American Airlines 2008 Annual Report Download - page 73

Download and view the complete annual report

Please find page 73 of the 2008 American Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

|

|

70

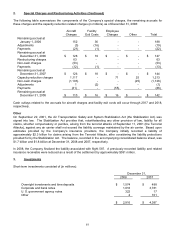

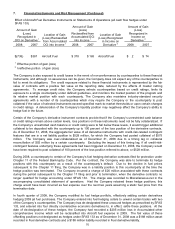

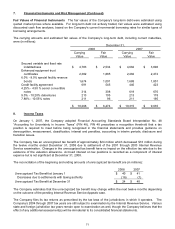

7. Financial Instruments and Risk Management (Continued)

Effect of Aircraft Fuel Derivative Instruments on Statements of Operations (all cash flow hedges under

SFAS 133)

Amount of Gain

(Loss)

Recognized in

OCI on Derivative1

Location of Gain

(Loss) Reclassified

from Accumulated

OCI into Income 1

Amount of Gain

(Loss)

Reclassified from

Accumulated OCI

into Income

1

Location of Gain

(Loss) Recognized

in Income on

Derivative

2

Amount of Gain

(Loss)

Recognized in

Income on

Derivative

2

2008

2007

2008

2007

2008

2007

$(738)

$381

Aircraft Fuel

$ 378

$ 165

Aircraft Fuel

$ 2

$ 74

1 Effective portion of gain (loss)

2 Ineffective portion of gain (loss)

The Company is also exposed to credit losses in the event of non-performance by counterparties to these financial

instruments, and although no assurances can be given, the Company does not expect any of the counterparties to

fail to meet its obligations. The credit exposure related to these financial instruments is represented by the fair

value of contracts with a positive fair value at the reporting date, reduced by the effects of master netting

agreements. To manage credit risks, the Company selects counterparties based on credit ratings, limits its

exposure to a single counterparty under defined guidelines, and monitors the market position of the program and

its relative market position with each counterparty. The Company also maintains industry-standard security

agreements with a number of its counterparties which may require the Company or the counterparty to post

collateral if the value of selected instruments exceed specified mark-to-market thresholds or upon certain changes

in credit ratings. A deterioration of the Company’s liquidity position may negatively affect the Company’s ability to

hedge fuel in the future.

Certain of the Company’s derivative instrument contracts provide that if the Company’s unrestricted cash balance

or credit ratings remain above certain levels, loss positions on these instruments need not be fully collateralized. If

the Company’s unrestricted cash balance or credit rating were to fall below these levels, it would trigger additional

collateral to be deposited with the counterparty up to 100 percent of the loss position of the derivative contracts.

As of December 31, 2008, the aggregate fair value of all derivative instruments with credit-risk-related contingent

features that are in a net liability position is $528 million, for which the Company had posted collateral of $575

million. The Company was over-collateralized as of December 31, 2008 due to a timing lag in collateral

reconciliation of $92 million by a certain counterparty. Excluding the impact of this timing lag, if all credit-risk-

contingent features underlying these agreements had been triggered on December 31, 2008, the Company would

have been required to post collateral of 100 percent of the loss position referred to above, or $528 million.

During 2008, a counterparty to certain of the Company’s fuel hedging derivative contracts filed for protection under

Chapter 11 of the Federal Bankruptcy Code. Per the contract, the Company was able to terminate its hedge

positions with this counterparty as a result of the counterparty’s default. Due to the decline in fuel prices

subsequent to the Chapter 11 filing, the Company was in a liability position to this counterparty at the time the

hedge position was terminated. The Company incurred a charge of $26 million associated with these contracts

during the period subsequent to the Chapter 11 filing and prior to termination, when the derivative contracts no

longer qualified for hedge accounting under SFAS 133. The charge was recorded to Miscellaneous-net in the

accompanying consolidated statement of operations. Had the Company retained these hedge positions, this

charge would have been incurred as fuel expense over the next two years assuming a static fuel price from the

termination date.

In fourth quarter of 2008, the Company modified its fuel hedge portfolio, effectively settling certain derivatives

hedging 2009 jet fuel purchases. The Company entered into fuel hedging collars to unwind certain trades with two

of the Company’s counterparties. The Company has de-designated these unwound hedges as prescribed by SFAS

133, and entered into four directly counteractive economic derivatives to, in effect, settle these positions. At the

date of de-designation of these hedges, the Company had recorded a $205 million loss in Accumulated other

comprehensive income which will be reclassified into Aircraft fuel expense in 2009. The fair value of these

offsetting positions not designated as hedges under SFAS 133 as of December 31, 2008 was a $188 million asset

recorded in Fuel derivative contracts and a $188 million liability recorded in Fuel derivative liability.