LabCorp 2009 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2009 LabCorp annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

|

|

LABORATORY CORPORATION OF AMERICA

Management’s Discussion and Analysis

of Financial Condition and Results of Operations

LABORATORY CORPORATION OF AMERICA 27

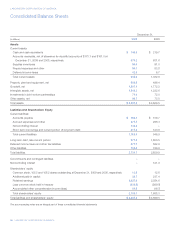

Contractual Cash Obligations

Payments Due by Period

2011- 2013- 2015 and

Total 2010 2012 2014 thereafter

Operating lease obligations $ 366.6 $ 100.4 $ 134.9 $ 69.2 $ 62.1

Contingent future licensing payments (a) 38.4 0.5 6.6 13.2 18.1

Minimum royalty payments 19.8 5.8 5.0 5.3 3.7

Zero-coupon subordinated notes (b) 292.2 292.2 – – –

Scheduled interest payments on Senior Notes 151.8 33.3 66.6 37.8 14.1

Term loan and revolving credit facility 500.0 125.0 375.0 – –

Long-term debt, other than term loan, revolving credit facility and

zero-coupon subordinated notes 602.2 0.7 1.5 350.0 250.0

Total contractual cash obligations (c)(d)(e) $ 1,971.0 $ 557.9 $ 589.6 $ 475.5 $ 348.0

(a) Contingent future licensing payments will be made if certain events take place, such as the launch of a specific test, the transfer of certain technology, and when specified revenue milestones are met.

(b) Holders of the zero-coupon subordinated notes may require the Company to purchase in cash all or a portion of their notes on September 11, 2011 at $819.54 per note ($302.2 in the aggregate).

Should the holders put the notes to the Company on that date, the Company believes that it will be able to satisfy this contingent obligation with cash on hand, borrowings on the revolving credit facility,

and additional financing if necessary. As announced by the Company on January 5, 2010, holders of the zero-coupon subordinated notes may choose to convert their notes during the first quarter of

2010 subject to terms as defined in the note agreement. See “Note 11 to Consolidated Financial Statements” for further information regarding the Company’s zero-coupon subordinated notes.

(c) The table does not include obligations under the Company’s pension and postretirement benefit plans, which are included in “Note 16 to Consolidated Financial Statements.” Benefits under the Company’s

postretirement medical plan are made when claims are submitted for payment, the timing of which is not practicable to estimate.

(d) The table does not include the Company’s contingent obligation to reimburse up to $200.0 in transition costs incurred during the first three years of the UnitedHealthcare contract. The Company anticipates

that it has approximately $22.8 remaining to be paid out on this contingent obligation.

(e) The table does not include the Company’s reserves for unrecognized tax benefits. The Company had a $73.7 and $86.7 reserve for unrecognized tax benefits, including interest and penalties, at

December 31, 2009 and 2008, respectively, which is included in “Note 13 to Consolidated Financial Statements.” Substantially all of these tax reserves are classified in other long-term liabilities

in the Company’s Consolidated Balance Sheets at December 31, 2009 and 2008.

Off-Balance Sheet Arrangements

The Company does not have transactions or relationships with

“special purpose” entities, and the Company does not have any

off-balance sheet financing other than normal operating leases.

Other Commercial Commitments

At December 31, 2009, the Company provided letters of credit

aggregating approximately $39.5, primarily in connection with

certain insurance programs. Letters of credit provided by the

Company are secured by the Company’s senior credit facilities

and are renewed annually, around mid-year.

Effective January 1, 2008 the Company acquired additional

partnership units in its Ontario, Canada (“Ontario”) joint venture

for approximately $140.9 in cash (net of cash acquired), bringing

the Company’s percentage interest owned to 85.6%. Concurrent

with this acquisition, the terms of the joint venture’s partnership

agreement were amended. Based upon the amended terms of

this agreement, the Company began including the consolidated

operating results, financial position and cash flows of the Ontario

joint venture in the Company’s consolidated financial statements

on January 1, 2008. The amended joint venture’s partnership

agreement also enables the holders of the noncontrolling interest

to put the remaining partnership units to the Company in defined

future periods, at an initial amount equal to the consideration

paid by the Company in 2008, and subject to adjustment

based on market value formulas contained in the agreement.

The initial difference of $123.0 between the value of the put and

the underlying noncontrolling interest was recorded as additional

noncontrolling interest liability and as a reduction to additional

paid-in capital in the consolidated financial statements. The con-

tractual value of the put, in excess of the current noncontrolling

interest of $23.5, totals $118.9 at December 31, 2009.

In December 2009, the Company received notification

from the holders of the noncontrolling interest in the Ontario

joint venture that they intend to put their remaining partner-

ship units to the Company in accordance with the terms of

the joint venture’s partnership agreement. These units were

acquired on February 8, 2010 for CN$147.8. On February 17,

2010, the Company completed a transaction to sell the units

acquired from the previous noncontrolling interest holder to a new

Canadian partner for the same price. Upon the completion of

these two transactions, the Company’s financial ownership

percentage in the joint venture partnership remained unchanged

at 85.6%. Concurrent with the sale to the new partner, the

partnership agreement for the Ontario Canada joint venture

was amended and restated with substantially the same terms

as the previous agreement.