Starbucks 2003 Annual Report Download - page 4

Download and view the complete annual report

Please find page 4 of the 2003 Starbucks annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

|

|

16 Fiscal2003AnnualReport

Fiscal2003AnnualReport 17

MANAGEMENT’SDISCUSSIONANDANALYSISOF

FINANCIALCONDITIONANDRESULTSOFOPERATIONS

General

StarbucksCorporation’sfiscalyearendsontheSundayclosest

toSeptember30.Fiscalyears2003,2002and2001eachhad

52weeks.Thefiscal yearendingonOctober3,2004,will

include53weeks.

Acquisitions

On July 14, 2003, the Company acquired Seattle Coffee

Company (“SCC”) from AFC Enterprises, Inc. SCC

includes the Seattle’s Best Coffee® and Torrefazione Italia®

brands,whichcomplementtheCompany’sexistingportfolio

of products. The results of operations of SCC are included

intheaccompanyingconsolidatedfinancialstatementsfrom

the date of purchase. The $70 million all-cash purchase

transactiongeneratedgoodwillofapproximately$43million

and indefinite-lived intangibles, consisting of trade names

andrecipes,ofapproximately$13million.Proformaresults

ofoperations havenotbeenprovided,as theamountswere

notdeemedmaterialtotheconsolidatedfinancialstatements

ofStarbucks.

Duringfiscal2003,Starbucksincreaseditsequityownership

to 50% for its international licensed operations in Austria,

Shanghai,Spain,SwitzerlandandTaiwan,whichenabledthe

Companytoexertsignificantinfluenceovertheiroperating

and financial policies. For these operations, management

determined that a change in accounting method, from

the cost method to the equity method, was required. This

accounting change included adjusting previously reported

information for the Company’s proportionate share of net

losses as required by Accounting Principles Board Opinion

No.18,“TheEquityMethodofAccountingforInvestments

inCommonStock.”

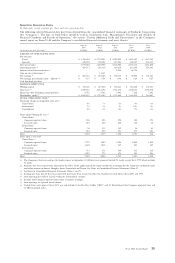

As shown in the table below, the cumulative effect of

the accounting change to the equity method resulted in

reductionsofnetearningsof$2.4millionand$0.9millionfor

the52weeksendedSeptember29,2002,andSeptember30,

2001,respectively(inthousands,exceptearningspershare):

52weeksended

Sept29, Sept30,

2002 2001

Netearnings,previouslyreported$215,073$ 181,210

Effectofchangetoequitymethod (2,387) (875)

Netearnings,asrestated $212,686$ 180,335

Netearningspercommonshare–basic:

Previouslyreported $ 0.56$ 0.48

Asrestated $ 0.55$ 0.47

Netearningspercommonshare–diluted:

Previouslyreported $ 0.54$ 0.46

Asrestated $ 0.54$ 0.46

Additionally,areductionofnetearningsfortheeffectsofthe

accounting change prior to fiscal 2001of $0.2millionwas

recorded.

Reclassifications

During the fiscal first quarter of 2004, the Company

realigneditsresourcestobettermanageitsrapidly growing

operations. In connection with this process, classification

of operating expenses within the consolidated statements

of earnings was evaluated using broad-based definitions of

retail, specialty and general and administrative functions.

As a result, management determined that certain functions

notdirectly supporting retailornon-retailoperations, such

as executive, administrative, finance and risk management

overheadprimarilywithininternationaloperations,wouldbe

moreappropriatelyclassifiedas“Generalandadministrative

expenses” than as store or other operating expenses.

Accordingly, amounts in prior year periods have been

reclassifiedtoconformtocurrentyearclassifications.