Proctor and Gamble 1999 Annual Report Download - page 23

Download and view the complete annual report

Please find page 23 of the 1999 Proctor and Gamble annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

|

|

The Procter & Gamble Company and Subsidiaries

19

LATIN AMERICA REGION

Latin America continued to deliver solid results,

despite a challenging economic environment,

with record sales, unit volume and net earnings.

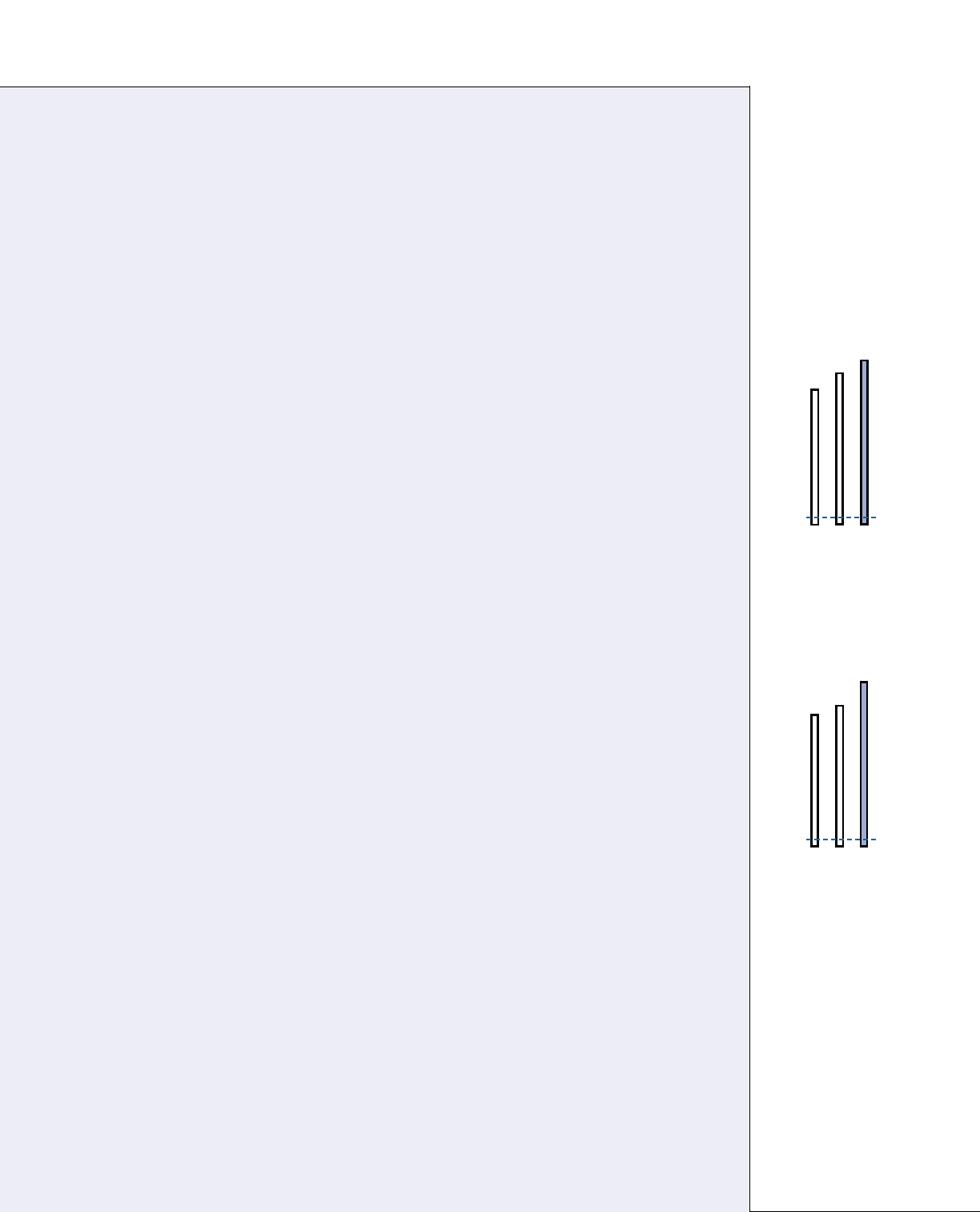

Net sales in the region grew 7% to $2.83 bil-

lion on 3% unit volume growth, as inflation-

targeted pricing outpaced the negative impact of

currency devaluation, primarily in Mexico and

Venezuela. Strong volume progress in laundry and

snacks supplemented the prior year acquisition

of Loreto y Peña, a paper company in Mexico,

and the buyout of a paper joint venture in the

Southern Cone. Laundry results reflect the strength-

ening of the base business in Mexico and the launch

of Ariel in the Southern Cone. In the prior year,

sales for the region grew 14% to $2.64 billion on

12% unit volume growth, reflecting acquisitions,

strength in the base business and pricing.

For the current year, net earnings for the

region were $318 million, a 16% increase. Mexico,

Venezuela and Central America achieved double-

digit earnings growth, and more than offset the

heavy investment in the laundry expansion in the

Southern Cone. Earnings surpassed sales as a result

of cost reductions and tax benefits generated from

inflationary markets. Prior year net earnings were

$274 million, a 7% increase over 1997, despite

increased initiative spending. Net earnings margin

for the current year was 11.3% compared to 10.4%

and 11.1% in 1998 and 1997, respectively.

In Mexico, the Company’s largest operation

in the region, business results were strong. Unit

volume increased 7%, behind a strong base busi-

ness, prior year acquisitions and a general upturn

in the consumer market. Prior year results were

also strong, behind acquisitions and favorable

economic conditions.

The balance of the region’s volume fell 1%,

driven by the economic situation in Brazil.

However, Chile and Argentina achieved double-

digit volume increases over 1998, behind the prior

year acquisition and the expansion of Ariel into the

Southern Cone.

Prior to January 1, 1998, both Brazil and Peru

were highly inflationary economies, and accord-

ingly, the results of the Company’s subsidiaries

in Brazil and Peru were measured using the

United States dollar as their functional currency.

Effective January 1, 1998, neither Brazil nor Peru

qualified as a highly inflationary economy. The

impact of this change was not material to the

Company’s earnings.

HEDGING AND DERIVATIVE

FINANCIAL INSTRUMENTS

The Company is exposed to market risk, includ-

ing changes in interest rates, currency exchange

rates and commodity prices. To manage the

volatility relating to these exposures, the Company

nets the exposures on a consolidated basis to take

advantage of natural offsets and enters into various

derivative transactions for the residual portion

pursuant to the Company’s policies in areas such

as counterparty exposure and hedging practices.

The financial impacts of these hedging instru-

ments are offset in part or in whole by corre-

sponding changes in the underlying exposures

being hedged. The Company does not hold or

issue derivative financial instruments for trading

purposes. Note 6 to the consolidated financial

statements includes a discussion of the Company’s

accounting policies for financial instruments.

Derivative positions are monitored using

techniques including market value, sensitivity

analysis and value at risk modeling. The tests for

interest rate and currency rate exposures discussed

below are based on a variance/co-variance value at

risk model using a one year horizon and a 95%

confidence level. The model incorporates the

impact of correlation and diversification from

holding multiple currency and interest rate

instruments, and assumes that financial returns

are normally distributed, and approximates the

financial return for options and other non-linear

instruments. Estimates of volatility and corre-

lations of market factors are drawn from the

RiskMetrics™ dataset as of June 30, 1999. In

cases where data is unavailable in RiskMetrics™

a reasonable proxy is included.

The Company’s market risk exposures rela-

tive to interest and currency rates, as discussed

below, have not changed materially versus the

previous reporting period. In addition, the

Company is not aware of any facts or circum-

stances that would significantly impact such

exposures in the near-term.

2.3

2.6

2.8

’97 ’98 ’99

LATIN AMERICA

NET SALES

Billions of Dollars

256

274

318

’97 ’98 ’99

LATIN AMERICA

NET EARNINGS

Millions of Dollars