Starbucks 2005 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2005 Starbucks annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

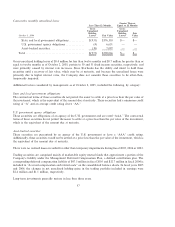

Recent Accounting Pronouncements

In November 2005, the FASB issued Staff Position No. FAS 115-1, ""The Meaning of Other-Than-

Temporary Impairment and Its Application to Certain Investments'' (""FSP 115-1''). FSP 115-1 provides

accounting guidance for identifying and recognizing other-than-temporary impairments of debt and equity

securities, as well as cost method investments in addition to disclosure requirements. FSP 115-1 is effective for

reporting periods beginning after December 15, 2005, and earlier application is permitted. The Company has

adopted this new pronouncement in its fourth quarter of fiscal 2005. The adoption of FSP 115-1 did not have

an impact on the Company's consolidated financial statements. The required disclosures are presented in

Notes 4 and 7 of this Report.

In March 2005, the FASB issued Interpretation No. 47, ""Accounting for Conditional Asset Retirement

Obligations, an interpretation of FASB Statement No. 143'' (""FIN 47''). FIN 47 requires the recognition of a

liability for the fair value of a legally-required conditional asset retirement obligation when incurred, if the

liability's fair value can be reasonably estimated. FIN 47 also clarifies when an entity would have sufficient

information to reasonably estimate the fair value of an asset retirement obligation. FIN 47 is effective for

fiscal years ending after December 15, 2005, or no later than Starbucks fiscal fourth quarter of 2006. The

Company has not yet determined the impact of adoption on its consolidated statement of earnings and balance

sheet.

In December 2004, the FASB issued SFAS 123R, a revision of SFAS 123. SFAS 123R will require Starbucks

to, among other things, measure all employee stock-based compensation awards using a fair value method and

record the expense in the Company's consolidated financial statements. The provisions of SFAS 123R, as

amended by SEC Staff Accounting Bulletin No. 107, ""Share-Based Payment,'' are effective no later than the

beginning of the next fiscal year that begins after June 15, 2005. Starbucks will adopt the new requirements

using the modified prospective transition method in its first fiscal quarter of 2006, which ends January 1, 2006.

In addition to the recognition of expense in the financial statements, under SFAS 123R, any excess tax

benefits received upon exercise of options will be presented as a financing activity inflow rather than as an

adjustment of operating activity as currently presented. Based on its current analysis and information,

management has determined that the impact of adopting SFAS 123R will result in a material reduction of net

earnings and diluted earnings per share.

In December 2004, the FASB issued Staff Position No. FAS 109-1, ""Application of SFAS No. 109,

Accounting for Income Taxes, to the Tax Deduction on Qualified Production Activities provided by the

American Jobs Creation Act of 2004'' (""FSP 109-1''). FSP 109-1 states that qualified domestic production

activities should be accounted for as a special deduction under SFAS No. 109, ""Accounting for Income

Taxes,'' and not be treated as a rate reduction. The provisions of FSP 109-1 are effective immediately. The

Company will qualify for a benefit beginning in fiscal 2006, which is not expected to be material to the

Company's consolidated financial statements.

In December 2004, the FASB issued Staff Position No. FAS 109-2, ""Accounting and Disclosure Guidance

for the Foreign Earnings Repatriation Provision within the American Jobs Creation Act of 2004''

(""FSP 109-2''). The American Jobs Creation Act allows a special one-time dividends received deduction on

the repatriation of certain foreign earnings to a U.S. taxpayer (repatriation provision), provided certain criteria

are met. The law allows the Company to make an election to repatriate earnings through fiscal 2006.

FSP 109-2 provides accounting and disclosure guidance for the repatriation provision. Although FSP 109-2

was effective upon its issuance, it allows companies additional time beyond the enactment date to evaluate the

effects of the provision on its plan for investment or repatriation of unremitted foreign earnings. The Company

continues to evaluate the impact of the new Act to determine whether it will repatriate foreign earnings and

the impact, if any, this pronouncement will have on its consolidated financial statements. As of October 2,

52