Safeway 1997 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 1997 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

|

|

17

Vons’ operating and administrative expense ratio has historically

been higher than Safeway’s (partially due to the high cost of real

estate and labor in southern California). In addition, goodwill

amortization has increased by approximately $30 million as a

result of the Merger. On a pro forma basis, operating and

administrative expense declined 35 basis points to 22.95%

of sales in 1997, from 23.30% in 1996.

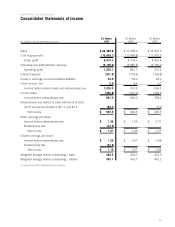

Interest Expense Interest expense increased to $241.2 million in

1997 from $178.5 million in 1996 because of the debt incurred

during the second quarter of 1997 to repurchase stock in con-

junction with the Merger.

During 1997, Safeway recorded an extraordinary loss of $64.1

million ($0.13 per share) for the repurchase of $589.0 million of

Safeway’s public debt, $285.5 million of Vons’ public debt, and

$40.0 million of medium-term notes. The extraordinary loss rep-

resents the payment of premiums on retired debt and the write-

off of deferred finance costs, net of the related tax benefits.

Safeway financed this repurchase with a public offering of $600

million of senior debt securities and the balance with commercial

paper. The refinancing extends Safeway’s overall long-term debt

maturities, increases financial flexibility and, based on current

interest rates, is expected to reduce annual interest expense.

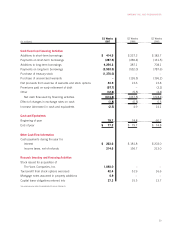

In May 1997, Safeway entered into interest rate cap agree-

ments which expire in 1999 and entitle the Company to receive

from counterparties the amounts, if any, by which interest at

LIBOR on an $850 million notional amount exceeds 7%. The

unamortized cost to purchase the cap agreements was $2.5

million at year-end 1997.

As of year-end 1997, the Company had effectively converted

$135.1 million of its floating rate debt to fixed interest rate debt

through the use of interest rate swap agreements. Interest rate

swap and cap agreements increased interest expense by $3.3

million in 1997, $3.0 million in 1996 and $0.3 million in 1995.

The significant terms of swap and cap agreements outstanding

at year-end 1997 are described in Note E to the Company’s

1997 consolidated financial statements.

Equity in Earnings of Unconsolidated Affiliates Safeway’s invest-

ment in unconsolidated affiliates consists of a 49% ownership

interest in Casa Ley, S.A. de C.V. (“Casa Ley”), which operates

74 food and general merchandise stores in western Mexico.

Through the first quarter of 1997, Safeway also held a 34.4%

interest in Vons. Safeway records its equity in earnings of

unconsolidated affiliates on a one-quarter delay basis.

Income from Safeway’s equity investment in Casa Ley

increased to $22.7 million in 1997 from $18.8 million in

1996 and $8.6 million in 1995. For much of 1995, Mexico

suffered from high interest rates and inflation which adversely

affected Casa Ley. Since 1996, interest rates and inflation

in Mexico moderated and Casa Ley’s financial results have

gradually improved.

Equity in earnings of unconsolidated affiliates included

Safeway’s share of Vons’ earnings of $12.2 million in the first

quarter of 1997, $31.2 million in 1996 and $18.3 million in 1995.

Liquidity and Financial Resources

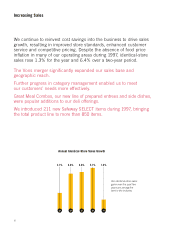

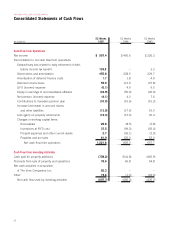

Net cash flow from operations was $1,221.6 million in 1997,

$825.2 million in 1996 and $657.7 million in 1995. Net cash

flow from operations increased in 1997 and 1996 largely due to

increased net income.

Cash flow used by investing activities was $607.7 million

in 1997, $482.3 million in 1996 and $425.7 million in 1995.

The increase in cash flow used by investing activities in 1997 is

primarily the result of increased capital expenditures to open

37 new stores, complete 181 remodels, complete construction

of a manufacturing plant in California and begin work on a new

distribution center in Maryland.

Cash flow used by financing activities was $614.6 million

in 1997, $337.5 million in 1996 and $218.4 million in 1995,

reflecting Safeway’s reduction in total debt in 1995 and 1996,

followed by increased borrowing related to the Merger in 1997.

Net cash flow from operations as presented on the

Statement of Cash Flows is an important measure of cash gen-

erated by the Company’s operating activities. Operating cash

flow, as defined below, is similar to net cash flow from opera-

tions because it excludes certain non-cash items. However,

operating cash flow also excludes interest expense and income

taxes. Management believes that operating cash flow is relevant

because it assists investors in evaluating Safeway’s ability to

service its debt by providing a commonly used measure of cash

available to pay interest. Operating cash flow also facilitates

comparisons of Safeway’s results of operations with companies

having different capital structures. Other companies may define

operating cash flow differently, and as a result, such measures

may not be comparable to Safeway’s operating cash flow.

Safeway’s computation of operating cash flow is as follows

(dollars in millions):

1997 1996 1995

Income before income taxes

and extraordinary loss $1,076.3 $ 767.6 $ 556.5

LIFO expense (income) (6.1) 4.9 9.5

Interest expense 241.2 178.5 199.8

Depreciation

and amortization 455.8 338.5 329.7

Equity in earnings of

unconsolidated affiliates (34.9) (50.0) (26.9)

■■■■

Operating cash flow $1,732.3 $1,239.5 $1,068.6

■■■■

As a percent of sales 7.70% 7.18% 6.52%

■■■■

As a multiple of interest expense 7.18x 6.94x 5.35x

■■■■

Total debt increased to $3.34 billion at year-end 1997 from

$1.98 billion at year-end 1996 due primarily to the Merger. Annual

debt maturities over the next five years are set forth in Note C of

the Company’s 1997 Consolidated Financial Statements.

Based upon the current level of operations, Safeway believes

that operating cash flow and other sources of liquidity, including

borrowings under Safeway’s commercial paper program and the

Bank Credit Agreement (defined below), will be adequate to meet

anticipated requirements for working capital, capital expendi-

tures, interest payments and scheduled principal payments for