Starbucks 2005 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2005 Starbucks annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

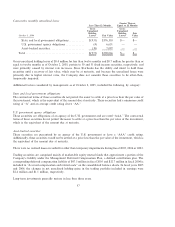

2005, the Company has not made an election to repatriate earnings under this provision. The Company may or

may not elect to repatriate earnings in fiscal 2006. Earnings under consideration for repatriation range from $0

to $75 million and the related income tax effects range from $0 to $5 million. As provided in FSP 109-2,

Starbucks has not adjusted its tax expense or deferred tax liability to reflect the repatriation provision.

In November 2004, the FASB issued Statement No. 151, ""Inventory Costs, an amendment of ARB No. 43,

Chapter 4'' (""SFAS 151''). SFAS 151 clarifies that abnormal inventory costs such as costs of idle facilities,

excess freight and handling costs, and wasted materials (spoilage) are required to be recognized as current

period charges. The provisions of SFAS 151 are effective for fiscal years beginning after June 15, 2005. The

adoption of SFAS 151 in fiscal 2006 is not expected to have a significant impact on the Company's

consolidated balance sheet or statement of earnings.

Note 2: Business Acquisitions

In November 2004, Starbucks increased its equity ownership from 18% to 100% for its licensed operations in

Germany. As a result, management determined that a change in accounting method, from the cost method to

the consolidation method, was necessary and included adjusting previously reported information for the

Company's proportionate share of net losses of 18% as required by APB No. 18, ""The Equity Method of

Accounting for Investments in Common Stock.'' The cumulative effect of the accounting change for prior

periods resulted in a reduction of retained earnings of $3.6 million as of October 3, 2004. See Note 19 in the

Company's 2004 10-K/A for additional information.

In April 2005, Starbucks acquired substantially all of the assets of Ethos Brands, LLC, (such assets,

""Ethos''), a privately held bottled water company based in Santa Monica, California, for $8 million. The

earnings of Ethos are included in the accompanying consolidated financial statements from the date of

acquisition.

In July 2005, Starbucks increased its equity ownership in its licensed operations in Southern China and Chile,

to 51% and 100%, respectively, for purchase prices totaling $15 million, of which $10 million was payable as of

October 2, 2005. Previously, Starbucks owned less than 20% in each of these operations, which were

accounted for under the cost method. These increases in equity ownership resulted in a change of accounting

method, from the cost method to the consolidation method, on the respective dates of acquisition. This

accounting change also included adjusting previously reported information for the Company's proportionate

share of net losses in Southern China and Chile.

53