Safeway 1997 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 1997 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

|

|

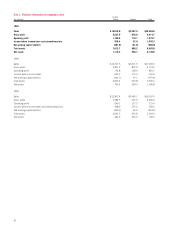

Note D: Lease Obligations

Approximately two-thirds of the premises that the Company

occupies are leased. The Company had approximately 1,310

leases at year-end 1997, including approximately 180 which are

capitalized for financial reporting purposes. Most leases have

renewal options, some with terms and conditions similar to the

original lease, others with reduced rental rates during the option

periods. Certain of these leases contain options to purchase the

property at amounts that approximate fair market value.

As of year-end 1997, future minimum rental payments applica-

ble to non-cancelable capital and operating leases with remaining

terms in excess of one year were as follows (in millions):

Capital Operating

Leases Leases

1998 $ 48.7 $ 202.3

1999 44.5 198.6

2000 39.1 189.5

2001 35.4 173.5

2002 34.3 161.1

Thereafter 282.2 1,315.7

■■■

Total minimum lease payments 484.2 $2,240.7

Less amounts representing interest (239.1)

Present value of net minimum lease

payments 245.1

Less current obligations (22.0)

Long-term obligations $ 223.1

Future minimum lease payments under non-cancelable

capital and operating lease agreements have not been reduced

by minimum sublease rental income totalling $142.7 million.

Amortization expense for property under capital leases was

$21.1 million in 1997, $17.9 million in 1996 and $18.9 million

in 1995. Accumulated amortization of property under capital

leases was $153.4 million at year-end 1997 and $156.1 million

at year-end 1996.

The following schedule shows the composition of total rental

expense for all operating leases (in millions). In general, contin-

gent rentals are based on individual store sales.

1997 1996 1995

Property leases:

Minimum rentals $206.0 $138.2 $132.7

Contingent rentals 12.3 9.9 9.1

Less rental income

from subleases (13.4) (11.1) (11.1)

■■ ■■

204.9 137.0 130.7

Equipment leases 19.3 21.0 20.8

■■ ■■

$224.2 $158.0 $151.5

■■ ■■

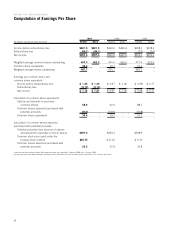

Note E: Interest Expense

Interest expense consisted of the following (in millions):

1997 1996 1995

Bank Credit Agreement $ 36.9 $ 16.4 $ 25.2

Commercial paper 43.8 ––

9.30% Senior Secured

Debentures 5.3 6.6 6.6

10% Senior Subordinated Notes 19.3 24.1 24.1

9.875% Senior Subordinated

Debentures 8.2 10.9 10.9

9.65% Senior Subordinated

Debentures 17.8 22.0 22.0

9.35% Senior Subordinated Notes 12.3 15.3 16.1

7.45% Senior Debentures 3.4 ––

7.00% Senior Notes 5.2 ––

6.85% Senior Notes 4.1 ––

Vons Debentures 10.2 ––

10% Senior Notes 4.3 5.9 5.9

Mortgage notes payable 22.0 33.0 43.3

Other notes payable 9.9 11.9 11.3

Medium-term notes 4.4 6.0 7.1

Short-term bank borrowings 8.8 5.1 6.6

Obligations under capital leases 26.0 20.8 21.0

Amortization of deferred

finance costs 1.7 1.8 4.0

Interest rate swap and

cap agreements 3.3 3.0 0.3

Capitalized interest (5.7) (4.3) (4.6)

■■■■■■■■

$241.2 $178.5 $199.8

■■■■■■■■

In May 1997, Safeway entered into interest rate cap agree-

ments which expire in 1999 and entitle the Company to

receive from counterparties the amounts, if any, by which

interest at LIBOR on an $850 million notional amount exceeds

7%. The unamortized cost to purchase the cap agreements

was $2.5 million at year-end 1997.

Additionally, as of year-end 1997, the Company had effec-

tively converted $135.1 million of its floating rate debt to

fixed interest rate debt through the use of interest rate swap

agreements. The significant terms of the swap agreements

outstanding at year-end 1997 were as follows (dollars in

millions):

Variable

Canada Interest

U.S. Fixed Fixed Rates

Notional Interest Interest to be Origination Expiration

Principal Rates Paid Rates Paid Received Date Date

$100.0 6.2% 5.8% 1997 2007

35.1 6.0% 4.9 1993 1998

$135.1

The variable interest rate received on the U.S. swap is based

on federal reserve rates quoted for commercial paper. The vari-

able interest rate received on the Canadian swap is based on the

average of bankers’ acceptance rates quoted by Canadian banks.

At year-end 1997 and 1996, net unrealized losses on the interest

rate swap agreements totaled $0.4 million and $2.0 million.

The notional principal amounts do not represent cash flows

and therefore are not subject to credit risk. The Company is

subject to risk from nonperformance of the counterparties to

the swap and cap agreements in the amount of any interest

differential to be received. Because the Company monitors the

29