Proctor and Gamble 1999 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 1999 Proctor and Gamble annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

|

|

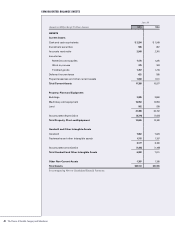

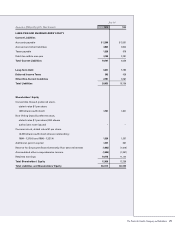

The Procter & Gamble Company and Subsidiaries

37

Millions of Dollars Except Per Share Amounts

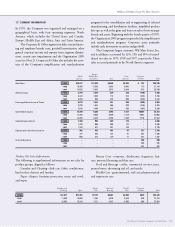

Currency instruments outstanding are as follows:

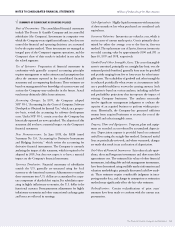

June 30

1999 1998

Notional amount

Forward contracts $1,988 $3,448

Purchased options 1,358 1,262

Currency swaps 33 217

Fair value

Forward contracts $ (6) $30

Purchased options 19 16

Currency swaps 58

The reduction in the notional amount of forward

contracts reflects the introduction of the euro and increased

efficiencies in our hedge program. The deferred gains and

losses on these instruments were not material.

In addition, in order to hedge currency exposures related

to the net investments in foreign subsidiaries, the Company

utilizes local currency financing entered into by the

subsidiaries, and currency interest rate swaps and other foreign

currency denominated financing instruments entered into by

the parent. Gains and losses on instruments designated as

hedges of net investments are offset against the translation

effects reflected in shareholders’ equity.

Currency interest rate swaps, foreign currency instruments

and foreign currency denominated debt that have been desig-

nated as hedges of the Company’s net investment exposure in

certain foreign subsidiaries have notional amounts totaling

$826 and $1,138 at June 30, 1999 and 1998, respectively. These

hedges resulted in gains of $5 and $42, net of $4 and $25 in

tax effects, reflected in shareholders’ equity.

Credit Risk

Credit risk arising from the inability of a counterparty to meet

the terms of the Company’s financial instrument contracts is

generally limited to the amounts, if any, by which the coun-

terparty’s obligations exceed the obligations of the Company.

It is the Company’s policy to enter into financial instruments

with a diversity of creditworthy counterparties. Therefore, the

Company does not expect to incur material credit losses on its

risk management or other financial instruments.

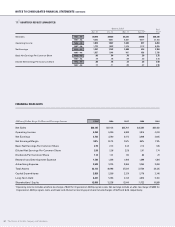

7STOCK OPTIONS

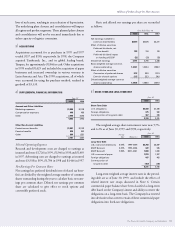

The Company has stock-based compensation plans under

which stock options are granted annually to key managers and

directors at the market price on the date of grant. The 1999

grants are fully exercisable after three years and have a fifteen

year life, while prior years’ grants are fully exercisable after one

year and have a ten year life. In 1998, the Company granted

stock options to all eligible employees not covered by the key

manager and director plans. These grants, which comprised

8.7 million of the 20.3 million options granted in 1998, are

fully exercisable after five years and have a ten year life. The

Company issues stock appreciation rights in countries where

stock options have not been approved by local governments.

Pursuant to FASB Statement No. 123, “Accounting for

Stock-Based Compensation,” the Company has elected to

account for its employee stock option plans under APB

Opinion No. 25, “Accounting for Stock Issued to

Employees.” Accordingly, compensation cost has not been

recognized for stock options issued under these plans. Had

compensation cost for the plans been determined based on

the fair value at the grant date consistent with FASB

Statement No. 123, the Company’s net earnings and earnings

per share would have been as follows:

Years Ended June 30

1999 1998 1997

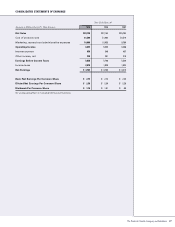

Net earnings

As reported $3,763 $3,780 $3,415

Pro forma 3,683 3,472 3,305

Net earnings per common share

Basic

As reported $ 2.75 $ 2.74 $ 2.43

Pro forma 2.69 2.51 2.35

Diluted

As reported 2.59 2.56 2.28

Pro forma 2.53 2.35 2.20

The fair value of each option grant is estimated on the

date of grant using a binomial option-pricing model with the

following weighted average assumptions:

Years Ended June 30

1999 1998 1997

Interest rate 5.4% 5.6% 6.6%

Dividend yield 1.5% 2% 2%

Expected volatility 26% 26% 22%

Expected life in years 766