LabCorp 2011 Annual Report Download - page 16

Download and view the complete annual report

Please find page 16 of the 2011 LabCorp annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

14

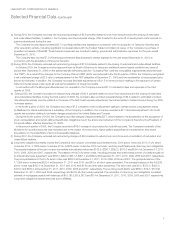

LABORATORY CORPORATION OF AMERICA

Management’s Discussion and Analysis

of Financial Condition and Results of Operations (in millions)

Off-Balance Sheet Arrangements

The Company does not have transactions or relationships

with “special purpose” entities, and the Company does not

have any off balance sheet financing other than normal

operating leases.

Other Commercial Commitments

As of December 31, 2011, the Company provided letters of

credit aggregating approximately $37.4, primarily in connec-

tion with certain insurance programs. Letters of credit provided

by the Company are secured by the Company’s Revolving

Credit Facility and are renewed annually, around mid-year.

The partnership units of the holders of the noncontrolling

interest in the Ontario, Canada (“Ontario”) joint venture were

acquired by the Company on February 8, 2010 for $137.5.

On February 17, 2010, the Company completed a transaction

to sell the units acquired from the previous noncontrolling

interest holder to a new Canadian partner for the same price.

As a result of this transaction, the Company recorded a

component of noncontrolling interest in other liabilities and

a component in mezzanine equity. Upon the completion of

these two transactions, the Company’s financial ownership

percentage in the joint venture partnership remained

unchanged at 85.6%. Concurrent with the sale to the new

partner, the partnership agreement for the Ontario joint venture

was amended and restated with substantially the same terms

as the previous agreement.

On October 14, 2011, the Company issued notice to a

noncontrolling interest holder in the Ontario joint venture of its

intent to purchase the holder’s partnership units in accordance

with the terms of the joint venture’s partnership agreement. On

November 28, 2011, this purchase was completed for a total

purchase price of CN$151.7 as outlined in the partnership

agreement (CN$147.8 plus certain adjustments relating to

cash distribution hold backs made to finance recent business

acquisitions and capital expenditures). The purchase of these

additional partnership units brings the Company’s percentage

interest owned to 98.2%.

The contractual value of the remaining noncontrolling

interest put, in excess of the current noncontrolling interest of

$3.6, totals $16.6 at December 31, 2011. At December 31,

2011 and 2010, $20.2 and $20.6, respectively, have been

classified as mezzanine equity in the Company’s condensed

consolidated balance sheet.

At December 31, 2011, the Company was a guarantor on

approximately $0.9 of equipment leases. These leases were

entered into by a joint venture in which the Company owns a 50%

interest and have a remaining term of approximately two years.

Based on current and projected levels of operations,

coupled with availability under its Revolving Credit Facility,

the Company believes it has sufficient liquidity to meet both

its anticipated short-term and long-term cash needs; however,

the Company continually reassesses its liquidity position in

light of market conditions and other relevant factors.

New Accounting Pronouncements

In September 2011, the FASB issued authoritative guidance

to amend and simplify the rules related to testing goodwill for

impairment. The revised guidance allows an entity to make an

initial qualitative evaluation, based on the entity’s events and

circumstances, to determine whether it is more likely than not

that the fair value of a reporting unit is less than its carrying

amount. The results of this qualitative assessment determine

whether it is necessary to perform the currently required

two-step impairment test. The new guidance is effective for

annual and interim goodwill impairment tests performed for

fiscal years beginning after December 15, 2011, with early

adoption permitted. Adoption of this guidance is not expected

to have a material impact on the Company’s consolidated

financial statements.

In July 2011, the FASB issued authoritative guidance on the

presentation and disclosure of patient service revenue, provision

for bad debts, and the allowance for doubtful accounts for

certain health care entities. This literature was issued to

provide greater transparency about a health care entity’s net

patient service revenue and the related allowance for doubtful

accounts. Specifically, this literature requires the provision for

bad debts associated with patient service revenue to be sepa-

rately displayed on the face of the statement of operations as a

component of net revenue for health care entities that provide

services regardless of a patient’s ability to pay. The guidance

also requires enhanced disclosures of significant changes in

estimates in the provision for bad debts relating to patient

services when an entity recognizes revenue regardless of a

patient’s ability to pay. This guidance is effective for fiscal years

and interim periods beginning after December 15, 2011, with

early adoption permitted. The Company does not believe the

adoption of the authoritative guidance in the first quarter of 2012

will have an impact on its consolidated financial statements.