Lowe's 2007 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2007 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

|

|

36 |LOWE’S 2007 ANNUAL REPORT

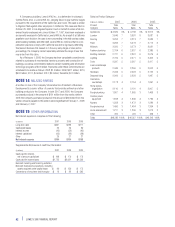

Short-term and long-term investments include restricted balances pledged

as collateral for letters of credit for the Company’s extended warranty program

and for a portion of the Company’s casualty insurance and installed sales program

liabilities. Restricted balances included in short-term investments were $167 million

at February 1,2008 and $248 million at February 2,2007. Restricted balances

included in long-term investments were $172 million at February 1, 2008 and

$32 million at February 2, 2007.

NOTE 3 PROPERTY AND ACCUMULATED

DEPRECIATION

Property is summarized by major class in the following table:

Estimated

Depreciable February 1, February 2,

(In millions) Lives, In Years 2008 2007

Cost:

Land N/A $ 5,566 $ 4,807

Buildings 7–40 10,036 8,481

Equipment 3–15 8,118 7,036

Leasehold improvements 3–40 3,063 2,484

Construction in progress N/A 2,053 2,296

Total cost 28,836 25,104

Accumulated depreciation (7,475) (6,133)

Property, less accumulated depreciation $21,361 $18,971

Included in net property are assets under capital lease of $523 million, less

accumulated depreciation of $294 million,at February 1, 2008,and $533 million,

less accumulated depreciation of $274 million, at February 2,2007.

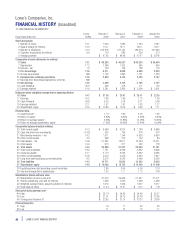

NOTE 4 SHORT-TERM BORROWINGS AND

LINES OF CREDIT

In June 2007, the Company entered into an Amended and Restated Credit

Agreement (Amended Facility) to modify the senior credit facility by extend-

ing the maturity date to June 2012 and providing for borrowings of up to

$1.75 billion. The Amended Facility supports the Company’s commercial

paper and revolving credit programs. Borrowings made are unsecured and

are priced at a fixed rate based upon market conditions at the time of fund-

ing, in accordance with the terms of the Amended Facility.The Amended

Facility contains certain restrictive covenants, which include maintenance

of a debt leverage ratio as defined by the Amended Facility. The Company

was in compliance with those covenants at February 1, 2008. Seventeen

banking institutions are participating in the Amended Facility. As of Febru-

ary 1, 2008, there was $1.0 billion outstanding under the commercial paper

program.The weighted-average interest rate on the outstanding commer-

cial paper was 3.92%. As of February 2, 2007, there was $23 million of

short-term borrowings outstanding under the senior credit facility, but no

outstanding borrowings under the commercial paper program. The interest

rate on the short-term borrowing was 5.41%.

In October 2007, the Company established a Canadian dollar (C$)

denominated credit facility in the amount of C$50 million, which provides

revolving credit support for the Company’s Canadian operations. This uncom-

mitted facility provides the Company with the ability to make unsecured

borrowings, which are priced at a fixed rate based upon market conditions

at the time of funding in accordance with the terms of the credit facility.

As of February 1, 2008, there were no borrowings outstanding under the

credit facility.

In January 2008, the Company entered into a C$ denominated credit

agreement in the amount of C$200 million for the purpose of funding the

build out of retail stores in Canada and for working capital and other general

corporate purposes. Borrowings made are unsecured and are priced at a fixed

rate based upon market conditions at the time of funding in accordance with

the terms of the credit agreement. The credit agreement contains certain

restrictive covenants, which include maintenance of a debt leverage ratio

as defined by the credit agreement.The Company was in compliance with those

covenants at February 1, 2008. Three banking institutions are participating

in the credit agreement. As of February 1, 2008, there was C$60 million or

the equivalent of $60 million outstanding under the credit facility.The interest

rate on the short-term borrowing was 5.75%.

Five banks have extended lines of credit aggregating $789 million for

the purpose of issuing documentary letters of credit and standby letters of

credit. These lines do not have termination dates and are reviewed periodi-

cally. Commitment fees ranging from .225% to .50% per annum are paid

on the standby letters of credit amounts outstanding. Outstanding letters of

credit totaled $299 million as of February 1, 2008, and $346 million as of

February 2, 2007.

NOTE 5 LONG-TERM DEBT

Fiscal Year

(In millions) of Final February 1, February 2,

Debt Category Interest Rates Maturity 2008 2007

Secured debt:1

Mortgage notes 6.00 to 8.25% 2028 $ 33 $ 30

Unsecured debt:

Debentures 6.50 to 6.88% 2029 694 693

Notes 8.25% 2010 499 498

Medium-term notes –

series A 7.35 to 8.20% 2023 20 27

Medium-term notes –

series B27.11 to 7.61% 2037 217 267

Senior notes 5.00 to 6.65% 2037 3,271 1,980

Convertible notes 0.86 to 2.50% 2021 511 518

Capital leases and other 2030 371 400

Total long-term debt 5,616 4,413

Less current maturities 40 88

Long-term debt,excluding current maturities $5,576 $4,325

1Real properties with an aggregate book value of $47 million were pledged as collateral at

February 1, 2008, for secured debt.

2Approximately 46% of these medium-term notes may be put at the option of the holder on the

twentieth anniversary of the issue at par value. The medium-term notes were issued in 1997.

None of these notes are currently putable.

Debt maturities, exclusive of unamortized original issue discounts,

capital leases and other, for the next five years and thereafter are as follows:

2008, $10 million; 2009, $10 million; 2010, $501 million; 2011, $1 million;

2012, $552 million; thereafter, $4.3 billion.

The Company’s debentures, notes, medium-term notes, senior notes and

convertible notes contain certain restrictive covenants. The Company was in

compliance with all covenants in these agreements at February 1, 2008.

Senior Notes

In September 2007, the Company issued $1.3 billion of unsecured senior

notes comprised of three tranches: $550 million of 5.60% senior notes

maturing in September 2012, $250 million of 6.10% senior notes maturing

in September 2017 and $500 million of 6.65% senior notes maturing in

September 2037. The 5.60%, 6.10% and 6.65% senior notes were issued

at discounts of approximately $2.7 million, $1.3 million and $6.3 million,

respectively. Interest on the senior notes is payable semiannually in arrears

in March and September of each year until maturity, beginning in March 2008.

The discount associated with the issuance is included in long-term debt and

is being amortized over the respective terms of the senior notes. The net

proceeds of approximately $1.3 billion were used for general corporate

purposes, including capital expenditures and working capital needs, and

for repurchases of shares of the Company’s common stock.