Walmart 2002 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2002 Walmart annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

|

|

16

Wal-Mart is a large but straightforward business. In the United States, our operations are centered around retail stores and membership warehouse clubs.

Internationally, our operations are centered on retail stores, warehouse clubs and restaurants. We have built our business by offering our customers

quality merchandise at low prices. We are able to lower the cost of merchandise through our negotiations with suppliers and by efficiently managing our

distribution network. The key to our success is our ability to grow our base business. In the U.S. we grow our base business by aggressively building new

stores and by increasing sales in our existing stores. Internationally, we grow our business by building new stores, increasing sales in our existing stores

and through acquisitions. We intend to continue to expand both domestically and internationally.

Because we are a large company, we do enter into some complex transactions. One complex area is our derivatives program. We do not use derivative

instruments for speculation or for the purpose of creating additional revenues; however, we do enter into derivative transactions to limit our exposure

to known business risks. Examples of these business risks include changes in interest rates and movements in foreign currency exchange rates. The

discussion of our derivative transactions has been given a great deal of space in the financial section of this Annual Report. The Market Risk section

of this Management’s Discussion and Analysis and Note 4 to the Consolidated Financial Statements give you more information on these transactions.

Please remember that the accounting and disclosure rules for derivative transactions are very specific and any discussion of them requires the use of

technical terminology.

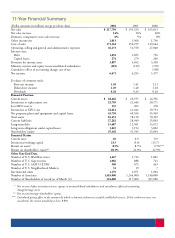

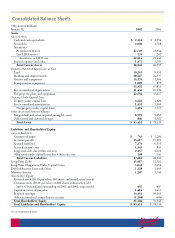

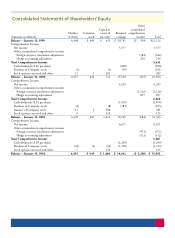

Net Sales

The Company and each of its operating segments had net sales (in millions) for the three fiscal years ended January 31, 2002 as follows:

Fiscal Year Wal-Mart Stores SAM’S CLUB International Other Total Company Total Company Increase

from Prior Fiscal Year

2002 $ 139,131 $ 29,395 $ 35,485 $ 13,788 $ 217,799 14%

2001 121,889 26,798 32,100 10,542 191,329 16%

2000 108,721 24,801 22,728 8,763 165,013 20%

Our net sales grew by 14% in fiscal 2002 when compared with fiscal 2001. That increase resulted from our domestic and international expansion

programs, and a domestic comparative store sales increase of 6% when compared with fiscal 2001. The sales increase of 16% in fiscal 2001, when

compared with fiscal 2000, resulted from our domestic and international expansion programs, and a domestic comparative store sales increase of 5%.

The Wal-Mart Stores and SAM’S CLUB segments include domestic units only. Wal-Mart stores and SAM’S CLUBS located outside the United States

are included in the International segment.

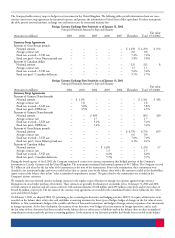

Costs and Expenses

For fiscal 2002, our cost of sales increased as a percentage of total net sales when compared to fiscal 2001, resulting in an overall decrease of 0.24%

in the Company’s gross margin from 21.47% in the fiscal year 2001 to a gross margin of 21.23% in fiscal 2002. This decrease in gross margin

occurred primarily due to a shift in customer buying patterns to products that carry lower margins and an increase in food sales as a percent of our

total sales. Food products generally carry lower margins than general merchandise. Management expects our gross margins to continue to decrease as

food sales continue to increase as a percentage of total Company sales both domestically and internationally. Management also expects the Company’s

program to convert many of our Wal-Mart discount stores to Supercenters, which have full-line food departments, and the opening of additional

Neighborhood Markets to result in continuing increases in the percentage that food sales contribute to our total net sales. Partially offsetting the

overall decrease in gross margin in fiscal 2002, the Company reduced cost of sales by $67 million as a result of a LIFO inventory adjustment. A LIFO

inventory adjustment that reduces cost of sales indicates that the current economic environment is deflationary, meaning that on average, identical

products that we sold in both fiscal 2002 and 2001 decreased in price from fiscal 2001 to 2002. The balance in the LIFO reserve on the Company’s

balance sheet is attributable to food inventories and other inventories held by our subsidiary, McLane Company, Inc. Management believes that these

categories will not be disinflationary in the near future and that future gross margins may not benefit from a LIFO adjustment, such as that which

occurred in fiscal 2002.

Our total cost of sales as a percentage of our total net sales decreased for fiscal 2001 when compared to fiscal 2000, resulting in increases in gross margin

of 0.05% for fiscal 2001 to 21.47% from 21.42% in fiscal 2000. This improvement in gross margin resulted primarily from a $176 million LIFO

inventory adjustment that reduced our cost of sales. This LIFO adjustment was offset by continued price rollbacks and increased International sales

and increased food sales.

Our operating, selling, general and administrative expenses increased 0.12% as a percentage of total net sales to 16.61% in fiscal 2002 when compared

with fiscal 2001. This increase was primarily due to increased utility and insurance costs, including Associate medical, property and casualty insurance.

Management believes that the trend of increasing insurance costs will continue for at least the near future. Operating, selling, general and administrative

expenses increased 0.10% as a percentage of sales in fiscal 2001 when compared with fiscal 2000. This increase was primarily due to increased

maintenance and repair costs and depreciation charges incurred during the year.

Interest Costs

Our interest costs for corporate debt decreased 0.09% as a percentage of net sales from 0.57% in fiscal 2001 to 0.48% in fiscal 2002. This decrease

resulted from lower interest rates, less need for debt financing of the Company’s operations due to the Company’s inventory reduction efforts and

the positive impacts of the Company’s fixed rate to variable rate interest rate swap program. For fiscal 2002, total Company inventory increased

approximately 5% on a total Company sales increase of 14%. Interest costs increased 0.11% as a percentage of sales from 0.46% in fiscal 2000 to

0.57% in fiscal 2001. This increase resulted from additional debt issuances made to finance a part of the ASDA acquisition costs, but was somewhat

offset by reductions in debt resulting from the Company’s inventory control efforts. See the Market Risk section of this discussion for further detail

regarding the Company’s fixed to floating interest rate swaps.

Management’s Discussion and Analysis