Apple 1995 Annual Report Download - page 19

Download and view the complete annual report

Please find page 19 of the 1995 Apple annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

|

|

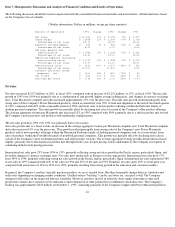

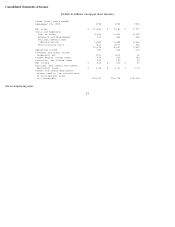

management, higher 1994 sales levels attributable to various pricing and promotional actions, and strong sales of new product inventory which

had been built up in preparation for the introduction of Power Macintosh. Profit levels improved as operating expenses decreased due to the

Company's implementation of restructuring actions initiated in the third quarter of 1993.

Cash generated by operations in 1994 was partially offset by cash used for restructuring and an increase in accounts receivable. The increase in

accounts receivable reflected an increase in sales levels achieved during 1994. The balance of accrued restructuring costs decreased as the

restructuring actions initiated in the third quarter of 1993 continued to be implemented. In addition, in the third quarter of 1994, the Company

lowered its estimate of the costs associated with the restructuring and recorded an adjustment that increased income by $127 million ($79

million, or $0.66 per share, after taxes). This adjustment primarily reflected the modification or cancelation of certain elements of the

Company's original restructuring plan because of changing business and economic conditions that made certain elements of the restructuring

plan financially less attractive than originally anticipated.

Excluding short-term investments, net cash used for investments increased in 1995 compared with 1994 and 1993 levels. Net cash used for the

purchase of property, plant, and equipment totaled $159 million in 1995, and was primarily made up of increases in manufacturing machinery

and equipment. The Company anticipates that capital expenditures in 1996 will remain relatively consistent with 1995 expenditure levels.

The Company leases the majority of its facilities and certain of its equipment under noncancelable operating leases. In 1995, rent expense

under all operating leases was approximately $127 million. The Company's future lease commitments are discussed on page 34 of the Notes to

Consolidated Financial Statements.

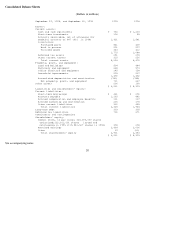

Short-term borrowings at September 29, 1995, were approximately $169 million higher than at September 30, 1994. These borrowings were

primarily made to fund expected working capital growth in certain markets worldwide. In general, the Company's short-

term borrowings reflect

borrowings made under its commercial paper program and short-

term loans from certain commercial banks. In particular, Apple Japan, Inc. and

Apple Computer BV (Netherlands), subsidiaries of the Company, held short-

term borrowings from several banks, totaling approximately $199

million and $262 million, respectively, at September 29, 1995.

The Company's balance of long-term debt remained relatively constant during 1995. In 1994, $300 million aggregate principal amount of 6.5%

unsecured notes were issued under an omnibus shelf registration statement filed with the Securities and Exchange Commission. This shelf

registration was for the registration of debt and other securities for an aggregate offering amount of $500 million. The notes were sold at

99.925% of par, for an effective yield to maturity of 6.51%. The notes pay interest semi-annually and mature on February 15, 2004. The 6.51%

fixed rate was subsequently effectively converted to a floating rate through ten-year interest rate swaps based on the three-month U.S. dollar

London Interbank Offered Rate ("LIBOR"). To mitigate the credit risk associated with these ten-year swap transactions, the Company entered

into margining agreements with its third-party bank counterparties. Margining under these agreements does not start until 1997. Furthermore,

these agreements would require the Company to post margin only if certain credit risk thresholds were exceeded. It is anticipated that any

margin the Company may be required to post in the future would not have a material adverse effect on the Company's liquidity position.

The Company expects that it will continue to incur short- and long-term borrowings from time to time to finance U.S. working capital needs

and capital expenditures, because a substantial portion of the Company's cash, cash equivalents, and short-term investments is held by foreign

subsidiaries, generally in U.S. dollar-denominated holdings. Amounts held by foreign subsidiaries would be subject to U.S. income taxation

upon repatriation to the United States; the Company's financial statements fully provide for any related tax liability on amounts that may be

repatriated. Refer to the Income Taxes footnote on pages 31 - 32 of the Notes to Consolidated Financial Statements for further discussion.

The Company believes that its balances of cash, cash equivalents, and short-term investments, together with funds generated from operations

and short- and long-term borrowing capabilities, will be sufficient to meet its operating cash requirements on a short- and long-term basis.

17