DTE Energy 2012 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2012 DTE Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

|

|

Table of Contents

The fair values we calculate for our derivatives may change significantly as inputs and assumptions are updated for new information. Actual cash

returns realized on our derivatives may be different from the results we estimate using models. As fair value calculations are estimates based largely on

commodity prices, we perform sensitivity analyses on the fair values of our forward contracts. See sensitivity analysis in Item 7A. Quantitative and

Qualitative Disclosures About Market Risk. See also the Fair Value section, herein. See Notes 3 and 4 of the Notes to Consolidated Financial Statements in

Item 8 of this Report.

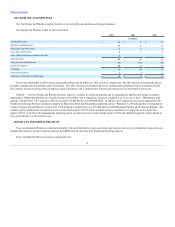

Allowance for Doubtful Accounts

We establish an allowance for doubtful accounts based on historical losses and management's assessment of existing economic conditions, customer

trends, and other factors. The allowance for doubtful accounts for our two utilities is calculated using the aging approach that utilizes rates developed in

reserve studies and applies these factors to past due receivable balances. We believe the allowance for doubtful accounts is based on reasonable estimates.

Asset Impairments

Goodwill

Certain of our reporting units have goodwill or allocated goodwill resulting from purchase business combinations. We perform an impairment test for

each of our reporting units with goodwill annually or whenever events or circumstances indicate that the value of goodwill may be impaired.

In September 2011, the FASB issued ASU No. 2011-08, Intangibles-Goodwill and Other (Topic 350)-Testing Goodwill for Impairment, which is

intended to simplify how entities test for goodwill impairment by permitting an entity the option of performing a qualitative assessment to determine whether

further impairment testing is necessary (“step zero”). The standard is effective for annual and interim goodwill impairments tests for fiscal years beginning

after December 15, 2011. We did not apply step zero for the 2012 goodwill impairment test and proceeded directly to step one of the test.

In performing Step 1 of the impairment test, we compare the fair value of the reporting unit to its carrying value including goodwill. If the carrying value

including goodwill were to exceed the fair value of a reporting unit, Step 2 of the test would be performed. Step 2 of the impairment test requires the carrying

value of goodwill to be reduced to its fair value, if lower, as of the test date.

For Step 1 of the test, we estimate the reporting unit's fair value using standard valuation techniques, including techniques which use estimates of

projected future results and cash flows to be generated by the reporting unit. Such techniques generally include a terminal value that utilizes an earnings

multiple approach, which incorporates the current market values of comparable entities. These cash flow valuations involve a number of estimates that require

broad assumptions and significant judgment by management regarding future performance. We also employ market-based valuation techniques to test the

reasonableness of the indications of value for the reporting units determined under the cash flow technique.

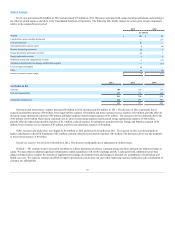

We performed our annual impairment test as of October 1, 2012 and determined that except for the Unconventional Gas Production reporting unit, the

estimated fair value of each reporting unit exceeded its carrying value, and no impairment existed. The $2 million of goodwill attributable to the

Unconventional Gas Production reporting unit was written off in the fourth quarter of 2012 in connection with its sale. As part of the annual impairment test,

we also compared the aggregate fair value of our reporting units to our overall market capitalization. The implied premium of the aggregate fair value over

market capitalization is likely attributable to an acquisition control premium (the price in excess of a stock's market price that investors typically pay to gain

control of an entity). The results of the test and key estimates that were incorporated are as follows.

40