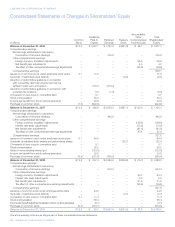

LabCorp 2009 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 2009 LabCorp annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

|

|

LABORATORY CORPORATION OF AMERICA

Management’s Discussion and Analysis

of Financial Condition and Results of Operations

28 LABORATORY CORPORATION OF AMERICA

At December 31, 2009, the Company was a guarantor on

approximately $2.5 of equipment leases. These leases were

entered into by a joint venture in which the Company owns a

50% interest and have a remaining term of approximately

three years.

Based on current and projected levels of operations, coupled

with availability under its senior credit facilities, the Company

believes it has sufficient liquidity to meet both its anticipated

short-term and long-term cash needs; however, the Company

continually reassesses its liquidity position in light of market

conditions and other relevant factors.

New Accounting Pronouncements

In June 2009, the FASB established authoritative United States

generally accepted accounting principles (“GAAP”), codifying

and superseding all pre-existing accounting standards and

literature. This newly codified GAAP is effective for financial

statements issued for interim and annual periods ending after

September 15, 2009. The Company has adopted the guidance

without any impact on the consolidated financial statements.

In December 2007, the FASB issued authoritative guidance

requiring all entities to report noncontrolling (minority) interests

in subsidiaries as equity in the consolidated financial statements.

The Company adopted the guidance as of January 1, 2009

and pursuant to the provisions of the literature, the presentation

and disclosure requirements have been applied retrospectively

for all periods presented. Due to the nature of the noncontrolling

interest put, the Company has not included the noncontrolling

interest in its Ontario joint venture in the equity section of the

accompanying consolidated balance sheets.

In December 2007, the FASB issued authoritative guidance

in connection with business combinations which was intended

to simplify existing guidance and converge rulemaking under

U.S. GAAP with international accounting rules. The guidance

applies prospectively to business combinations where the

acquisition date is on or after the beginning of the first annual

reporting period beginning on or after December 15, 2008.

The Company adopted the literature as of January 1, 2009,

and the Company began recording acquisitions in accordance

with the authoritative guidance. As a result, acquisition related

costs, primarily legal and other professional services, of $7.7

were included in selling, general and administrative expenses

for the year ended December 31, 2009.

In April 2009, the FASB issued authoritative guidance in

connection with accounting for assets acquired and liabilities

assumed in a business combination that arise from contingencies.

The guidance addresses application issues regarding the initial

recognition and measurement, subsequent measurement and

accounting, and disclosure of assets and liabilities arising from

contingencies in a business combination. Due to the fact that

the literature is applicable to acquisitions completed after

January 1, 2009 and the Company did not have any business

combinations with assets and liabilities arising from contingen-

cies in 2009, the adoption of the authoritative guidance did not

impact the Company’s consolidated financial statements.

In May 2008, the FASB issued authoritative guidance in

connection with accounting for convertible debt instruments

that may be settled in cash upon conversion. The guidance

requires that the liability and equity components of convertible

debt instruments that may be settled in cash upon conversion

(including partial cash settlement) be separately accounted for

in a manner that reflects an issuer’s nonconvertible debt bor-

rowing rate. The resulting debt discount is amortized over the

period the convertible debt is expected to be outstanding as

additional non-cash interest expense. The guidance is effective

for financial statements issued for fiscal years beginning after

December 15, 2008, and interim periods within those fiscal

years. Retrospective application to all periods presented is

required except for instruments that were not outstanding during

any of the periods that will be presented in the annual financial

statements for the period of adoption but were outstanding

during an earlier period. The literature impacts the Company’s

zero-coupon subordinated notes, and requires that additional

interest expense essentially equivalent to the portion of issuance

proceeds retroactively allocated to the instrument’s equity

component be recognized over the period from the zero-coupon

subordinated notes’ issuance in 2001 through September 2004

(the first date holders of these notes had the ability to put them

back to the Company). As anticipated, the adoption of this

authoritative guidance and its retrospective application did not

have an impact on results of operations for periods following 2004,

but it did result in an increase of $215.4 in opening additional

paid-in capital and a corresponding decrease in opening retained

earnings as of January 1, 2007, net of deferred tax impacts, on

post-2004 consolidated balance sheets.

In December 2008, the FASB issued authoritative guidance

in connection with employers’ disclosures about postretirement

benefit plan assets. The objectives of the disclosures about

plan assets in an employers’ defined benefit pension or other

postretirement plan are to provide users of financial statements