Starbucks 2002 Annual Report Download - page 5

Download and view the complete annual report

Please find page 5 of the 2002 Starbucks annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

|

|

19

RESULTS OF OPERATIONS—FISCAL 2002 COMPARED TO

FISCAL 2001

Systemwide Retail Store Sales

Systemwide retail store sales, which include net sales for both

Company-operated and licensed retail stores, were $3.8 billion

in fiscal 2002, an increase of 29% from $3.0 billion in fiscal

2001, primarily due to the opening of 1,177 new stores and

strong comparable store sales growth in North America.

During fiscal 2003, Starbucks expects to open at least 1,200

new stores, including approximately 525 Company-operated

and 225 licensed stores in North America, and 75 Company-

operated and 375 licensed stores internationally.

Consolidated Net Revenues

During the fiscal year ended September 29, 2002, Starbucks

derived approximately 85% of net revenues from its

Company-operated retail stores. Retail revenues include the

North American Retail and International Retail business

units. The remaining 15% of net revenues was derived from

the Company’s Specialty Operations, which includes Business

Alliances and all other non-retail business units.

Net revenues increased 24% from $2.6 billion in fiscal 2001 to

$3.3 billion in fiscal 2002, primarily due to the Company’s

store expansion program and comparable store sales increases.

Comparable store sales increased by 6%, 5%, and 9% in fiscal

2002, 2001 and 2000, respectively. As a result of its expansion

strategy of clustering stores in existing markets, Starbucks has

experienced a certain level of cannibalization of sales of

existing stores by new stores as store concentration has

increased.However, management believes such cannibalization

has been justified by the incremental sales and return on new

store investments. This cannibalization, as well as increased

competition, slowing economies and other factors, may put

downward pressure on the Company’s comparable store sales

growth in future periods.

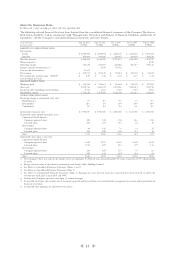

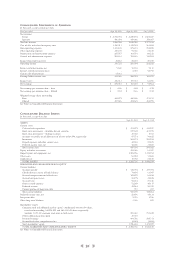

The table below reconciles revenues by operating segment to

revenues on the accompanying consolidated statements of

earnings (in thousands):

Fiscal year ended Sept 29, Sept 30, Oct 1,

2002 2002 2000

North American Retail $ 2,583,756 $ 2,086,354 $1,734,929

International Retail 209,148 143,240 88,678

Subtotal – Retail revenues 2,792,904 2,229,594 1,823,607

Business Alliances 222,410 193,574 160,812

All other business units

(excl. International Retail) 344,425 276,603 216,402

Intersegment revenues (1) (70,831) (50,791) (23,207)

Subtotal – Specialty revenues 496,004 419,386 354,007

Total net revenues $ 3,288,908 $ 2,648,980 $2,177,614

(1) Intersegment revenues consist primarily of product sales to and from

subsidiaries and equity method investees.

Net Revenues by Segment

North American Retail

North American Retail revenues increased by $497.4 million,

or 24%, to $2.6 billion in fiscal 2002, from $2.1 billion in fiscal

2001, primarily due to the opening of 525 new retail stores in

fiscal 2002 and comparable store sales growth of 7% for the

period. The increase in comparable store sales was due to

higher transaction volume. Management believes increased

customer traffic was driven by new product innovation, which

continues to broaden the customer base during non-peak

hours of operation, and by expanding the Company’s capacity

to satisfy customer demand through enhanced technology,

training and execution at retail stores.

Business Alliances

Business Alliances revenues increased by $28.8 million, or 15%,

to $222.4 million in fiscal 2002, from $193.6 million in fiscal

2001, primarily due to the opening of 269 new licensed stores

in fiscal 2002 and the resulting increase in royalty revenues

from and product sales to those licensees.

All Other Business Units (including International Retail, net of

Intersegment revenues)

Revenues for all other business units increased by $113.6

million, or 31%, to $482.7 million for fiscal 2002, from $369.1

million in fiscal 2001. This increase was mainly related to

growth in the number of international Company-operated

and licensed retail stores.

Consolidated Results of Operations

Cost of sales and related occupancy costs decreased to 41.0%

of net revenues in fiscal 2002, from 42.0% in fiscal 2001.The

decrease was primarily due to a shift in sales mix to higher

margin products, such as handcrafted beverages, as well as

lower green coffee costs. Starbucks does not expect a benefit

from lower green coffee costs in fiscal 2003, as the Company

has moved away from formula-based commodity exchange

pricing contracts, and is instead basing most contracts on

higher, fixed prices to encourage the continuing supply of

high-quality green coffee. Improvements in cost of sales were

partially offset by higher occupancy costs due to increased

repair and maintenance activities on Company-operated retail

stores and the continuing trend of higher retail rent expense.

Store operating expenses as a percentage of retail revenues

increased to 40.1% in fiscal 2002, from 39.3% in fiscal 2001.

The restaurant portion of retail revenues, which is comprised

of made-to-order beverages and fresh food, was a higher

proportion of total retail revenues in fiscal 2002.This resulted

in higher payroll-related expenditures due to the continuing

shift in sales to more labor-intensive handcrafted beverages as

well as higher average wage rates. Higher provisions for retail

store asset impairment and disposals of $26.0 million in fiscal

2002 compared to $7.3 million in fiscal 2001 also contributed

to the unfavorable variance.

Starbucks regularly monitors the financial results of its

Company-operated retail stores and accumulates historical

operating measures to identify performance trends in various

markets. Provisions for asset impairment are recorded when,

among other things, retail stores are unable to generate current

and future estimated undiscounted cash flows in excess of asset

carrying values. Gains and losses on disposals are generated

primarily through renovation activities.

Other operating expenses (expenses associated with non-

retail operations) were 25.6% of specialty revenues in fiscal

2002, compared to 22.3% in fiscal 2001. The increase was a

result of continued development of the Company’s

international infrastructure, including additional regional

offices and employees supporting global expansion, as well as

higher advertising expenditures from the Company’s

interactive operations.

Depreciation and amortization expenses increased to $205.6

million in fiscal 2002, from $163.5 million in fiscal 2001.The

increase was primarily due to the opening of 525 new North

American and 89 new international Company-operated

retail stores.

General and administrative expenses increased to $202.2

million in fiscal 2002, compared to $151.4 million in fiscal

2001.The increase was primarily due to higher payroll-related

expenditures and an $18.0 million litigation settlement charge

related to two class action lawsuits.

Operating income increased 13.4% to $318.7 million in fiscal

2002, from $281.1 million in fiscal 2001.The operating margin

decreased to 9.7% of total net revenues in fiscal 2002,

compared to 10.6% in fiscal 2001 primarily due to higher

operating expenses partially offset by cost of sales

improvements, as discussed above.