Walmart 2014 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2014 Walmart annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

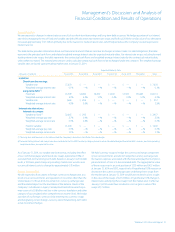

Management’s Discussion and Analysis of

Financial Condition and Results of Operations

Interest Rate Risk

We are exposed to changes in interest rates as a result of our short-term borrowings and long-term debt issuances. We hedge a portion of our interest

rate risk by managing the mix of xed and variable rate debt. We also enter into interest rate swaps and for scal 2014, the net fair value of our derivatives

increased approximately $107 million primarily due to uctuations in market interest rates, which helped reduce the Company’s overall exposure to

interest rate risk.

The table below provides information about our nancial instruments that are sensitive to changes in interest rates. For debt obligations, the table

represents the principal cash ows and related weighted-average interest rates by expected maturity dates. For interest rate swaps, including forward

starting interest rate swaps, the table represents the contractual cash ows and weighted-average interest rates by the contractual maturity date,

unless otherwise noted. The notional amounts are used to calculate contractual cash ows to be exchanged under the contracts. The weighted-average

variable rates are based upon prevailing market rates at January 31, 2014.

Expected Maturity Date

(Amounts in millions) Fiscal 2015 Fiscal 2016 Fiscal 2017 Fiscal 2018 Fiscal 2019 Thereafter Total

Liabilities

Short-term borrowings:

Variable rate $7,670 $ — $ — $ — $ — $ — $ 7,670

Weighted-average interest rate 0.1% —% —% —% —% —% 0.1%

Long-term debt

(1)

:

Fixed rate $3,309 $4,084 $2,000 $1,000 $3,500 $30,223 $44,116

Weighted-average interest rate 2.3% 2.4% 1.7% 5.4% 3.0% 5.1% 4.3%

Variable rate $665 $ 292 $ — $ — $ — $ — $ 957

Weighted-average interest rate 4.3% 0.6% —% —% —% —% 3.2%

Interest rate derivatives

Interest rate swaps:

Variable to xed

(2)

$2,665 $ 292 $ — $ — $ — $ — $ 2,957

Weighted-average pay rate 2.7% 0.9% —% —% —% —% 2.5%

Weighted-average receive rate 0.3% 0.6% —% —% —% —% 0.3%

Fixed to variable $1,000 $ — $ — $ — $ — $ — $ 1,000

Weighted-average pay rate 0.3% —% —% —% —% —% 0.3%

Weighted-average receive rate 3.1% —% —% —% —% —% 3.1%

(1) The long-term debt amounts in the table exclude the Company’s derivatives classified as fair value hedges.

(2) Forward starting interest rate swaps have been included in the fiscal 2015 maturity category based on when the related hedged forecasted debt issuances, and corresponding

swap terminations, are expected to occur.

As of January 31, 2014, our variable rate borrowings, including the eect

of our commercial paper and interest rate swaps, represented 18% of

our total short-term and long-term debt. Based on January 31, 2014 debt

levels, a 100 basis point change in prevailing market rates would cause

our annual interest costs to change by approximately $78 million.

Foreign Currency Risk

We are exposed to uctuations in foreign currency exchange rates as a

result of our net investments and operations in countries other than the

United States. For scal 2014, movements in currency exchange rates

and the related impact on the translation of the balance sheets of the

Company’s subsidiaries in Japan, Canada, Brazil and Africa were the pri-

mary cause of a $2.8 billion net loss in the currency translation and other

category of accumulated other comprehensive income (loss). We hedge

a portion of our foreign currency risk by entering into currency swaps

and designating certain foreign-currency-denominated long-term debt

as net investment hedges.

We hold currency swaps to hedge the currency exchange component

of our net investments and also to hedge the currency exchange rate

uctuation exposure associated with the forecasted payments of princi-

pal and interest of non-U.S. denominated debt. The aggregate fair value

of these swaps was in an asset position of $550 million and $453 million

at January 31, 2014 and 2013, respectively. A hypothetical 10% increase or

decrease in the currency exchange rates underlying these swaps from

the market rate at January 31, 2014 would have resulted in a loss or gain

in the value of the swaps of $274 million. A hypothetical 10% change in

interest rates underlying these swaps from the market rates in eect at

January 31, 2014 would have resulted in a loss or gain in value of the

swaps of $7 million.

Walmart 2014 Annual Report 31