Walmart 2014 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 2014 Walmart annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

Management’s Discussion and Analysis of

Financial Condition and Results of Operations

Transactions with Noncontrolling Interest Holders

As discussed in Note 13 to our Consolidated Financial Statements, we

have completed or anticipate completing the following transactions

with noncontrolling interest shareholders that have impacted our cash

ows from nancing activities or that will impact our cash ows from

nancing activities in the future:

India Operations

During scal 2014, the Company acquired, for $100 million, the

remaining ownership interest in Bharti Walmart Private Limited,

previously a joint venture between Bharti Ventures Limited (“Bharti”)

and the Company established in 2007, which operated the Company’s

wholesale cash & carry business in India. Upon completion of the

transaction, the Company became the sole owner of the cash &

carry business in India. In addition, the Company also terminated

its joint venture, franchise and supply agreements with Bharti Retail

Limited (“Bharti Retail”), which operates Bharti’s retail business in

India, and transferred its investment in that business to Bharti. In

connection with the agreements related to the Bharti retail business,

the Company paid and forgave indebtedness of approximately

$234 million. The amounts paid to complete these transactions are

included in the other investing and other nancing categories in the

Company’s Consolidated Statements of Cash Flows for scal 2014.

Walmart Chile

In September 2013, certain redeemable noncontrolling interest

shareholders exercised put options that required the Company to

purchase a portion of their shares in Walmart Chile at the mutually

agreed upon redemption value to be determined after exercise of

the put options. In scal 2014, the Company recorded an increase to

redeemable noncontrolling interest of $1.0 billion, with a correspond-

ing decrease to capital in excess of par value, to reect the estimated

redemption value of the redeemable noncontrolling interest at

$1.5 billion. Subsequent to the initial exercise, the Company negotiated

with the redeemable noncontrolling interest shareholders to acquire

all of their redeemable noncontrolling interest shares. The Company

completed this transaction in February 2014, after period end, using

its existing cash and bringing its ownership interest in Walmart Chile

to approximately 99.7 percent. The Company has since initiated a

tender oer for the remaining 0.3 percent noncontrolling interest

held by the public in Chile at the same value per share as was paid

to the redeemable noncontrolling interest shareholders. The tender

oer will expire in the rst quarter of scal 2015.

Capital Resources

We believe cash ows from continuing operations, our current cash

position and access to debt and capital markets will continue to be

sucient to meet our anticipated operating cash needs, including

seasonal buildups in merchandise inventories, and complete our capital

expenditures, dividend payments and share repurchases.

We have strong commercial and long-term debt ratings that have

enabled and should continue to enable us to renance our debt as it

becomes due at favorable rates in debt capital markets. At January 31,

2014, the ratings assigned to our commercial paper and rated series

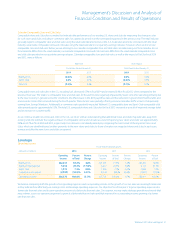

of our outstanding long-term debt were as follows:

Rating agency Commercial paper Long-term debt

Standard & Poor’s A-1+ AA

Moody’s Investors Service P-1 Aa2

Fitch Ratings F1+ AA

Credit rating agencies review their ratings periodically and, therefore, the

credit ratings assigned to us by each agency may be subject to revision

at any time. Accordingly, we are not able to predict whether our current

credit ratings will remain consistent over time. Factors that could aect

our credit ratings include changes in our operating performance, the

general economic environment, conditions in the retail industry, our

nancial position, including our total debt and capitalization, and

changes in our business strategy. Any downgrade of our credit ratings

by a credit rating agency could increase our future borrowing costs or

impair our ability to access capital and credit markets on terms com-

mercially acceptable to us. In addition, any downgrade of our current

short-term credit ratings could impair our ability to access the commercial

paper markets with the same exibility that we have experienced

historically, potentially requiring us to rely more heavily on more expensive

types of debt nancing. The credit rating agency ratings are not

recommendations to buy, sell or hold our commercial paper or debt

securities. Each rating may be subject to revision or withdrawal at any

time by the assigning rating organization and should be evaluated

independently of any other rating. Moreover, each credit rating is specic

to the security to which it applies.

To monitor our credit rating and our capacity for long-term nancing,

we consider various qualitative and quantitative factors. We monitor the

ratio of our debt-to-total capitalization as support for our long-term

nancing decisions. At January 31, 2014 and 2013, the ratio of our debt-

to-total capitalization was 42.6% and 41.5%, respectively. For the purpose

of this calculation, debt is dened as the sum of short-term borrowings,

long-term debt due within one year, obligations under capital leases

due within one year, long-term debt and long-term obligations under

capital leases. Total capitalization is dened as debt plus total Walmart

shareholders’ equity. The increase in our debt-to-total capitalization

ratio was primarily driven by changes in working capital and higher

long-term debt balances.

Walmart 2014 Annual Report 29