Starbucks 2002 Annual Report Download - page 19

Download and view the complete annual report

Please find page 19 of the 2002 Starbucks annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26

|

|

33

The Company’s valuations are based upon a multiple option

valuation approach, and forfeitures are recognized as they

occur. The Black-Scholes option valuation model was

developed for use in estimating the fair value of traded options,

which have no vesting restrictions and are fully transferable. In

addition, option valuation models require the input of highly

subjective assumptions, including the expected stock-price

volatility. The Company’s employee stock options have

characteristics significantly different from those of traded

options, and changes in the subjective input assumptions can

materially affect the fair value estimate. Because Company

stock options do not trade on a secondary exchange,

employees can receive no value nor derive any benefit from

holding stock options under these plans without an increase,

above the grant price, in the market price of the Company’s

stock. Such an increase in stock price would benefit all

stockholders commensurately.

As required by SFAS No. 123, the Company has determined

that the weighted average estimated fair values of options

granted during fiscal 2002, 2001 and 2000 were $6.48, $8.98

and $5.37 per share, respectively.

In applying SFAS No. 123, the impact of outstanding stock

options granted prior to 1996 has been excluded from the pro

forma calculations; accordingly, the 2002 pro forma

adjustments are not necessarily indicative of future period pro

forma adjustments.

Defined Contribution Plan

Starbucks maintains voluntary defined contribution plans

covering eligible employees as defined in the plan documents.

Participating employees may elect to defer and contribute a

portion of their compensation to the plan up to plan limits of

approximately 19%, not to exceed the dollar amounts set by

applicable laws. Effective January 1, 2003, participating

employees may elect to defer and contribute up to 50% of their

compensation. For certain plans, the Company matched 25%

of each employee’s eligible contribution up to a maximum of

the first 4% of each employee’s compensation. Beginning

April 1, 2002, the Company’s matching contributions for the

majority of its plans were increased to a maximum of 150%,

depending on participants’ years of service.

The Company’s matching contributions to all plans were

approximately $3.1 million, $1.6 million and $1.1 million in

fiscal 2002, 2001 and 2000, respectively.

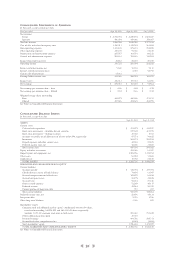

Note 13: Income Taxes

A reconciliation of the statutory federal income tax rate with

the Company’s effective income tax rate is as follows:

Fiscal year ended Sept 29, Sept 30, Oct 1,

2002 2001 2000

Statutory rate 35.0% 35.0% 35.0%

State income taxes, net of federal

income tax benefit 3.4 3.8 3.7

Valuation allowance change

from prior year (0.9) 0.9 3.5

Other, net (0.5) (2.4) (1.1)

Effective tax rate 37.0% 37.3% 41.1 %

The provision for income taxes consists of the following

(in thousands):

Fiscal year ended Sept 29, Sept 30, Oct 1,

2002 2001 2000

Currently payable:

Federal $ 109,154 $ 91,750 $ 70,157

State 16,820 17,656 12,500

Foreign 5,807 3,198 1,601

Deferred tax asset, net (5,468) (4,892) (18,252)

Total $ 126,313 $ 107,712 $ 66,006

Deferred income taxes or tax benefits reflect the tax effect of

temporary differences between the amounts of assets and

liabilities for financial reporting purposes and amounts as

measured for tax purposes. The Company will establish a

valuation allowance if it is more likely than not these items will

either expire before the Company is able to realize their

benefits, or that future deductibility is uncertain. Periodically,

the valuation allowance is reviewed and adjusted based on

management’s assessments of realizable deferred tax assets.The

valuation allowance as of September 29, 2002, was related to

losses from investments in majority-owned foreign

subsidiaries; the valuation allowance as of September 30, 2001,

was related to losses from investments in majority-owned

foreign subsidiaries and from Internet-related companies.The

tax effect of temporary differences and carryforwards that

cause significant portions of deferred tax assets and liabilities is

as follows (in thousands):

Sept 29, Sept 30,

2002 2001

Deferred tax assets:

Equity and other investments $ 14,026 $ 3,784

Capital loss carryforwards 6,077 17,448

Accrued occupancy costs 14,597 12,317

Accrued compensation and related costs 12,726 9,898

Other accrued expenses 16,608 7,245

Foreign tax credits 10,199 5,199

Other 6,971 164

Total 81,204 56,055

Valuation allowance (5,476) (8,704)

To tal deferred tax asset, net

of valuation allowance 75,728 47,351

Deferred tax liabilities:

Property, plant and equipment (50,819) (34,260)

Other (5,199) (355)

Total (56,018) (34,615)

Net deferred tax asset $ 19,710 $ 12,736

As of September 29, 2002, the Company had foreign tax credit

carryforwards of $10.2 million with expiration dates between

fiscal years 2004 and 2008.The Company also had capital loss

carryforwards of $15.8 million expiring in 2006.

Taxes currently payable of $32.8 million and $50.3 million are

included in “Accrued taxes” on the accompanying

consolidated balance sheets as of September 29, 2002, and

September 30, 2001, respectively.

The fair value of stock-based awards to employees is estimated on the date of grant using the Black-Scholes option-pricing model

with the following weighted average assumptions:

Employee Stock Options Employee Stock Purchase Plan

2002 2001 2000 2002 2001 2000

Expected life (years) 2 – 5 2 – 5 2 – 6 0.25 0.25 0.25

Expected volatility 43% – 54% 57% 55% 33% – 51% 41% – 49% 42% – 82%

Risk-free interest rate 1.63% – 4.96% 2.37% – 5.90% 5.65% – 6.87% 1.93% – 2.73% 2.35% – 4.68% 5.97% – 6.40%

Expected dividend yield 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%