American Airlines 2008 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2008 American Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

|

|

62

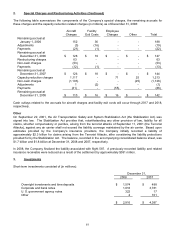

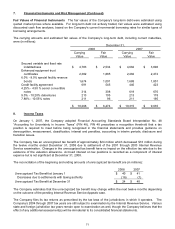

3. Investments (Continued)

Short-term investments at December 31, 2008, by contractual maturity included (in millions):

Due in one year or less

$ 2,916

Due between one year and three years

-

Due after three years

-

$ 2,916

All short-term investments are classified as available-for-sale and stated at fair value. Unrealized gains and losses

are reflected as a component of Accumulated other comprehensive income (loss).

The Company has adopted Statement of Financial Accounting Standards No. 157 “Fair Value Measurements”

(SFAS 157) as it applies to financial assets and liabilities effective January 1, 2008. SFAS 157 defines fair value,

establishes a framework for measuring fair value under generally accepted accounting principles (GAAP) and

enhances disclosures about fair value measurements.

SFAS 157 defines fair value as the exchange price that would be received for an asset or paid to transfer a liability

(an exit price) in the principal or most advantageous market for the asset or liability in an orderly transaction

between market participants on the measurement date. Under SFAS 157, AMR utilizes several valuation

techniques in order to assess the fair value of the Company’s financial assets and liabilities. The Company’s fuel

derivative contracts, which primarily consist of commodity options and collars, are valued using energy and

commodity market data which is derived by combining raw inputs with quantitative models and processes to

generate forward curves and volatilities. The Company’s short-term investments primarily utilize broker quotes in

a non-active market for valuation of these securities.

SFAS 157 also establishes a fair value hierarchy which requires an entity to maximize the use of observable inputs

and minimize the use of unobservable inputs when measuring fair value. The standard describes three levels of

inputs that may be used to measure fair value:

Level 1 - Quoted prices in active markets for identical assets or liabilities.

Level 2 - Observable inputs other than Level 1 prices such as quoted prices for similar assets or liabilities;

quoted prices in markets that are not active; or other inputs that are observable or can be corroborated by

observable market data for substantially the full term of the assets or liabilities. The Company’s short-term

investments primarily utilize broker quotes in a non-active market for valuation of these securities. The

Company’s fuel derivative contracts, which primarily consist of commodity options and collars, are valued

using energy and commodity market data which is derived by combining raw inputs with quantitative models

and processes to generate forward curves and volatilities.

Level 3 - Unobservable inputs that are supported by little or no market activity and that are significant to the

fair value of the assets or liabilities.

The Company utilizes the market approach to measure fair value for its financial assets and liabilities. The

market approach uses prices and other relevant information generated by market transactions involving

identical or comparable assets or liabilities.