Lowe's 2007 Annual Report Download - page 24

Download and view the complete annual report

Please find page 24 of the 2007 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

22 |LOWE’S 2007 ANNUAL REPORT

Our Big 3 Specialty Sales initiatives had mixed results in 2007. Growth in

Installed Sales was 2.8% and growth in Special Order Sales was 0.5% in 2007,

while comparable store sales declined 5.5% for Installed Sales and 8.1% for

Special Order Sales as a result of the weakness in bigger-ticket and more complex

projects. For the year, Installed Sales was approximately 6% of our total sales

and Special Order Sales was approximately 8%. In contrast, total sales growth

for Commercial Business Customers outpaced the company average.

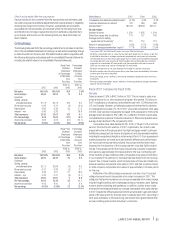

Gross margin

For 2007,gross margin of 34.64% represented a12-basis-point increase over

2006.This increase as a percentage of sales was primarily driven by leverage

of 13 basis points related to positive product mix shifts, 11 basis points related

to increased penetration of imported goods and five basis points of improved

inventory shrink results.This leverage was partially offset by de-leverage of

13 basis points in transportation costs primarily attributable to rising fuel costs,

and seven basis points as a result of start-up costs for new distribution facilities.

SG&A

The increase in SG&A as a percentage of sales from 2006 to 2007 was primarily

driven by de-leverage of 67 basis points in store payroll as a result of the weak

sales environment.As sales per store declined,stores were meeting our minimum

staffing hours threshold which increased the proportion of fixed to total payroll.

Although this creates short-term pressure on earnings, in the long-term it

ensures that we maintain the high service levels that customers have come to

expect from Lowe’s. In addition, we saw de-leverage of eight basis points in

retirement plan expenses as a result of changes to the 401k plan to replace the

performance match program with an increased baseline match.No performance

match was earned in 2006.We also had de-leverage in fixed expenses such as

rent, utilities and property taxes as a result of softer sales.These items were

partially offset by leverage of 23 basis points in advertising expense, primarily

attributable to reduced spending on tab production and distribution, and

national television advertising.

Store opening costs

Store opening costs,which include payroll and supply costs incurred prior to store

opening as well as grand opening advertising costs,totaled $141 million in 2007,

compared to $146 million in 2006.These costs are associated with the opening

of 153 stores in 2007 (149 new and four relocated),as compared with the open-

ing of 155 stores in 2006 (151 new and four relocated).Store opening costs for

stores opened during the year in the U.S.averaged approximately $0.8 million

and $0.9 million per store in 2007 and 2006,respectively.Store opening costs for

stores opened during the year in Canada averaged approximately $2.4 million

per store in 2007 as a result of additional expenses necessary to enter a new

market. Because store opening costs are expensed as incurred, the timing of

expense recognition fluctuates based on the timing of store openings.

Depreciation

Depreciation de-leveraged 35 basis points as a percentage of sales in 2007.

This de-leverage was driven by the opening of 153 stores in 2007 and nega-

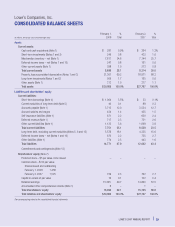

tive comparable store sales.Property,less accumulated depreciation, increased

to $21.4 billion at February 1, 2008, compared to $19.0 billion at February 2,

2007.At February 1,2008,we owned 87% of our stores,compared to 86% at

February 2, 2007, which includes stores on leased land.

Interest

Net interest expense is comprised of the following:

(In millions) 2007 2006

Interest expense, net of amount capitalized $230 $200

Amortization of original issue discount and loan costs 9 6

Interest income (45) (52)

Net interest expense $194 $154

Interest expense increased primarily as a result of the September 2007

$1.3 billion debt issuance and the October 2006 $1 billion debt issuance,

partially offset by an increase in capitalized interest.

Income tax provision

Our effective income tax rate was 37.7% in 2007 versus 37.9% in 2006.

The decrease in the effective tax rate was due to a continuation of the effect

of increased federal tax credits associated with Welfare to Work and Work

Opportunity Tax Credit programs as well as increased state tax credits

related to our investments in employees and property.

Fiscal 2006 Compared to Fiscal 2005

For the purpose of the following discussion, comparable store sales,comparable

store average ticket and comparable store customer transactions are based

on comparable 52-week periods.

Net sales

Our continued focus on executing the fundamentals and providing customer-

valued solutions together with our store expansion program drove sales of

$46.9 billion in 2006.We opened 155 stores in 2006,including four relocations,

and ended the year with 1,385 stores in 49 states. The additional week in

2005 resulted in approximately $750 million in additional net sales in 2005.

Excluding the additional week, net sales would have increased approximately

10% in 2006.

Comparable store sales were flat in 2006 versus a comparable store sales

increase of 6.1% in 2005. Total customer transactions increased 6.4%

compared to 2005, and average ticket increased 1.9% to $68.98.Average

ticket and customer transactions for comparable stores were relatively flat

versus the prior year.

Sales in many areas of the country were pressured by the slowdown in

the housing market.Markets in the Northeast,Florida and California were most

exposed to the slowdown in housing in 2006 and reduced total company

comparable store sales by approximately 150 basis points for the year. Sales

trends in those markets clearly indicated a cautious home improvement

consumer. Also, areas of the Gulf Coast and Florida, which experienced

increased demand in 2005 related to rebuilding from the hurricanes,experienced

comparable store sales declines of 18.7% in the second half of 2006.

Reflective of the difficult sales environment,11 of our 20 product categories

experienced comparable store sales increases in 2006.The categories that

performed above our average comparable store sales change included rough

plumbing,building materials,rough electrical,home environment,paint,fashion

plumbing, flooring, nursery, seasonal living, and lawn & landscape products.

In addition, hardware performed at approximately our average comparable

store sales change in 2006. Despite the difficult sales environment, we were

able to gain unit market share in all of our 20 product categories versus the

prior calendar year, according to third-party estimates.

Outdoor power equipment and lumber experienced the greatest comparable

store sales declines in 2006. Comparable store generator sales were down

34% for the year, compared to strong sales driven by the 2005 hurricanes.

Additionally, a warmer than normal winter led to comparable store sales declines

for snow throwers. However, despite the difficult sales environment, we

experienced a 2% unit market share gain in outdoor power equipment in

calendar year 2006.Lumber and plywood experienced more than 15% cost

deflation and similar retail price deflation in 2006.

Our Big 3 Specialty Sales initiatives had mixed results in 2006.A hesitation

to take on large projects by some consumers had an impact on our Installed

Sales and Special Order Sales in the second half of 2006. Installed Sales

increased 9% over 2005. Special Order Sales increased 5% over 2005. In

contrast, sales growth for Commercial Business Customers was nearly double

the company average.