DTE Energy 2011 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 2011 DTE Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

|

|

18

• Recoverable uncollectible expense - Receivable for the MPSC approved uncollectible expense tracking mechanism that

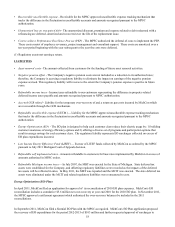

tracks the difference in the fluctuation in uncollectible accounts and amounts recognized pursuant to the MPSC

authorization.

• Unamortized loss on reacquired debt - The unamortized discount, premium and expense related to debt redeemed with a

refinancing are deferred, amortized and recovered over the life of the replacement issue.

• Cost to achieve Performance Excellence Process (PEP) - The MPSC authorized the deferral of costs to implement the PEP.

These costs consist of employee severance, project management and consultant support. These costs are amortized over a

ten-year period beginning with the year subsequent to the year the costs were deferred.

(1) Regulatory assets not earning a return.

LIABILITIES

• Asset removal costs - The amount collected from customers for the funding of future asset removal activities.

• Negative pension offset - The Company's negative pension costs are not included as a reduction to its authorized rates;

therefore, the Company is accruing a regulatory liability to eliminate the impact on earnings of the negative pension

expense accrued. This regulatory liability will reverse to the extent the Company's pension expense is positive in future

years.

• Refundable income taxes - Income taxes refundable to our customers representing the difference in property-related

deferred income taxes payable and amounts recognized pursuant to MPSC authorization.

• Accrued GCR refund - Liability for the temporary over-recovery of and a return on gas costs incurred by MichCon which

are recoverable through the GCR mechanism.

• Refundable uncollectible expense (UETM )— Liability for the MPSC approved uncollectible expense tracking mechanism

that tracks the difference in the fluctuation in uncollectible accounts and amounts recognized pursuant to the MPSC

authorization.

• Energy Optimization (EO) - The EO plan is designed to help each customer class reduce their electric usage by: 1) building

customer awareness of energy efficiency options and 2) offering a diverse set of programs and participation options that

result in energy savings for each customer class. The regulatory liability represents EO surcharges collected on excess of

EO plan expenditures incurred.

• Low Income Energy Efficiency Fund (LIEEF) — Escrow of LIEEF funds collected by MichCon as ordered by the MPSC

pursuant to July 2011 Michigan Court of Appeals decision.

• Refundable self implemented rates - Amounts refundable to customers for base rates implemented by MichCon in excess of

amounts authorized in MPSC orders.

• Refundable Michigan income taxes — In July 2007, the MBT was enacted by the State of Michigan. State deferred tax

assets were established for the Company, and offsetting regulatory liabilities were recorded as the impacts of the deferred

tax assets will be reflected in rates. In May 2011, the MBT was repealed and the MCIT was enacted. The state deferred tax

assets were eliminated under the MCIT and related regulatory liabilities were remeasured to zero.

Energy Optimization (EO) Plans

In April 2011, MichCon filed an application for approval of its reconciliation of 2010 EO plan expenses. MichCon's EO

reconciliation includes a cumulative $5.6 million net over-recovery at year end 2010 for the 2010 EO plan. In November 2011,

the MPSC approved a settlement agreement which authorized the over-recovery balances be included in the 2011

reconciliations.

In September 2011, MichCon filed a biennial EO Plan with the MPSC as required. MichCon's EO Plan application proposed

the recovery of EO expenditures for the period 2012-2015 of $103 million and further requested approval of surcharges to