DTE Energy 2012 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 2012 DTE Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

|

|

Table of Contents

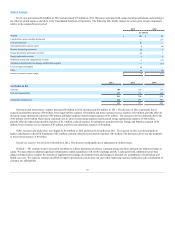

The amount of such collateral which could be requested fluctuates based upon commodity prices and the provisions and maturities of the underlying

transactions and could be substantial. Also, upon a downgrade below investment grade, we could have restricted access to the commercial paper market and if

DTE Energy is downgraded below investment grade our non-utility businesses, especially the Energy Trading and Power and Industrial Projects segments,

could be required to restrict operations due to a lack of available liquidity. A downgrade below investment grade could potentially increase the borrowing costs

of DTE Energy and its subsidiaries and may limit access to the capital markets. The impact of a downgrade will not affect our ability to comply with our

existing debt covenants. While we currently do not anticipate such a downgrade, we cannot predict the outcome of current or future credit rating agency

reviews.

In January 2012, Fitch Ratings raised DTE Electric's senior secured debt rating from 'A-' to 'A' and raised DTE Gas' senior secured debt rating from

'BBB+' to 'A-'. At the same time, Fitch Ratings revised the outlook for DTE Gas from stable to positive. In January 2013, Fitch raised DTE Gas' senior

secured debt rating from 'A-' to 'A' and revised the outlook from positive to stable. In February 2012, Moody's revised the outlook of DTE Energy, DTE

Electric and DTE Gas from stable to positive. In February 2013, Moody's raised DTE Energy's senior unsecured debt rating from 'Baa2' to 'Baa1', DTE

Electric's senior secured debt rating from 'A2' to 'A1', and DTE Gas' senior secured debt rating from 'A2 to A1'. At the same time, Moody's revised the outlook

of DTE Energy, DTE Electric and DTE Gas from positive to stable.

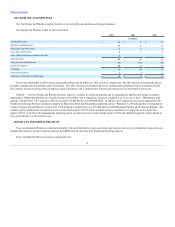

The preparation of financial statements in conformity with generally accepted accounting principles require that management apply accounting policies

and make estimates and assumptions that affect results of operations and the amounts of assets and liabilities reported in the financial statements.

Management believes that the areas described below require significant judgment in the application of accounting policy or in making estimates and

assumptions in matters that are inherently uncertain and that may change in subsequent periods. Additional discussion of these accounting policies can be

found in the Notes to Consolidated Financial Statements in Item 8 of this Report.

Regulation

A significant portion of our business is subject to regulation. This results in differences in the application of generally accepted accounting principles

between regulated and non-regulated businesses. DTE Electric and DTE Gas are required to record regulatory assets and liabilities for certain transactions that

would have been treated as revenue or expense in non-regulated businesses. Future regulatory changes or changes in the competitive environment could result in

the discontinuance of this accounting treatment for regulatory assets and liabilities for some or all of our businesses. Management believes that currently

available facts support the continued use of regulatory assets and liabilities and that all regulatory assets and liabilities are recoverable or refundable in the

current rate environment.

See Note 11 of the Notes to Consolidated Financial Statements in Item 8 of this Report.

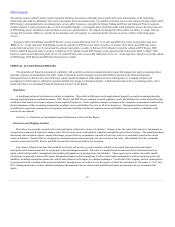

Derivatives and Hedging Activities

Derivatives are generally recorded at fair value and shown as Derivative Assets or Liabilities. Changes in the fair value of the derivative instruments are

recognized in earnings in the period of change, unless the derivative meets certain defined conditions and qualifies as an effective hedge. The normal purchases

and normal sales exception requires, among other things, physical delivery in quantities expected to be used or sold over a reasonable period in the normal

course of business. Contracts that are designated as normal purchases and normal sales are not recorded at fair value. Substantially all of the commodity

contracts entered into by DTE Electric and DTE Gas meet the criteria specified for this exception.

Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market

participants at the measurement date in a principal or most advantageous market. Fair value is a market-based measurement that is determined based on

inputs, which refer broadly to assumptions that market participants use in pricing assets and liabilities. These inputs can be readily observable, market

corroborated or generally unobservable inputs. Management makes certain assumptions it believes that market participants would use in pricing assets and

liabilities, including assumptions about risk, and the risks inherent in the inputs to valuation techniques. Credit risk of the Company and our counterparties

is incorporated in the valuation of the assets and liabilities through the use of credit reserves, the impact of which was immaterial at December 31, 2012 and

2011. Management believes it uses valuation techniques that maximize the use of observable market-based inputs and minimize the use of unobservable

inputs.

39