Lowe's 2007 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 2007 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

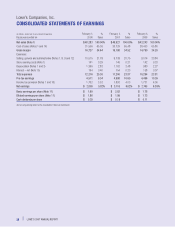

18 |LOWE’S 2007 ANNUAL REPORT

This discussion and analysis summarizes the significant factors affecting

our consolidated operating results, financial condition, liquidity and capital

resources during the three-year period ended February 1, 2008 (our fiscal

years 2007,2006 and 2005).Fiscal years 2007 and 2006 contained 52 weeks

of operating results, compared to fiscal year 2005 which contained 53 weeks.

Unless otherwise noted, all references herein for the years 2007, 2006 and

2005 represent the fiscal years ended February 1, 2008, February 2, 2007,

and February 3, 2006, respectively. This discussion should be read in

conjunction with the consolidated financial statements and notes to the

consolidated financial statements included in this annual report.

EXECUTIVE OVERVIEW

External Factors Impacting Our Business

The home improvement market is large and fragmented.While we are the world’s

second-largest home improvement retailer,we have captured a relatively small

portion of the overall home improvement market.Based on the most recent com-

prehensive data available,which is from 2006,we estimate the size of the U.S.

home improvement market to be approximately $755 billion annually,comprised

of $585 billion of product demand and $170 billion of installed labor opportunity.

This data captures a wide range of categories relevant to our business,including

major appliances and garden supplies.We believe the current home improvement

market provides ample opportunity to support our growth plans.

Net sales totaled $48.3 billion in 2007,an increase of 2.9% versus the prior

year.Thisincreasewasdrivenbyourstoreexpansionprogram.However,comparable

store sales declined 5.1% in 2007.The effects of a soft housing market,tight

mortgage market, continued deflationary pressures from lumber and plywood,

and unseasonable weather, including the exceptional drought in certain areas

of the U.S.,pressured our industry and contributed to lower than expected sales.

However, our performance relative to the industry suggests we are providing

customer-valued solutions in a challenging sales environment.

Overthepastseveralquarterswehaveused third-partyhomepriceinformation

todefine three broad marketgroupingsbasedonhome price dynamicswithin those

markets.These three categories included 1) markets that are overpriced with a

correction expected,2) markets thatare overpriced with no correctionexpected and

3)marketsthatarenotoverpriced.Themarketswith the mostovervaluedhomeprices

have generated the worst relative results. Markets with less impact on the

housing front have generated better relative comparable store sales.However,

as we have monitored these markets, we have seen erosion in comparable

store sales performance across all three market categories.

The sales environment remains challenging, and the external pressures

facing our industry will continue in 2008.We will continue to monitor the

structural drivers of demand including housing turnover, employment and

personal disposable income, as well as consumer sentiment related to home

improvement.We anticipate that at least some of the headwinds will lessen

as 2008 unfolds.The effects of the recent economic stimulus package and

the Federal Reserve interest rate cuts could aid in stabilizing many of the

factors that pressured sales in 2007.Additionally, normalized weather follow-

ing last year’s unusual pattern could lead to better relative results. Even with

these lessening headwinds, 2008 will be another challenging year as many

pressures on the home improvement consumer remain.

Managing for the Long-Term

Despite the external pressures currently facing our industry,we continue to

manage our business for the long-term.We will continue to focus on providing

customer-valued solutions and capitalizing on opportunities to gain market share

and strengthen our business. However, in the short-term managing expenses and

capital spending is crucial.We have and will continue to look for opportunities to

cut costs without sacrificing customer service.

Capturing Market Share

Customer-Focused

In this challenging sales environment, we will continue to pursue our disciplines

of providing excellent customer service and gaining profitable market share.

We continue to refine and improve our “Customer-Focused” program which

measures each store’s performance relative to five key components of customer

satisfaction, including selling skills, delivery, installed sales, checkout and

phone answering.The fact that we are providing great service and value to our

customers is evidenced by our continued strong market share gains.

Merchandising and Marketing

We continue to enhance our product offerings to customers but with an

awareness that in many markets customers are more focused on maintenance

versus enhancement.They are looking for great value at all price points.We

are also continuing to diligently manage our seasonal inventory to ensure we

maximize sales, but minimize markdowns.

A similar awareness of market differences will drive our advertising plan

in 2008.We are focused on highlighting key maintenance projects and inexpen-

sive enhancements in markets suffering the biggest slowdown in housing,while

continuing to highlight larger projects in less impacted markets.

Growth Opportunities

We have considerable growth opportunities and see the potential for 2,400 to

2,500 stores in NorthAmerica.In 2007, we opened 153 stores (149 new and

four relocated) in markets around the country,bringing our total to 1,534 stores

in the U.S.and Canada.We opened our first store in the state of Vermont in

January.We now have stores in all 50 states,and we still see many opportunities

to continue to grow market share in the markets we serve.In addition,we opened

our first stores outside the U.S.in December, and,as of the end of 2007,we had

six stores operating in the Greater Toronto Area.We are also preparing for the

opening of our first stores in Monterrey, Mexico, in 2009.

Specialty Sales

We recognize the opportunity that our Specialty Sales initiatives represent and

the importance of these businesses to our long-term growth.Our Specialty

Sales initiatives include three major categories: Installed Sales, Special Order

Sales and Commercial Business Customer sales, internally referred to as the

“Big 3.”In addition, our effort to utilize e-Commerce to drive sales and conve-

niently provide product information to customers is managed by our Specialty

Sales group. In fiscal 2007,both the Installed Sales and Special Order Sales

categories had growth in total sales, but comparable store sales fell below the

company average.These categories continue to be pressured by the weakness

in bigger-ticket and more complex projects.This weakness is more pronounced

in the most pressured housing markets.Contrasting the weakness has been

the relative strength in our Commercial Business Customer sales. Comparable

store sales and total sales growth for this category outpaced the company

average. Our efforts to build relationships and serve the needs of repair/

remodelers,property maintenance professionals,and professional tradespeople

continue to drive results.We feel that our continued focus on the categories of

this initiative that have the greatest opportunity will produce growth.

Expense Management

Centralized Management

We have always been a centrally managed company,and we value the discipline

and consistency that comes with that structure.We have built a regional and dis-

trict support infrastructure to ensure that occurs.As we have further penetrated

U.S.markets,shortening the average distance between our stores,the shortened

distance has allowed us to increase the number of stores in each district and

region.We are confident that we will continue to have the oversight we need to

MANAGEMENT’S DISCUSSION AND ANALYSIS

of Financial Condition and Results of Operations