American Airlines 2008 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2008 American Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

|

|

69

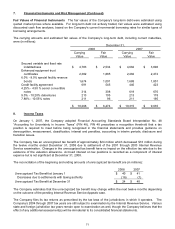

7. Financial Instruments and Risk Management (Continued)

In accordance with Statement of Financial Accounting Standards No. 133, “Accounting for Derivative Instruments

and Hedging Activity” (SFAS 133), the Company assesses, both at the inception of each hedge and on an on-

going basis, whether the derivatives that are used in its hedging transactions are highly effective in offsetting

changes in cash flows of the hedged items. Derivatives that meet the requirements of SFAS 133 are granted

special hedge accounting treatment, and the Company’s hedges generally meet these requirements. Accordingly,

the Company’s fuel derivative contracts are accounted for as cash flow hedges, and the fair value of the

Company’s hedging contracts is recorded in Current Assets or Current Liabilities in the accompanying

consolidated balance sheets until the underlying jet fuel is purchased. The Company determines the ineffective

portion of its fuel hedge contracts by comparing the cumulative change in the total value of the fuel hedge

contract, or group of fuel hedge contracts, to the cumulative change in a hypothetical jet fuel hedge. If the total

cumulative change in value of the fuel hedge contract more than offsets the total cumulative change in a

hypothetical jet fuel hedge, the difference is considered ineffective and is immediately recognized as a component

of Aircraft fuel expense. Effective gains or losses on fuel hedging contracts are deferred in Accumulated other

comprehensive income (loss) and are recognized in earnings as a component of Aircraft fuel expense when the

underlying jet fuel being hedged is used.

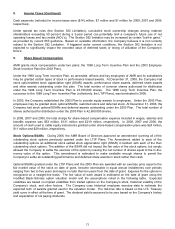

Ineffectiveness is inherent in hedging jet fuel with derivative positions based in crude oil or other crude oil related

commodities. In assessing effectiveness, the Company uses a regression model to determine the correlation of

the change in prices of the commodities used to hedge jet fuel (e.g. NYMEX Heating oil) to the change in the price

of jet fuel. The Company also monitors the actual dollar offset of the hedges’ market values as compared to

hypothetical jet fuel hedges. The fuel hedge contracts are generally deemed to be “highly effective” if the R-

squared is greater than 80 percent and dollar offset correlation is within 80 percent to 125 percent. The Company

discontinues hedge accounting prospectively if it determines that a derivative is no longer expected to be highly

effective as a hedge or if it decides to discontinue the hedging relationship. Subsequently, any changes in the fair

value of these derivatives are marked to market through earnings in the period of change.

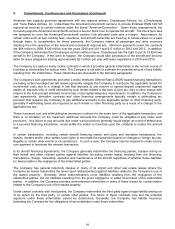

For the years ended December 31, 2008, 2007 and 2006, the Company recognized net gains of approximately

$380 million, $239 million and $97 million, respectively, as a component of fuel expense on the accompanying

consolidated statements of operations related to its fuel hedging agreements, including the ineffective portion of

the hedges. In addition, in 2006, the Company recognized a loss of $102 million in Miscellaneous – net for

changes in market value of hedges that did not qualify for hedge accounting during certain periods in 2006. The

fair value of the Company’s fuel hedging agreements at December 31, 2008 and 2007, representing the amount

the Company would receive (pay) to terminate the agreements, totaled ($450) million and $353 million,

respectively, which excludes a payable and a receivable, respectively, related to contracts that settled in

December of each year. As of December 31, 2008, the Company estimates that during the next twelve months it

will reclassify from Accumulated other comprehensive loss into earnings approximately $711 million in net losses

(based on prices as of December 31, 2008) related to its fuel derivative hedges, including losses from terminated

contracts with a bankrupt counterparty and unwound trades.

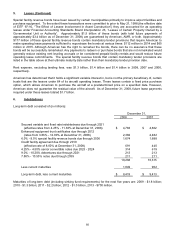

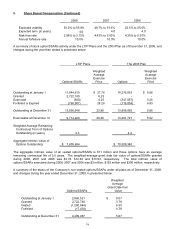

The impact of cash flow hedges on the Company’s consolidated financial statements for the years ending

December 31, 2008 and 2007, respectively, is depicted below (in millions):

Fair Value of Aircraft Fuel Derivative Instruments (all cash flow hedges under SFAS 133)

Asset Derivatives as of December 31,

Liability Derivatives as of December 31,

2008

2007

2008

2007

Balance

Sheet

Location

Fair

Value

Balance

Sheet

Location

Fair

Value

Balance

Sheet

Location

Fair

Value

Balance

Sheet

Location

Fair

Value

Fuel

derivative

contracts

$ -

Fuel

derivative

contracts

$ 416

Fuel

derivative

liability

$ 528

Accrued

liabilities

$ -