LabCorp 2011 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2011 LabCorp annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

12

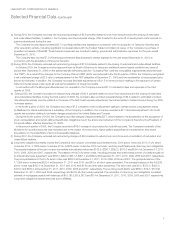

LABORATORY CORPORATION OF AMERICA

Management’s Discussion and Analysis

of Financial Condition and Results of Operations (in millions)

its scientific capabilities, grow esoteric testing capabilities and

increase presence in key geographic areas.

The Company has invested a total of $50.8 over the past

three years in licensing new testing technologies (including

approximately $49.4 estimated fair market value of technol-

ogy acquired in certain acquisitions in 2010 and 2009) and

had $66.2 net book value of capitalized patents, licenses

and technology as of December 31, 2011. While the

Company continues to believe its strategy of entering into

licensing and technology distribution agreements with the

developers of leading-edge technologies will provide future

growth in revenues, there are certain risks associated with

these investments. These risks include, but are not limited

to, the failure of the licensed technology to gain broad

acceptance in the marketplace and/or that insurance

companies, managed care organizations, or Medicare and

Medicaid will not approve reimbursement for these tests at

a level commensurate with the costs of running the tests.

Any or all of these circumstances could result in impairment

in the value of the related capitalized licensing costs.

Financing Activities

On December 21, 2011, the Company entered into a Credit

Agreement (the “Credit Agreement”) providing for a five-year

$1,000.0 senior unsecured revolving credit facility (the

“Revolving Credit Facility”) with Bank of America, N.A., acting

as Administrative Agent, Barclays Capital as Syndication

Agent, and a group of financial institutions as lending parties.

As part of the new Revolving Credit Facility, the Company

repaid all of the outstanding balances of $318.8 on its existing

term loan facility and $235.0 on its existing revolving credit

facility. In conjunction with the repayment and cancellation

of its old credit facility, the Company recorded approximately

$1.0 of remaining unamortized debt costs as interest expense

in the accompanying Consolidated Statements of Operations

for the year ended December 31, 2011. The balances out-

standing on the Company’s Revolving Credit Facility at

December 31, 2011 and December 31, 2010 were $560.0

and $0.0, respectively. The Revolving Credit Facility bears

interest at varying rates based upon a base rate or LIBOR plus

(in each case) a percentage based on the Company’s debt

rating with Standard & Poor’s and Moody’s Ratings Services.

The Revolving Credit Facility is available for general

corporate purposes, including working capital, capital expen-

ditures, acquisitions, funding of share repurchases and other

restricted payments permitted under the Credit Agreement.

The Credit Agreement also contains limitations on aggregate

subsidiary indebtedness and a debt covenant that requires

that the Company maintain on the last day of any period for

four consecutive fiscal quarters, in each case taken as one

accounting period, a ratio of total debt to consolidated

EBITDA (Earnings Before Interest, Taxes, Depreciation, and

Amortization) of not more than 3.0 to 1.0. The Company was

in compliance with all covenants in the Credit Agreement at

December 31, 2011.

As of December 31, 2011, the effective interest rate on the

Revolving Credit Facility was 1.26%.

The interest rate swap agreement to hedge variable interest

rate risk on the Company’s variable interest rate term loan

expired on March 31, 2011. On a quarterly basis under the

swap, the Company paid a fixed rate of interest (2.92%) and

received a variable rate of interest based on the three-month

LIBOR rate on an amortizing notional amount of indebtedness

equivalent to the term loan balance outstanding. The swap

was designated as a cash flow hedge. Accordingly, the

Company recognized the fair value of the swap in the

condensed consolidated balance sheets and any changes in

the fair value were recorded as adjustments to accumulated

other comprehensive income (loss), net of tax. The fair value

of the interest rate swap agreement was the estimated amount

that the Company would have paid or received to terminate

the swap agreement at the reporting date. The fair value of

the swap was a liability of $2.4 at December 31, 2010 and

was included in other liabilities in the respective condensed

consolidated balance sheet.

On October 28, 2010, in conjunction with the acquisition of

Genzyme Genetics, the Company entered into a $925.0 Bridge

Term Loan Credit Agreement, among the Company, the lenders

named therein and Citibank, N.A., as administrative agent (the

“Bridge Facility”). The Company replaced and terminated the

Bridge Facility in November 2010 by making an offering in the

debt capital markets. On November 19, 2010, the Company

sold $925.0 in debt securities, consisting of $325.0 aggregate

principal amount of 3.125% Senior Notes due May 15, 2016 and

$600.0 aggregate principal amount of 4.625% Senior Notes due

November 15, 2020. Beginning on May 15, 2011, interest on the

Senior Notes due 2016 and 2020 is payable semi-annually on

May 15 and November 15. On December 1, 2010, the acquisi-

tion of Genzyme Genetics was funded by the proceeds from the

issuance of these Notes ($915.4) and with cash on hand.