Lowe's 2013 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2013 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

|

|

21

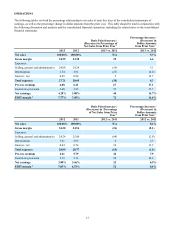

SG&A – The 84 basis point decrease in SG&A expense as a percentage of sales from 2011 to 2012 was primarily driven by 81

basis points of leverage due to long-lived asset impairment and other costs associated with the 27 store closures and

discontinued projects in 2011. We also experienced approximately 35 basis points of leverage associated with our proprietary

credit program, which was driven by increased portfolio income as a result of continued growth in the program. These were

partially offset by deleverage of approximately 15 basis points associated with incentive compensation, due to higher

attainment levels compared to targets for store-based employees relative to last year. In addition, we experienced nine basis

points of deleverage in contract labor associated with information technology projects to improve customer experiences.

Depreciation – Depreciation expense deleveraged six basis points for 2012 compared to 2011 primarily due to higher

depreciation associated with IT capital investments made to improve customer experiences, which have shorter average useful

lives. Property, less accumulated depreciation, decreased to $21.5 billion at February 1, 2013 compared to $22.0 billion at

February 3, 2012. At February 1, 2013 and February 3, 2012 we owned 89% of our stores, which included stores on leased

land.

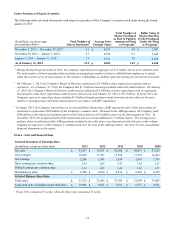

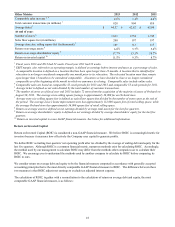

Interest – Net – Net interest expense is comprised of the following:

(In millions)

2012

2011

Interest expense, net of amount capitalized

$

427

$

379

Amortization of original issue discount and loan costs

5

4

Interest income

(9

)

(12

)

Interest - net

$

423

$

371

Net interest expense increased primarily as a result of the issuance of $1.0 billion and $2.0 billion of unsecured notes in

November 2011 and April 2012, respectively, partially offset by favorable tax settlements that resulted in a reduced interest

accrual during 2012.

Income tax provision – Our effective income tax rate was 37.6% in 2012 compared to 36.7% in 2011. The lower effective tax

rate in 2011 was the result of the recognition of one-time federal employee retention benefits from the federal HIRE (Hiring

Incentives to Restore Employment) retention tax credit, as well as the favorable settlement of certain state tax matters in the

third quarter of 2011.

LOWE’S BUSINESS OUTLOOK

As of February 26, 2014, the date of our fourth quarter 2013 earnings release, we expected total sales in 2014 to increase

approximately 5% and comparable sales to increase approximately 4%. We expected to open approximately 15 home

improvement stores and five Orchard stores during 2014. In addition, earnings before interest and taxes as a percentage of

sales (operating margin) were expected to increase approximately 65 basis points, and the effective tax rate was expected to be

approximately 38.1%. Diluted earnings per share of $2.60 were expected for the fiscal year ending January 30, 2015. Our

guidance assumed approximately $3.4 billion in share repurchases during 2014, spread evenly across the four quarters.

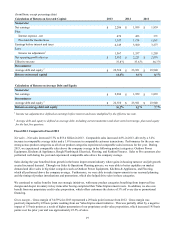

FINANCIAL CONDITION, LIQUIDITY AND CAPITAL RESOURCES

Cash Flows

Cash flows from operating activities continued to provide the primary source of our liquidity. The increase in net cash

provided by operating activities for 2013 versus 2012 was primarily driven by an increase in net earnings. The increase in net

cash used in investing activities for 2013 versus 2012 was driven by a decrease in the net cash flows from purchase and sale of

investments and the acquisition of Orchard, partially offset by a decrease in capital expenditures. The decrease in net cash used

in financing activities for 2013 was driven primarily by a decrease in cash used to repurchase shares, which included shares

repurchased under our share repurchase program and shares withheld from employees to satisfy statutory tax withholding

liabilities upon vesting of restricted stock awards, the repayment of unsecured notes that matured in the prior year, and an

increase in short-term borrowings in the current year. These were partially offset by a decrease in cash provided by the

issuance of long term-debt as a result of the issuance of $1.0 billion of unsecured notes in September 2013 versus the issuance

of $2.0 billion of unsecured notes in April 2012.