Proctor and Gamble 2002 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2002 Proctor and Gamble annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

|

|

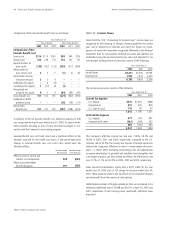

34 The Procter & Gamble Company and Subsidiaries

Asset Write-Downs

Asset write-downs relate to the establishment of new carrying values

for assets held for sale or disposal. These assets represent excess

capacity in the process of being removed from service or disposed as

well as businesses held for sale in the next 12 months. These assets

were written down to the amounts expected to be realized upon sale or

disposal, less minor disposal costs.

Additionally, asset write-downs include certain manufacturing assets

that are expected to operate at levels significantly below their planned

capacity, primarily capital expansions related to recent initiatives that

have not met expectations. The projected cash flows from such assets

over their remaining useful lives are no longer estimated to be greater

than their current carrying values; therefore, they were written down to

estimated fair value, generally determined by reference to discounted

expected future cash flows. Such before-tax charges represented

approximately $45 in 2002, $160 in 2001 and $0 in 2000.

Accelerated Depreciation

Charges for accelerated depreciation relate to long-lived assets that will

be taken out of service prior to the end of their normal service period

due to manufacturing consolidations, technology standardization, plant

closures or strategic choices to discontinue initiatives. The Company has

shortened the estimated useful lives of such assets, resulting in

incremental depreciation expense.

Other Restructuring Charges

Other costs incurred as a direct result of the program include

relocation, training, certain costs associated with discontinuation of

initiatives and the establishment of global business services and the

new legal and organization structure.

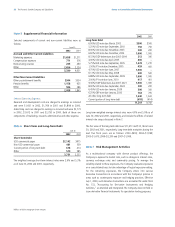

Note 3 Acquisitions and Spin-off

Acquisitions

The purchase method of accounting was used for acquisitions in all

periods presented. In 2002, acquisitions totaled $5.5 billion, resulting in

additions to goodwill of $3.6 billion and other intangible assets of $1.7

billion (see Note 4). These acquisitions consisted primarily of Clairol

along with an incremental payment for Dr. John’s Spinbrush.

On November 16, 2001, the Company completed the acquisition of

the Clairol business from the Bristol-Myers Squibb Company for

approximately $5.0 billion in cash, financed primarily with debt. Total

cash paid includes final purchase price adjustments based on a working

capital formula. The Clairol business consists of hair care, hair colorants

and personal care products, giving the Company entry into the hair

colorant market, while providing potential for significant synergies. The

operating results of the Clairol business are reported in the Company’s

beauty care segment from November 16, 2001.

The following table provides pro forma results of operations for the

years ended June 30, 2002, 2001 and 2000, as if Clairol had been

acquired as of the beginning of each fiscal year presented. The pro

forma results include adjustments for estimated interest expense on

acquisition debt and amortization of intangible assets, excluding

goodwill and indefinite-lived intangibles. However, pro forma results do

not include any anticipated cost savings or other effects of the planned

integration of Clairol. Accordingly, such amounts are not necessarily

indicative of the results that would have occurred if the acquisition had

closed on the dates indicated, or that may result in the future.

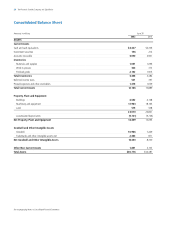

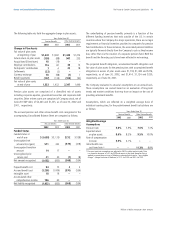

The initial purchase price allocation of the Clairol business resulted in

the following condensed balance sheet of assets acquired and liabilities

assumed. It is anticipated that there will be changes to the initial

allocation as fair values are finalized next quarter, but the Company

does not expect these changes to have a material impact on the results

of operations or financial condition of the Company in future periods.

The Clairol acquisition resulted in $1,533 in total intangible assets

acquired with $1,220 allocated to trademarks with indefinite lives. The

remaining $313 of acquired intangibles have determinable useful lives

and were assigned to trademarks of $128, patents and technology of

$146 and other intangible assets of $39. Total intangible assets

acquired with determinable lives have a weighted average useful life of

9 years (11 years for trademarks, 9 years for patents and technology

and 5 years for other intangible assets).

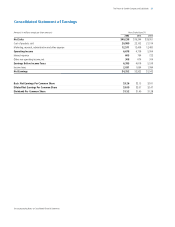

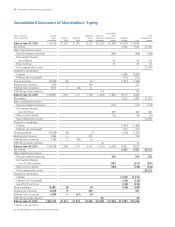

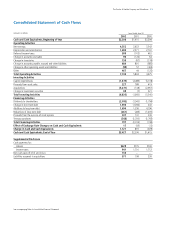

Notes to Consolidated Financial Statements

Millions of dollars except per share amounts

$40,801

2,927

$2.07

$41,488

3,517

$2.45

$40,780

4,406

$3.13

2002

Net sales

Net earnings

Diluted net earnings per common share

Years Ended June 30

Pro forma results

2000

2001

$487

184

1,533

3,300

18

5,522

450

47

497

5,025

Current assets

Property, plant and equipment

Intangible assets

Goodwill (1)

Other non-current assets

Total assets acquired

Current liabilities

Non-current liabilities

Total liabilities assumed

Net assets acquired

(1) Approximately $2.6 billion is expected to be deductible for tax purposes.

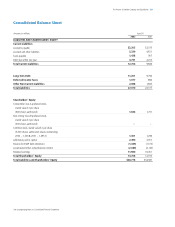

Opening Balance