DTE Energy 2012 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2012 DTE Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

|

|

Table of Contents

Various non-utility subsidiaries of the Company have entered into contracts which contain ratings triggers and are guaranteed by DTE Energy. These

contracts contain provisions which allow the counterparties to request that the Company post cash or letters of credit as collateral in the event that DTE

Energy’s credit rating is downgraded below investment grade. As of December 31, 2012, the value of the transactions for which the Company would have

been exposed to collateral requests had DTE Energy’s credit rating been below investment grade on such date was approximately $ 326 million. In

circumstances where an entity is downgraded below investment grade and collateral requests are made as a result, the requesting parties often agree to accept

less than the full amount of their exposure to the downgraded entity. In addition, the Company maintains adequate credit facilities to meet this obligation

should such an occurrence arise.

We believe we have sufficient operating flexibility, cash resources and funding sources to maintain adequate amounts of liquidity and to meet our future

operating cash and capital expenditure needs. However, virtually all of our businesses are capital intensive, or require access to capital, and the inability to

access adequate capital could adversely impact earnings and cash flows.

See Notes 11, 12, 15, 17, and 20 of the Notes to Consolidated Financial Statements in Item 8 of this Report.

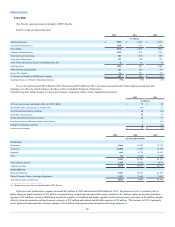

Contractual Obligations

The following table details our contractual obligations for debt redemptions, leases, purchase obligations and other long-term obligations as of

December 31, 2012:

Long-term debt:

Mortgage bonds, notes and other $6,865

$ 634

$1,066

$ 474

$4,691

Securitization bonds 479

177

302

—

—

Junior subordinated debentures 480

—

—

—

480

Capital lease obligations 20

7

10

3

—

Interest 5,890

415

688

577

4,210

Operating leases 233

38

56

41

98

Electric, gas, fuel, transportation and storage purchase obligations (a) 4,229

1,856

1,584

222

567

Other long-term obligations (b)(c)(d) 148

80

39

13

16

Total obligations $18,344

$3,207

$3,745

$1,330

$10,062

_______________________________________

(a) Excludes amounts associated with full requirements contracts where no stated minimum purchase volume is required.

(b) Includes liabilities for unrecognized tax benefits of $11 million.

(c) Excludes other long-term liabilities of $179 million not directly derived from contracts or other agreements.

(d) At December 31, 2012, we met the minimum pension funding levels required under the Employee Retirement Income Security Act of 1974 (ERISA) and the Pension Protection Act

of 2006 for our defined benefit pension plans. We may contribute more than the minimum funding requirements for our pension plans and may also make contributions to our benefit

plans and our postretirement benefit plans; however, these amounts are not included in the table above as such amounts are discretionary. Planned funding levels are disclosed in

the Capital Resources and Liquidity and Critical Accounting Estimates sections herein and in Note 20 of the Notes to Consolidated Financial Statements in Item 8 of this Report.

Credit Ratings

Credit ratings are intended to provide banks and capital market participants with a framework for comparing the credit quality of securities and are not

a recommendation to buy, sell or hold securities. The Company’s credit ratings affect our cost of capital and other terms of financing as well as our ability to

access the credit and commercial paper markets. Management believes that our current credit ratings provide sufficient access to the capital markets. However,

disruptions in the banking and capital markets not specifically related to us may affect our ability to access these funding sources or cause an increase in the

return required by investors.

As part of the normal course of business, DTE Electric, DTE Gas and various non-utility subsidiaries of the Company routinely enter into physical or

financially settled contracts for the purchase and sale of electricity, natural gas, coal, capacity, storage and other energy-related products and services. Certain

of these contracts contain provisions which allow the counterparties to request that the Company post cash or letters of credit in the event that the senior

unsecured debt rating of DTE Energy is downgraded below investment grade. Certain of these contracts for DTE Electric and DTE Gas contain similar

provisions in the event that the senior unsecured debt rating of the particular utility is downgraded below investment grade.

38