective aging categories within the Company’s receivables.

These collection and reserve processes, along with the close

monitoring of the billing process, help reduce the risks of

material revisions to reserve estimates resulting from adverse

changes in collection or reimbursement experience. The

following table presents the percentage of the Company’s

net accounts receivable outstanding by aging category at

December 31, 2010 and 2009:

Days Outstanding

2010 2009

0 – 30 51.1% 47.7%

31 – 60 17.5% 16.8%

61 – 90 9.7% 10.5%

91 – 120 7.2% 6.8%

121 – 150 4.0% 4.4%

151 – 180 3.7% 4.0%

181 – 270 5.8% 7.8%

271 – 360 0.9% 1.7%

Over 360 0.1% 0.3%

The above table excludes the Ontario operation’s percentage

of net accounts receivable outstanding by aging category. The

provincial government is the primary customer of the Ontario

operation. The Company believes that including the aging for

Ontario would not be representative of the majority of the

accounts receivable by aging category for the Company.

Pension Expense

In October 2009, the Company received approval from its Board

of Directors to freeze any additional service-based credits for any

years of service after December 31, 2009 on the Company

Plan and the PEP. Both plans have been closed to new partici-

pants. Employees participating in the Company Plan and the

PEP no longer earn service-based credits, but continue to

earn interest credits. In addition, effective January 1, 2010,

all employees eligible for the defined contribution retirement

plan (the “401K Plan”) receive a minimum 3% non-elective

contribution (“NEC”) concurrent with each payroll period.

The 401K Plan also permits discretionary contributions by

the Company of 1% to 3% of pay for eligible employees based

on service.

The Company Plan covers substantially all employees hired

prior to December 31, 2009. The benefits to be paid under the

Company Plan are based on years of credited service through

December 31, 2009, interest credits and average compensa-

tion. The Company also has the PEP which covers its senior

management group. Prior to 2010, the PEP provided for the

payment of the difference, if any, between the amount of any

maximum limitation on annual benefit payments under the

Employee Retirement Income Security Act of 1974 and the

annual benefit that would be payable under the Company

Plan but for such limitation.

The Company’s net pension cost is developed from actuarial

valuations. Inherent in these valuations are key assumptions,

including discount rates and expected return on plan assets,

which are updated on an annual basis at the beginning of

each year. The Company is required to consider current market

conditions, including changes in interest rates, in making these

assumptions. Changes in pension costs may occur in the future

due to changes in these assumptions. The key assumptions

used in accounting for the defined benefit retirement plans

were a 5.1% discount rate and a 7.5% expected long-term

rate of return on plan assets as of December 31, 2010.

Discount Rate

The Company evaluates several approaches toward setting

the discount rate assumption that is used to value the benefit

obligations of its retirement plans. At year-end, priority was given

to use of the Citigroup Pension Discount Curve and anticipated

cash outflows of each retirement plan were discounted with

the spot yields from the Citigroup Pension Discount Curve. A

single-effective discount rate assumption was then determined

for each retirement plan based on this analysis. A one percentage

point decrease or increase in the discount rate would have resulted

in a respective increase or decrease in 2010 retirement plan

expense of $1.5.