Lowe's 2007 Annual Report Download - page 26

Download and view the complete annual report

Please find page 26 of the 2007 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

24 |LOWE’S 2007 ANNUAL REPORT

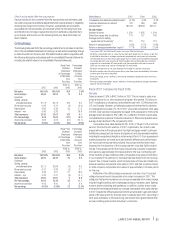

In October 2007, we established a Canadian dollar (C$) denominated

credit facility in the amount of C$50 million, which provides revolving credit

support for our Canadian operations. This uncommitted facility provides us

the ability to make unsecured borrowings that are priced at a fixed rate based

upon market conditions at the time of funding in accordance with the terms of

the credit facility.As of February 1, 2008,there were no borrowings outstanding

under the credit facility.

In January 2008,we entered into a C$ denominated credit agreement in

the amount of C$200 million for the purpose of funding the build-out of retail

stores in Canada and for working capital and other general corporate purposes.

Borrowings made are unsecured and are priced at a fixed rate based upon

market conditions at the time of funding in accordance with the terms of the

credit agreement.The credit agreement contains certain restrictive covenants,

which include maintenance of a debt leverage ratio as defined by the credit

agreement.We were in compliance with those covenants at February 1,2008.

Three banking institutions are participating in the credit agreement. As of

February 1, 2008, there was C$60 million or the equivalent of $60 million

outstanding under the credit facility. The interest rate on the short-term

borrowing was 5.75%.

Five banks have extended lines of credit aggregating $789 million for the

purpose of issuing documentary letters of credit and standby letters of credit.These

lines do not have termination dates and are reviewed periodically. Commitment

fees ranging from .225% to .50% per annum are paid on the standby letters of

credit amounts outstanding. Outstanding letters of credit totaled $299 million

as of February 1, 2008,and $346 million as of February 2, 2007.

Cash Requirements

Capital Expenditures

Our 2008 capital budget is approximately $4.2 billion, inclusive of approximately

$350 million of lease commitments,resulting in a net cash outflow of $3.8 billion

in 2008.Approximately 81% of this planned commitment is for store expansion.

Expansion plans for 2008 consist of approximately 120 new stores.This planned

expansion is expected to increase sales floor square footage by approximately

8%.All of the 2008 projects will be owned, which includes approximately 29%

that will be ground-leased properties.

On February 1, 2008,we owned and operated 13 regional distribution

centers (RDCs).We opened new RDCs in Rockford, Illinois and Lebanon, Oregon

in 2007.We will open our next RDC in Pittston,Pennsylvania in the second half

of 2008.On February 1,2008,we also operated 14 flatbed distribution centers

(FDCs) for the handling of lumber, building materials and other long-length items.

We opened a new FDC in Port of Stockton,California in 2007.We owned 12

and leased two of these FDCs.We expect to open an additional FDC in Purvis,

Mississippi in 2008.

Debt and Capital

In September 2007, we issued $1.3 billion of unsecured senior notes,comprised

of three tranches: $550 million of 5.60% senior notes maturing in September

2012, $250 million of 6.10% senior notes maturing in September 2017 and

$500 million of 6.65% senior notes maturing in September 2037. Interest on

the senior notes is payable semiannually in arrears in March and September

of each year until maturity, beginning in March 2008.

Fromtheirissuancethroughtheendof 2007,principalamounts of$985million,

or approximately 98%, of our February 2001 convertible notes had converted

from debt to equity. In 2007, $18 million in principal amounts converted.

Holders of the senior convertible notes,issued in October 2001,may convert

their notes into 34.424 shares of the company’s common stock only if:the closing

share price of the company’s common stock reaches specified thresholds, or the

credit rating of the notes is below a specified level, or the notes are called for

redemption,or specified corporate transactions representing a change in control

have occurred.There is no indication that we will not be able to maintain the

minimum investment grade rating. From their issuance through the end of

2007, an insignificant amount of the senior convertible notes had converted

from debt to equity.During the fourth quarter of 2006 and the first and second

quarters of 2007, our closing share prices reached the specified threshold

such that the senior convertible notes became convertible at the option of each

holder into shares of common stock in the first, second and third quarters of

2007.The senior convertible notes did not become convertible in the fourth

quarter of 2007 and will not become convertible in the first quarter of 2008,

because our closing share prices did not reach the specified threshold. Cash

interest payments on the senior convertible notes ceased in October 2006.

We may redeem for cash all or a portion of the notes at any time, at a price

equal to the sum of the issue price plus accrued original issue discount on the

redemption date.

Our debt ratings at February 1, 2008, were as follows:

Current Debt Ratings S&P Moody’s Fitch

Commercial paper A1 P1 F1+

Senior debt A+ A1 A+

Outlook Stable Stable Stable

On March 13, 2008, Fitch downgraded our commercial paper rating to

F1 from F1+ and affirmed our senior debt rating at A+, changing our outlook

to negative from stable.

We believe that net cash provided by operating activities and financing

activities will be adequate for our expansion plans and other operating require-

ments over the next 12 months. However, the availability of funds through the

issuance of commercial paper and new debt could be adversely affected due to

a debt rating downgrade or a deterioration of certain financial ratios. In addition,

continuing volatility in the capital markets may affect our ability to access those

markets for additional borrowings or increase costs associated with raising

funds.There are no provisions in any agreements that would require early cash

settlement of existing debt or leases as a result of a downgrade in our debt rating

or a decrease in our stock price.

We are committed to maintaining strong commercial paper ratings through

the management of debt-related ratios.

Dividends and Share Repurchases

Our quarterly cash dividend was increased in 2007 to $.08 per share, a 60%

increase over the prior year.

As of February 2, 2007, the total remaining authorization under the share

repurchase program was $1.5 billion.On May 25, 2007 the Board of Directors

authorized up to an additional $3.0 billion in share repurchases through 2009.

This program is implemented through purchases made from time to time either

in the open market or through private transactions.Shares purchased under the

share repurchase program are retired and returned to authorized and unissued

status. During 2007, we repurchased 76.4 million shares at a total cost of

$2.3 billion. As of February 1, 2008, the total remaining authorization under

the share repurchase program was $2.2 billion. Our current outlook for 2008

does not assume any share repurchases.

OFF-BALANCE SHEET ARRANGEMENTS

Other than in connection with executing operating leases, we do not have any

off-balance sheet financing that has, or is reasonably likely to have, a material,

current or future effect on our financial condition,cash flows,results of operations,

liquidity, capital expenditures or capital resources.