American Express 2006 Annual Report Download - page 103

Download and view the complete annual report

Please find page 103 of the 2006 American Express annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

-

115

-

116

|

|

[ 101 ]

notes to consolidated fi nancial statements

american express company

87, 88, 106, and 132(R). This standard requires that

companies record an asset or liability on the Consolidated

Balance Sheet equal to the over or under funded status

of their defined benefit and other postretirement benefit

plans effective for fiscal years ending after December

15, 2006. For each plan, the funded status is defined

by SFAS No. 158 as the difference between the fair

value of plan assets (for funded plans) and the respective

plan’s projected benefit obligation. The projected

benefit obligation represents a liability based on the plan

participant’s service to date and their expected future

compensation at their projected retirement date. Upon

adoption of SFAS No. 158 and recognition of the funded

status on the Company’s Consolidated Balance Sheet,

all previously unrecognized amounts (e.g. unrecognized

gains or losses and prior service cost) are reflected in

accumulated other comprehensive income (loss), net of

tax, in a one-time cumulative effect adjustment. Any

future changes in unrecognized gains or losses and prior

service cost will be recognized in other comprehensive

income, net of tax, in the periods in which they occur.

Under SFAS No. 158, accounting for plan expense and

payments will remain unchanged.

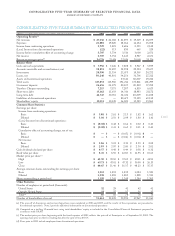

The following table provides the cumulative effect

of the change in accounting principle with respect to

recognizing the net funded status of defined benefit

pension plans (the Plan, the SRP and other international

plans) in the Consolidated Balance Sheet as of December

31, 2006.

(Millions)

Pre-SFAS

No. 158

SFAS

No. 158

impact

Post-

SFAS

No. 158

Accrued benefit

liability (a) $ (248) $ (39) $(287)

Prepaid benefit asset (b) $ 440 $ (416) 24

Net funded status $(263)

Accumulated other

comprehensive loss,

net of tax (c) $ 21 $ 310 $ 331

(a) The post-SFAS No. 158 accrued benefit liability represents the

excess of the projected benefit obligation over the fair value of

the plan assets for all plans in an underfunded position. The

projected benefit obligation and related fair value of plan assets

for these plans was $1.5 billion and $1.2 billion, respectively, at

December 31, 2006 and $2.3 billion and $2.1 billion, respectively,

at December 31, 2005.

(b) The post-SFAS No. 158 prepaid benefit asset represents the

excess of the fair value of the plan assets over the projected benefit

obligation for all plans in an overfunded position.

(c) The post-SFAS No. 158 accumulated other comprehensive

loss, net of tax includes the unrecognized gains and losses and

unamortized prior service cost related to the plans. See the table

below for further information.

Accumulated Other Comprehensive Loss

The following table provides the items comprising the

amount in accumulated other comprehensive loss as of

December 31:

(Millions) 2006

Net actuarial loss $ 474

Net prior service cost 13

Tota l , preta x effect 487

Tax impact (156)

Total, net of taxes $ 331

The estimated portion of the net actuarial loss and net

prior service cost above that is expected to be recognized

as a component of net periodic benefit cost in 2007 is

$40 million and $2 million, respectively.

Plan Assets and Obligations

The following tables provide a reconciliation of the

changes in the plans’ projected benefit obligation, the

fair value of assets and the net funded status for all

plans:

Reconciliation of Change in Projected

Benefit Obligation

(Millions) 2006 2005

Projected benefit obligation, October 1

prior year

$2,392 $2,168

Service cost 117 104

Interest cost 127 117

Benefits paid (55) (59)

Actuarial loss 33 220

Settlements/curtailments (95) (51)

Foreign currency exchange rate changes 147 (107)

Projected benefit obligation at

September 30,

$2,666 $2,392

Reconciliation of Change in Fair Value of Plan Assets

(Millions) 2006 2005

Fair value of plan assets, October 1 prior

year $2,135 $1,975

Actual return on plan assets 232 326

Employer contributions 46 41

Benefits paid (55) (59)

Settlements (95) (51)

Foreign currency exchange rate changes 135 (97)

Fair value of plan assets at

September 30, $2,398 $2,135