Safeway 1997 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 1997 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44

|

|

33

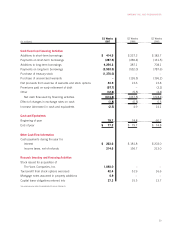

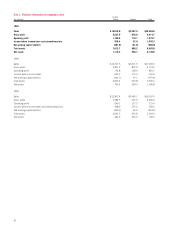

The funded status of the Plans at year-end was as follows

(in millions):

1997 1996

Fair value of assets at year-end $1,662.6 $1,392.0

■■

Actuarially determined present value of:

Vested benefit obligations 916.7 758.9

Non-vested benefit obligations 15.8 9.3

■■

Accumulated benefit obligations 932.5 768.2

Additional amounts related to

projected compensation

increases 124.3 98.9

■■

Projected benefit obligations 1,056.8 867.1

■■

Fair value of assets in excess of

projected benefit obligations 605.8 524.9

Adjustment for difference in book

and tax basis of assets (165.1) (165.1)

Unamortized prior service costs

resulting from improved Plan

benefits 93.7 83.3

Net gain from actuarial experience

which has not been recognized in

the consolidated financial

statements (193.0) (114.4)

■■

Prepaid pension costs $ 341.4 $ 328.7

■■

Retirement Restoration Plan The Retirement Restoration Plan

provides death benefits and supplemental income payments for

senior executives after retirement. The Company recognized

expense of $4.3 million in 1997, $4.4 million in 1996 and $3.4

million in 1995. The aggregate projected benefit obligation of the

Retirement Restoration Plan was approximately $48.4 million at

year-end 1997 and $44.9 million at year-end 1996.

Postretirement Benefits Other Than Pensions In addition to pen-

sion and the Retirement Restoration Plan benefits, the Company

sponsors plans that provide postretirement medical and life

insurance benefits to certain salaried employees. Retirees share

a portion of the cost of the postretirement medical plans.

Safeway pays all of the cost of the life insurance plans. The

plans are not funded.

In 1996, the Safeway postretirement medical plan was

amended to restrict the types of coverage available, to change

the participant contributions, and to exclude future retirees from

participating in the plan. The exclusion of future retirees in the

plan was considered a curtailment under the provisions of SFAS

No. 88 which resulted in recognition of a curtailment gain of

$14.5 million in 1996. In 1997, similar amendments were made

to the Vons postretirement medical plan, resulting in a $14.0

million adjustment to the accumulated postretirement benefit

obligation (“APBO”) at the date of the Merger.

The Company’s APBO was $28.4 million at year-end 1997

and $15.9 million at year-end 1996. The APBO represents the

actuarial present value of benefits expected to be paid after

retirement. Postretirement benefit expense was $2.2 million in

1997, $1.7 million in 1996 and $2.5 million in 1995.

The significant assumptions used to determine the periodic

postretirement benefit expense and the APBO were as follows:

1997 1996 1995

Discount rate 7.0% 7.0% 7.0%

Rate of compensation increase 5.5 5.5 5.5

For 1998, a 7.5% annual rate of increase in the per capita

cost of postretirement medical benefits provided under the

Company’s group health plan was assumed. The rate was

assumed to decrease gradually to 5.5% for 2002 and remain at

that level thereafter. A 5.5% annual rate of increase was

assumed for 1998 and thereafter in the per capita cost of postre-

tirement benefits provided under HMO plans. If the health care

cost trend rate assumptions were increased by 1% in each year,

the APBO as of year-end 1997 would increase $0.8 million, and

the net periodic postretirement benefit expense for 1997 would

remain unchanged. Retiree contributions have historically been

adjusted when plan costs increase. The APBO for the medical

plans anticipates future cost-sharing changes to the written plan

that are consistent with the Company’s past practice.

Multi-Employer Pension Plans Safeway participates in various

multi-employer pension plans, covering virtually all Company

employees not covered under the Company’s non-contributory

pension plans, pursuant to agreements between the Company

and employee bargaining units which are members of such plans.

These plans are generally defined benefit plans; however, in many

cases, specific benefit levels are not negotiated with or known by

the employer-contributors. Contributions of $130 million in 1997,

$112 million in 1996 and $105 million in 1995 were made and

charged to income.

Under U.S. legislation regarding such pension plans, a

company is required to continue funding its proportionate

share of a plan’s unfunded vested benefits in the event of

withdrawal (as defined by the legislation) from a plan or plan

termination. Safeway participates in a number of these pen-

sion plans, and the potential obligation as a participant in

these plans may be significant. The information required to

determine the total amount of this contingent obligation, as

well as the total amount of accumulated benefits and net

assets of such plans, is not readily available. During 1988 and

1987, the Company sold certain operations. In most cases the

party acquiring the operation agreed to continue making con-

tributions to the plans. Safeway is relieved of the obligations

related to these sold operations to the extent the acquiring

parties continue to make contributions. Whether such sales

could result in withdrawal under ERISA and, if so, whether

such withdrawals could result in liability to the Company, is

not determinable at this time.