Walgreens 2014 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2014 Walgreens annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

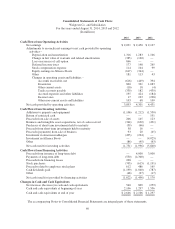

Letters of credit are issued to support purchase obligations and commitments (as reflected on the Contractual

Obligations and Commitments table) as follows (in millions):

August 31,

2014

Inventory purchase commitments $151

Insurance 259

Real estate development 9

Total $419

We have no off-balance sheet arrangements other than those disclosed on the Contractual Obligations and

Commitments table. Both on-balance sheet and off-balance sheet financing alternatives are considered when

pursuing our capital structure and capital allocation objectives.

RECENT ACCOUNTING PRONOUNCEMENTS

In May 2014, the Financial Accounting Standards Board (FASB) issued ASU 2014-09, Revenue from Contracts

with Customers, as a new Topic, ASC Topic 606. The new revenue recognition standard provides a five-step

analysis of transactions to determine when and how revenue is recognized. The core principle is that a company

should recognize revenue to depict the transfer of promised goods or services to customers in an amount that

reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. This

ASU is effective for annual periods beginning after December 15, 2016 (fiscal 2018) and shall be applied

retrospectively to each period presented or as a cumulative-effect adjustment as of the date of adoption. The

Company is evaluating the effect of adopting this new accounting guidance, but does not expect adoption will

have a material impact on the Company’s results of operations, cash flows or financial position.

In April 2014, the FASB issued ASU 2014-08, Reporting Discontinued Operations and Disclosures of Disposals

of Components of an Entity. This ASU raises the threshold for a disposal to qualify as discontinued operations

and requires new disclosures for individually material disposal transactions that do not meet the definition of a

discontinued operation. Under the new standard, companies report discontinued operations when they have a

disposal that represents a strategic shift that has or will have a major impact on operations or financial

results. This update will be applied prospectively and is effective for annual periods, and interim periods within

those years, beginning after December 15, 2014 (fiscal 2016). Early adoption is permitted provided the disposal

was not previously disclosed. This update will not have a material impact on the Company’s reported results of

operations and financial position. This ASU is non-cash in nature and will not affect the Company’s cash

position.

In May 2013, the FASB reissued an exposure draft on lease accounting that would require entities to recognize

assets and liabilities arising from lease contracts on the balance sheet. The proposed exposure draft states that

lessees and lessors should apply a “right-of-use model” in accounting for all leases. Under the proposed model,

lessees would recognize an asset for the right to use the leased asset, and a liability for the obligation to make

rental payments over the lease term. When measuring the asset and liability, variable lease payments are

excluded, whereas renewal options that provide a significant economic incentive upon renewal would be

included. The accounting by a lessor would reflect its retained exposure to the risks or benefits of the underlying

leased asset. A lessor would recognize an asset representing its right to receive lease payments based on the

expected term of the lease. The lease expense from real estate based leases would continue to be recorded under a

straight-line approach, but other leases not related to real estate would be expensed using an effective interest

method that would accelerate lease expense. A final standard is currently expected to be issued in calendar 2014

and would be effective no earlier than annual reporting periods beginning on January 1, 2017 (fiscal 2018 for the

Company). The proposed standard, as currently drafted, would have a material impact on the Company’s

financial position and the impact on the Company’s reported results of operations is being evaluated. The impact

of this exposure draft is non-cash in nature and would not affect the Company’s cash position.

53