Walmart 2014 Annual Report Download - page 26

Download and view the complete annual report

Please find page 26 of the 2014 Walmart annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

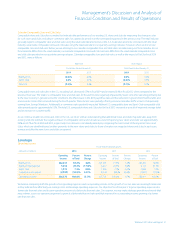

Management’s Discussion and Analysis of

Financial Condition and Results of Operations

Results of Operations

Consolidated Results of Operations

(Amounts in millions, Fiscal Years Ended January 31,

except unit counts) 2014 2013 2012

Total revenues $476,294 $468,651 $446,509

Percentage change in

total revenues from

previous scal year 1.6% 5.0% 6.0%

Net sales $473,076 $465,604 $443,416

Percentage change in

net sales from

previous scal year 1.6% 5.0% 5.9%

Total U.S. calendar comparable

store and club sales (0.5)% 2.4% 1.6%

Gross prot margin as a

percentage of net sales 24.3% 24.3% 24.5%

Operating income $ 26,872 $ 27,725 $ 26,491

Operating income as a

percentage of net sales 5.7% 6.0% 6.0%

Income from continuing

operations $ 16,551 $ 17,704 $ 16,408

Unit counts at period end 10,942 10,408 9,766

Retail square feet at period end 1,101 1,070 1,035

Our total revenues, which are mostly comprised of net sales, but also

include membership and other income, increased 1.6% and 5.0% for scal

2014 and 2013, respectively, when compared to the previous scal year.

The increase in total revenues was primarily a result of increases in our

net sales, which also increased 1.6% and 5.0% for scal 2014 and 2013,

respectively. The increase in net sales for scal 2014 was primarily due to

3.1% year-over-year growth in retail square feet, higher e-commerce sales,

the impact of scal 2013 acquisitions, which accounted for $730 million

of the net sales increase, and positive comparable club sales at Sam’s Club.

The positive eect of these items was partially oset by $5.1 billion of

negative impact from uctuations in currency exchange rates and

decreases in comparable store sales at Walmart U.S. and in a number of

our international operations. The increase in net sales for scal 2013 was

due to 3.3% growth in retail square feet and positive comparable store

and club sales. Additionally, net sales from acquisitions, through their

respective anniversary dates, accounted for $4.0 billion of the increase in

net sales. The increase in net sales for scal 2013 was partially oset by

$4.5 billion of negative impact from uctuations in currency exchange

rates. Increases in membership and other income of 5.6%, primarily due

to higher membership and other income at Sam’s Club, also contributed

to the increase in total revenues for scal 2014 and 2013.

Our gross prot rate decreased 3 basis points for scal 2014, when

compared to the previous scal year, primarily due to our ongoing

investment in price, as well as merchandise mix. For scal 2013, gross

prot rate decreased 12 basis points, when compared to the previous

scal year, primarily due to the Walmart U.S. segment’s strategic focus

on price investment and low price leadership.

For scal 2014, we did not meet our objective of growing operating

expenses at a slower rate than net sales as operating expenses as a

percentage of net sales increased 27 basis points. Overall, lower than

anticipated net sales, higher investment in key areas, such as global

leverage and e-commerce initiatives, and nearly $1.0 billion of increased

expenses for various matters described in the Walmart International

segment discussion, were the primary cause for the increase in operating

expenses as a percentage of net sales. Additional expenses related to the

FCPA inquiries and investigations, as well as our global compliance pro-

gram and related organizational enhancements also contributed to the

increase in operating expenses as a percentage of net sales. The negative

leverage impact of these items was partially oset by lower incentive

expenses for scal 2014. For scal 2013, we met our objective of growing

operating expenses at a slower rate than net sales as operating expenses

as a percentage of net sales decreased 14 basis points. The scal 2013

decrease in operating expenses as a percentage of net sales was primarily

due to productivity improvements and expense management.

For scal 2014, we did not meet our objective of growing operating

income at a faster rate than net sales as operating income decreased

3.1% while net sales increased 1.6%, when compared to the previous

scal year. This was primarily due to the factors we discussed for not

leveraging operating expenses, partially oset by increases in member-

ship and other income. For scal 2013, we also did not meet our

objective of growing operating income at a faster rate than net sales as

operating income increased 4.7% while net sales increased 5.0%, when

compared to the previous scal year. The primary causes for operating

income growing slower than net sales in scal 2013 were investments in

e-commerce initiatives, increased expenses related to the FCPA inquiries

and investigations, as well as our global compliance program and related

organizational enhancements, and investments in price, which reduced

gross margin.

Our eective income tax rates were 32.9%, 31.0% and 32.6% for scal 2014,

2013 and 2012, respectively. The reconciliation from the U.S. statutory

rate to the eective income tax rates for scal 2014, 2013 and 2012 is

presented in Note 9 in the “Notes to Consolidated Financial Statements.”

Our eective income tax rate for scal 2014 was higher than in scal 2013

primarily due to the tax impacts attributable to repatriated international

earnings during scal 2014. Our scal 2013 eective income tax rate was

lower than in scal 2012 primarily because the scal 2013 rate beneted

from a number of discrete tax items, including the positive impact from

scal 2013 legislative changes arising at the end of the scal 2012 year,

most notably the American Taxpayer Relief Act of 2012. Our eective

income tax rate may uctuate from period to period as a result of factors

including changes in our assessment of certain tax contingencies,

increases or decreases in valuation allowances, changes in tax law,

outcomes of administrative audits, the impact of discrete items and the

mix of earnings among our U.S. and international operations where

the statutory rates are generally lower than the U.S. statutory rate.

As a result of the factors discussed above, we reported $16.6 billion,

$17.7 billion and $16.4 billion of consolidated income from continuing

operations for scal 2014, 2013 and 2012, respectively, a decrease of

$1.1 billion for scal 2014 and an increase of $1.3 billion for scal 2013,

when compared to the previous scal year. Diluted income per common

share from continuing operations attributable to Walmart (“EPS”) was

$4.85, $5.01 and $4.53 for scal 2014, 2013 and 2012, respectively.

24 Walmart 2014 Annual Report