Lowe's 2013 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2013 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

|

|

38

lease, the Company depreciates these leasehold improvements over the shorter of the useful life of the leasehold assets or a

term that includes lease renewal periods deemed to be reasonably assured at the time the leasehold improvements are placed

into service. The amortization of these assets is included in depreciation expense in the consolidated financial statements.

Long-Lived Asset Impairment/Exit Activities - The carrying amounts of long-lived assets are reviewed whenever certain

events or changes in circumstances indicate that the carrying amounts may not be recoverable. A potential impairment has

occurred for long-lived assets held-for-use if projected future undiscounted cash flows expected to result from the use and

eventual disposition of the assets are less than the carrying amounts of the assets. An impairment loss is recorded for long-

lived assets held-for-use when the carrying amount of the asset is not recoverable and exceeds its fair value.

Excess properties that are expected to be sold within the next 12 months and meet the other relevant held-for-sale criteria are

classified as long-lived assets held-for-sale. Excess properties consist primarily of retail outparcels and property associated

with relocated or closed locations. An impairment loss is recorded for long-lived assets held-for-sale when the carrying amount

of the asset exceeds its fair value less cost to sell. A long-lived asset is not depreciated while it is classified as held-for-sale.

For long-lived assets to be abandoned, the Company considers the asset to be disposed of when it ceases to be used. Until it

ceases to be used, the Company continues to classify the asset as held-for-use and tests for potential impairment accordingly. If

the Company commits to a plan to abandon a long-lived asset before the end of its previously estimated useful life, its

depreciable life is re-evaluated.

The Company recorded long-lived asset impairment losses of $46 million during 2013, including $26 million for operating

locations, $17 million for excess properties classified as held-for-use and $3 million, including costs to sell, for excess

properties classified as held-for-sale. The Company recorded impairment losses of $77 million in 2012, including $55 million

for operating locations, $17 million for excess properties classified as held-for-use and $5 million, including costs to sell, for

excess properties classified as held-for-sale. The Company recorded long-lived asset impairment of $388 million during 2011,

including $40 million for operating locations, $269 million for locations identified for closure, $78 million for excess properties

classified as held-for-use and $1 million, including costs to sell, for excess properties classified as held-for-sale. Impairment

losses are included in SG&A expense in the consolidated statements of earnings. Fair value measurements associated with

long-lived asset impairments are further described in Note 2 to the consolidated financial statements.

During 2011, the Company closed 27 underperforming stores across the United States. These decisions were the result of the

Company’s realignment of its store operations structure and its continued efforts to focus resources in a manner that would

generate the greatest shareholder value. Total impairment losses for locations identified for closure for 2011 relate to these

store closings.

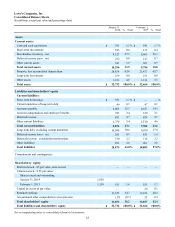

The net carrying amount of excess properties that do not meet the held-for-sale criteria is included in other assets (noncurrent)

on the consolidated balance sheets and totaled $204 million and $218 million at January 31, 2014 and February 1, 2013,

respectively.

When locations under operating leases are closed, a liability is recognized for the fair value of future contractual obligations,

including future minimum lease payments, property taxes, utilities, common area maintenance and other ongoing expenses, net

of estimated sublease income and other recoverable items. When the Company commits to an exit plan and communicates that

plan to affected employees, a liability is recognized in connection with one-time employee termination benefits. Subsequent

changes to the liabilities, including a change resulting from a revision to either the timing or the amount of estimated cash

flows, are recognized in the period of change. Expenses associated with exit activities are included in SG&A expense in the

consolidated statement of earnings.

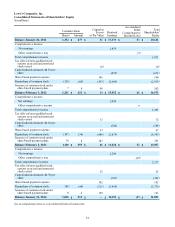

Equity Method Investments - The Company’s investments in certain unconsolidated entities are accounted for under the

equity method. The balance of these investments is included in other assets (noncurrent) in the accompanying consolidated

balance sheets. The balance is increased to reflect the Company’s capital contributions and equity in earnings of the

investees. The balance is decreased to reflect its equity in losses of the investees and for distributions received that are not in

excess of the carrying amount of the investments. Equity in earnings and losses of the investees has been immaterial and is

included in SG&A expense.

Leases - For lease agreements that provide for escalating rent payments or free-rent occupancy periods, the Company

recognizes rent expense on a straight-line basis over the non-cancellable lease term and option renewal periods where failure to

exercise such options would result in an economic penalty in such amount that renewal appears, at the inception of the lease, to

be reasonably assured. The lease term commences on the date that the Company takes possession of or controls the physical

use of the property. Deferred rent is included in other liabilities (noncurrent) on the consolidated balance sheets.