DTE Energy 2011 Annual Report Download - page 19

Download and view the complete annual report

Please find page 19 of the 2011 DTE Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

|

|

17

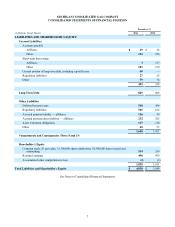

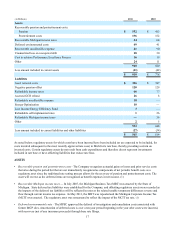

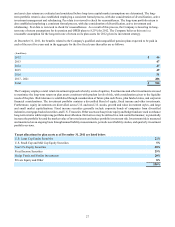

(in Millions)

Assets

Recoverable pension and postretirement costs:

Pension

Postretirement costs

Recoverable Michigan income taxes

Deferred environmental costs

Recoverable uncollectible expense

Unamortized loss on reacquired debt

Cost to achieve Performance Excellence Process

Other

Less amount included in current assets

Liabilities

Asset removal costs

Negative pension offset

Refundable income taxes

Accrued GCR refund

Refundable uncollectible expense

Energy Optimization

Low Income Energy Efficiency Fund

Refundable self implemented rates

Refundable Michigan income taxes

Other

Less amount included in current liabilities and other liabilities

2011

$ 552

196

54

49

41

28

16

24

960

(41)

$ 919

$ 346

120

66

26

18

10

3

1

—

2

592

(27)

$ 565

2010

$ 413

152

64

41

90

30

19

11

820

(42)

$ 778

$ 347

129

77

8

—

—

—

26

56

5

648

(34)

$ 614

As noted below, regulatory assets for which costs have been incurred have been included (or are expected to be included, for

costs incurred subsequent to the most recently approved rate case) in MichCon's rate base, thereby providing a return on

invested costs. Certain regulatory assets do not result from cash expenditures and therefore do not represent investments

included in rate base or have offsetting liabilities that reduce rate base.

ASSETS

• Recoverable pension and postretirement costs - The Company recognizes actuarial gains or losses and prior service costs

that arise during the period but that are not immediately recognized as components of net periodic benefit costs as a

regulatory asset since the traditional rate setting process allows for the recovery of pension and postretirement costs. The

asset will reverse as the deferred items are recognized as benefit expenses in net income. (1)

• Recoverable Michigan income taxes — In July 2007, the Michigan Business Tax (MBT) was enacted by the State of

Michigan. State deferred tax liabilities were established for the Company, and offsetting regulatory assets were recorded as

the impacts of the deferred tax liabilities will be reflected in rates as the related taxable temporary differences reverse and

flow through current income tax expense. In May 2011, the MBT was repealed and the Michigan Corporate Income Tax

(MCIT) was enacted. The regulatory asset was remeasured to reflect the impact of the MCIT tax rate. (1)

• Deferred environmental costs - The MPSC approved the deferral of investigation and remediation costs associated with

former MGP sites. Amortization of deferred costs is over a ten-year period beginning in the year after costs were incurred,

with recovery (net of any insurance proceeds) through base rate filings.