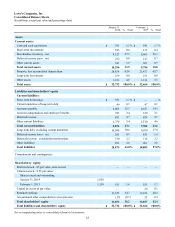

Lowe's 2013 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2013 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

|

|

43

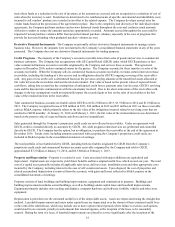

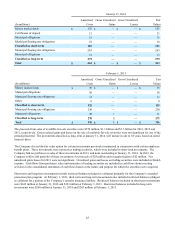

market inputs. The inputs to the pricing models were typically benchmark yields, reported trades, broker-dealer quotes, issuer

spreads and benchmark securities, among others.

Assets and Liabilities that are Measured at Fair Value on a Nonrecurring Basis

For the years ended January 31, 2014 and February 1, 2013, the Company’s only significant assets or liabilities measured at fair

value on a nonrecurring basis subsequent to their initial recognition were certain assets subject to long-lived asset impairment.

The Company reviews the carrying amounts of long-lived assets whenever certain events or changes in circumstances indicate

that the carrying amounts may not be recoverable. With input from store operations, the Company’s accounting and finance

personnel that organizationally report to the chief financial officer, assess the performance of retail stores quarterly against

historical patterns and projections of future profitability for evidence of possible impairment. An impairment loss is recognized

when the carrying amount of the asset (disposal) group is not recoverable and exceeds its fair value. The Company estimated

the fair values of assets subject to long-lived asset impairment based on the Company’s own judgments about the assumptions

that market participants would use in pricing the assets and on observable market data, when available. The Company

classified these fair value measurements as Level 3.

In the determination of impairment for operating locations, the Company determined the fair values of individual operating

locations using an income approach, which required discounting projected future cash flows. When determining the stream of

projected future cash flows associated with an individual operating location, management made assumptions, incorporating

local market conditions and inputs from store operations, about key variables including the following unobservable inputs:

sales growth rates, gross margin, controllable expenses, such as payroll and occupancy expense, and asset residual values. In

order to calculate the present value of those future cash flows, the Company discounted cash flow estimates at a rate

commensurate with the risk that selected market participants would assign to the cash flows. In general, the selected market

participants represented a group of other retailers with a location footprint similar in size to the Company’s.

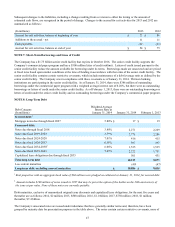

During 2013, 15 operating locations experienced a triggering event and were evaluated for recoverability. One of the 15

operating locations was determined to be impaired due to a decline in recent cash flow trends and an unfavorable sales outlook,

resulting in an impairment loss of $26 million. The discounted cash flow model used to estimate the fair value of the impaired

operating location assumed average annual sales growth rates ranging from 2.0% to 5.0% over the remaining life of the

location and applied a discount rate of approximately 6%.

The remaining 14 operating locations that experienced a triggering event during 2013 were determined to be recoverable and,

therefore, were not impaired. For 11 of these 14 locations, the expected undiscounted cash flows substantially exceeded the net

book value of the location’s assets. A 10% reduction in projected sales used to estimate future cash flows at the latest date

these 11 operating locations were evaluated for impairment would have resulted in the impairment of four of these locations

and increased recognized impairment losses by $39 million.

Three of the operating locations with a net book value of $25 million had expected undiscounted cash flows that exceeded the

net book value of its assets by less than a substantial amount. A 10% reduction in projected sales used to estimate future cash

flows at the date these operating locations were evaluated for impairment would have resulted in the impairment of these three

locations and increased recognized impairment losses by $23 million.

We analyzed other assumptions made in estimating the future cash flows of the operating locations evaluated for impairment,

but the sensitivity of those assumptions was not significant to the estimates.

In the determination of impairment for excess properties held-for-use and held-for-sale, which consisted of retail outparcels and

property associated with relocated or closed locations, the fair values were determined using a market approach based on

estimated selling prices. The Company determined the estimated selling prices by obtaining information from property brokers

or appraisers in the specific markets being evaluated or negotiated non-binding offers to purchase. The information obtained

from property brokers or appraisers included comparable sales of similar assets and assumptions about demand in the market

for these assets.

During 2013, the Company incurred total impairment charges of $19 million for 42 excess property locations. A 10%

reduction in the estimated selling prices for these excess properties at the dates the locations were evaluated for impairment

would have increased impairment losses by approximately $6 million.