Lowe's 2007 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2007 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

LOWE’S 2007 ANNUAL REPORT |23

Gross margin

For 2006,gross margin of 34.52% represented a 32-basis-point increase over

2005.This increase as a percentage of sales was primarily due to leverage of

20 basis points related to positive product mix shifts and a greater proportion

of imported goods, which typically have lower acquisition costs. For 2006, we

imported approximately 11% of our goods, compared to approximately 9.5%

in the prior year.These items were slightly offset by de-leverage of nine basis

points in inventory shrink as a percentage of sales.

SG&A

The decrease in SG&A as a percentage of sales from 2005 to 2006 was primarily

due to lower expenses related to bonus and retirement plans.Our performance-

based bonus and retirement expenses fluctuate with our sales and earnings

performance relative to plan, and decreased approximately $200 million, or

50 basis points, in 2006. In addition, insurance expense leveraged 12 basis

points in 2006, a result of our ongoing safety initiatives and the benefits of

regulatory changes in certain states,which contributed to actuarial projections

of lower costs to settle claims.These items were partially offset by de-leverage

in store payroll.As sales slowed throughout the year, our stores adjusted their

hours accordingly. However, because of our base staffing requirements and

customer service standards, we chose not to reduce payroll at the same rate

as sales.

Store opening costs

Store opening costs, which include payroll and supply costs incurred prior to

store opening as well as grand opening advertising costs, totaled $146 million

in 2006, compared to $142 million in 2005.These costs are associated with

the opening of 155 stores in 2006 (151 new and four relocated), as compared

with the opening of 150 stores in 2005 (147 new and three relocated). Store

opening costs for stores opened during the year averaged approximately

$0.9 million per store in 2006 and 2005. Because store opening costs are

expensed as incurred, the timing of expense recognition fluctuates based on

the timing of store openings.

Depreciation

Depreciation de-leveraged 21 basis points as a percentage of sales in 2006.

This de-leverage was driven by growth in assets and the softer sales environment.

At February 2, 2007, we owned 86% of our stores, compared to 84% at

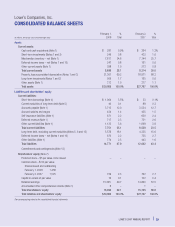

February 3,2006,which includes stores on leased land.Property, less accumu-

lated depreciation, increased to $19.0 billion at February 2, 2007, compared

to $16.4 billion at February 3, 2006.The increase in property resulted primarily

from our store expansion program as well as our remerchandising efforts.

Interest

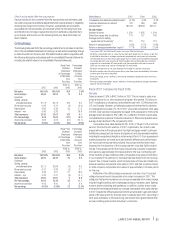

Net interest expense is comprised of the following:

(In millions) 2006 2005

Interest expense, net of amount capitalized $200 $186

Amortization of original issue discount and loan costs 6 17

Interest income (52) (45)

Net interest expense $154 $158

Interest expense increased primarily due to the October 2006 $1 billion debt

issuance, partially offset by lower interest expense on convertible debt due to

conversions during 2006. Interest expense relating to capital leases was

$34 million for 2006 and$39 millionfor 2005.Amortization of loancostsdecreased

in 2006 versus the prior year as a result of increased debt conversions.

Income tax provision

Our effective income tax rate was 37.9% in 2006 versus 38.5% in 2005.The

decrease in the effective tax rate was the result of increased federal tax credits

associated with Welfare toWork andWork OpportunityTax Credit programs and

increased state tax credits related to our investments in employees and property.

FINANCIAL CONDITION, LIQUIDITY AND

CAPITAL RESOURCES

Cash Flows

The following table summarizes the components of the consolidated statements

of cash flows.This table should be read in conjunction with the following

discussion and analysis and the consolidated financial statements, including

the related notes to the consolidated financial statements:

(In millions) 2007 2006 2005

Net cash provided by operating activities $4,347 $4,502 $ 3,842

Net cash used in investing activities (4,123) (3,715) (3,674)

Net cash used in financing activities (307) (846) (275)

Net decrease in cash and cash equivalents (83) (59) (107)

Cash and cash equivalents,beginning of year 364 423 530

Cash and cash equivalents, end of year $ 281 $ 364 $ 423

Cash flows from operating activities provide a significant source of our

liquidity.The change in cash flows from operating activities in 2007 compared

to 2006 resulted primarily from decreased net earnings and an increase in

inventory as a result of our store expansion program, partially offset by an

increase in deferred revenue associated with our extended warranty program.

The change in cash flows from operating activities in 2006 compared to 2005

resulted primarily from increased net earnings and increased days payable

outstanding, partially offset by the timing of tax payments and a decline in

deferred revenue associated with Specialty Sales.

The primary component of net cash used in investing activities continues

to be opening new stores, investing in existing stores through resets and

remerchandising, and investing in our distribution center and information

technology infrastructure. Cash acquisitions of fixed assets were $4.0 billion

for 2007, $3.9 billion in 2006 and $3.4 billion in 2005.The February 1, 2008,

retail selling space of 174 million square feet represented an 11% increase over

February 2, 2007.The February 2, 2007, retail selling space of 157 million

square feet represented a 12% increase over February 3, 2006.

The change in cash flows from financing activities in 2007 compared to

2006 resulted primarily from increased short-term and long-term borrowings.

This was offset by greater repurchases of common stock under our share

repurchase program in 2007 compared to 2006 and an increase in dividends

paid from $0.18 per share in 2006 to $0.29 per share in 2007.The change in

cash flows from financing activities in 2006 compared to 2005 resulted primarily

from greater repurchases of common stock.The ratio of debt to equity plus debt

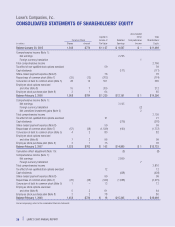

was 29.3% and 22.0% as of the years ended 2007 and 2006, respectively.

Sources of Liquidity

In addition to our cash flows from operations, additional liquidity is provided

by our short-term borrowing facilities. In June 2007, we entered into an

Amended and Restated Credit Agreement (Amended Facility) to modify the

senior credit facility by extending the maturity date to June 2012 and providing

for borrowings of up to $1.75 billion versus $1.0 billion under the previous

facility.TheAmended Facility supports our commercial paper and revolving credit

programs. Borrowings made are unsecured and are priced at a fixed rate based

upon market conditions at the time of funding in accordance with the terms of

theAmended Facility.TheAmended Facility contains certain restrictive covenants,

which include maintenance of a debt leverage ratio as defined by the Amended

Facility.We were in compliance with those covenants at February 1, 2008.

Seventeen banking institutions are participating in the Amended Facility.As of

February 1, 2008,there was $1.0 billion outstanding under the commercial

paper program that was issued in the fourth quarter. The weighted-average

interest rate on the outstanding commercial paper was 3.92%.