Walmart 2014 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2014 Walmart annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

Management’s Discussion and Analysis of

Financial Condition and Results of Operations

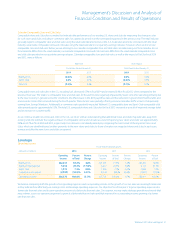

Cash Flows Provided by Operating Activities

Cash ows provided by operating activities were $23.3 billion, $25.6 billion

and $24.3 billion for scal 2014, 2013 and 2012, respectively. The decrease

in cash ows provided by operating activities for scal 2014, when

compared to the previous scal year, was primarily due to the timing of

income tax payments, as well as lower income from continuing operations.

The increase in cash ows provided by operating activities in scal 2013,

when compared to the previous scal year, was primarily due to higher

income for continuing operations.

Cash Equivalents and Working Capital

Cash and cash equivalents were $7.3 billion and $7.8 billion at January 31,

2014 and 2013, respectively. Our working capital decits were $8.2 billion

and $11.9 billion at January 31, 2014 and 2013, respectively. The decrease

in our working capital decit was primarily attributable to a decrease in

long-term debt due within one year and an increase in our inventory

levels due to lower than anticipated sales across the Company. Timing

dierences also contributed to the decrease in our working capital

decit. We generally operate with a working capital decit due to our

ecient use of cash in funding operations and in providing returns to

our shareholders in the form of share repurchases and payments of

cash dividends.

We employ nancing strategies (e.g., global funding structures) in an

eort to ensure cash can be made available in the country in which it is

needed with the minimum cost possible. We do not believe it will be

necessary to repatriate cash and cash equivalents held outside of the U.S.

and anticipate our domestic liquidity needs will be met through other

funding sources (ongoing cash ows generated from operations, external

borrowings or both). Accordingly, we intend, with only certain exceptions,

to continue to indenitely reinvest our cash and cash equivalents held

outside of the U.S. in our foreign operations. When the income earned

(either from operations or through global funding structures) and inde-

nitely reinvested outside of the U.S. is taxed at local country tax rates, which

are generally lower than the U.S. statutory rate, we realize an eective tax

rate benet. If our intentions with respect to reinvestment were to change,

most of the amounts held within our foreign operations could be repatri-

ated to the U.S., although any repatriation under current U.S. tax laws

would be subject to U.S. federal income taxes, less applicable foreign tax

credits. As of January 31, 2014 and 2013, cash and cash equivalents of

approximately $1.9 billion may not be freely transferable to the U.S. due

to local laws or other restrictions. We do not expect local laws, other

limitations or potential taxes on anticipated future repatriations of cash

amounts held outside of the U.S. to have a material eect on our overall

liquidity, nancial condition or results of operations.

Cash Flows Used in Investing Activities

Cash ows used in investing activities generally consist of payments

for property and equipment and investments and business acquisitions.

Payments for property and equipment were $13.1 billion, $12.9 billion

and $13.5 billion for scal 2014, 2013 and 2012, respectively. The scal

2014 increase was primarily for additional Neighborhood Markets and

other small formats in the Walmart U.S. segment. The scal 2013 decrease

was primarily the result of lowering the average cost for remodels.

Payments for investments and business acquisitions, net of cash

acquired, were $15 million, $316 million and $3.5 billion for scal 2014,

2013 and 2012, respectively.

Pending Transaction

As discussed in Note 13 to our Consolidated Financial Statements,

we currently anticipate completing the following transaction that will

impact our future cash ows from investing activities:

Vips Restaurant Business in Mexico

In September 2013, Wal-Mart de México, S.A.B. de C.V. (“Walmex”),

a majority-owned subsidiary of the Company, entered into a

denitive agreement with Alsea S.A.B. de C.V. to dispose of Walmex’s

Vips restaurant business (“Vips”) in Mexico for approximately

$625 million. Accordingly, the Vips operating results are presented

as discontinued operations in the Company’s Consolidated

Statements of Income for scal 2014, 2013 and 2012. Additionally,

the Vips assets and liabilities to be disposed of are reported

separately in the Company’s Consolidated Balance Sheets as of

January 31, 2014. The Vips sale is subject to approval by Mexican

regulatory authorities and is currently expected to close during

the rst half of scal 2015. Upon completion of this transaction,

the Company expects to record a net gain, which will be recorded

in discontinued operations in the Company’s Consolidated

Statements of Income.

Global Expansion Activities

In addition to our growth in retail square feet discussed throughout the

“Results of Operations” discussion, we expanded in e-commerce in each of

our segments during scal 2014, with Walmart U.S. and Sam’s Club focused

on the e-commerce market in the U.S. and Walmart International focused

on the e-commerce markets in countries outside of the U.S., primarily the

United Kingdom, China and Brazil. Some of our scal 2014 e-commerce

accomplishments included developing a new recommendation engine

to further personalize search, improving the mobile shopping experience,

accelerating the deployment of our global technology platform and

increasing assortment oered on our websites. Each of these accom-

plishments further supports the operations of our segments.

Our scal 2015 global expansion plans include continuing to grow our

retail square feet, which will include a signicant increase in the number

of Neighborhood Markets and other small stores. In addition, we plan to

continue to expand our e-commerce capabilities. We anticipate nancing

our global expansion activities through cash ows provided by operating

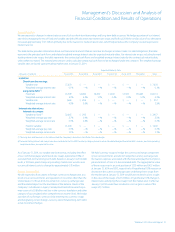

activities and future debt nancings. The following table provides our

estimated range for scal 2015 capital expenditures, as well as our

estimated range for growth in retail square feet. Our anticipated

e-commerce capital expenditures are included in our estimated range

for scal 2015 capital expenditures. The amounts in the table do not

include capital expenditures or growth in retail square feet from any

pending or future acquisitions.

Fiscal 2015 Fiscal 2015

Projected Capital Projected Growth in

Expenditures Retail Square Feet

(in billions) (in thousands)

Walmart U.S. $ 6.4 to $ 6.9 21,000 to 23,000

Walmart International 4.0 to 4.5 12,000 to 14,000

Sam’s Club 1.0 to 1.0 2,000 to 2,000

Corporate and support 1.0 to 1.0 — to —

Total $12.4 to $13.4 35,000 to 39,000

Walmart 2014 Annual Report 27